LIC’s Jan Suraksha (Plan No. 880) is a non-linked, individual micro insurance plan designed for economically weaker sections with affordable premiums. It offers basic life cover, guaranteed additions, and a lump-sum payout at maturity. The plan comes with a limited premium payment term. It is available for individuals aged 18 to 55, with a basic sum assured of ₹1 lakh to ₹2 lakh.

LIC offers scale and trust, but at Ditto, we find its term plans lack strong value for money and modern tech support compared to private insurers. If you prefer LIC as your insurer, consider term plan options such as Digi Term and Bima Kavach, which are designed to meet higher protection needs. This guide is ideal for individuals seeking an LIC-backed plan with low life coverage.

Is LIC Jan Suraksha a term plan? Not really. It is closer to a micro endowment plan that combines small savings with basic life cover. As per the IRDAI annual report 2024-25, LIC issued around 9 lakh micro insurance policies, with total premiums of ₹354.81 crore under individual business. This highlights the insurer’s strong reach and role in expanding insurance access to underserved segments.

In the next few minutes, you will understand how LIC Jan Suraksha works, what it offers, where it falls short, and whether it truly fits your family’s financial protection needs.

High CSR: Above 97%, which indicates strong claim reliability, supported by LIC’s government backing and long track record.

Healthy ASR: Above 90%, which reflects balanced settlement across both small and large claims.

Strong Business Scale: Premium volume well above ₹5,000 crore highlights market leadership and wide reach.

High Claim Payout Capacity: Total death claims paid exceed ₹200 crore, showing the ability to handle large payouts.

Low Complaint Ratio: Around one-fourth of the industry average, indicating a relatively better customer experience at scale.

Robust Solvency Ratio: Above the minimum IRDAI requirement of 1.5x, indicating strong financial stability and ability to meet future claims.

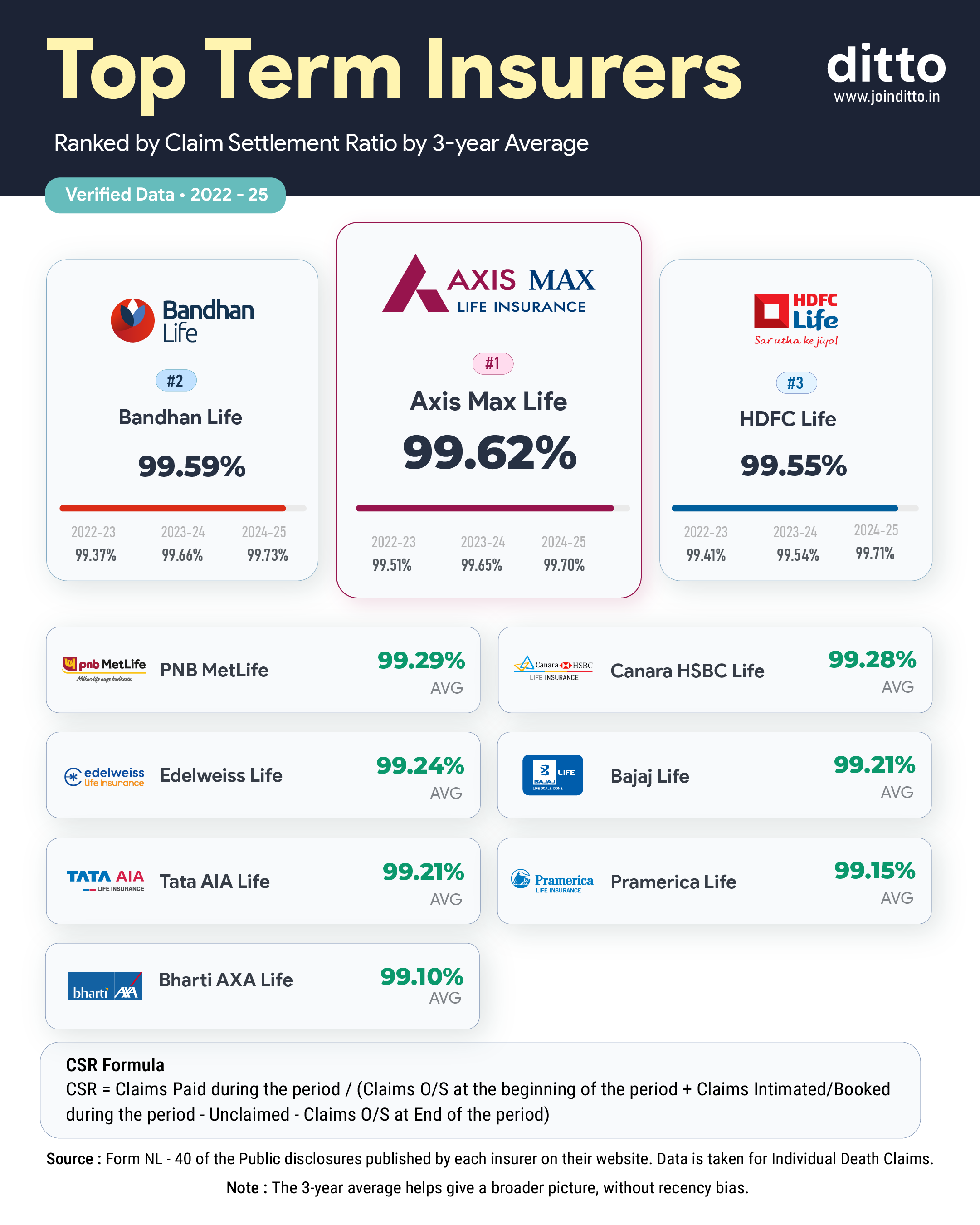

However, LIC does not feature in the top 10 term insurance companies by CSR. This is because, although strong, it falls slightly below the industry mean of 98.66%, which acts as the benchmark for top-ranking term insurers. Take a look at the infographic, which gives a clearer picture of which companies consistently handle claims better and maintain stronger reliability.

Eligibility Criteria of LIC Jan Suraksha Plan

Eligibility

Criteria

Minimum Entry Age

18 years

Maximum Entry Age

55 years

Policy Term

12 to 20 years

Maximum Maturity Age

70 years

Premium Paying Term (PPT)

Policy term minus 5 years

Premium Payment Modes

Yearly, half-yearly, quarterly, and monthly

CTA

Key Features of LIC Jan Suraksha Plan

Death Benefit: The sum assured on death is defined as the higher of seven times the annualized premium or the basic sum assured. In addition, the death benefit will never be less than 105% of the total premiums paid up to the date of death, which ensures a minimum payout for the family. If the policy is active and the life assured passes away during the term, LIC pays the sum assured on death, along with any accrued guaranteed additions.

Auto Cover: The plan offers a safety net if you miss payments after a few years. If you have paid at least 3 years’ premiums, cover continues for 6 months. If you have paid for 5 years or more, the cover extends up to 2 years from the first missed premium.

Loan Facility: You can take a loan after completing one full policy year. LIC allows up to 80% of the surrender value for active policies and 70% for paid-up policies, which provides access to funds if needed.

Accidental Death And Disability Rider Benefit: You can add this rider during the premium paying term if at least 5 years remain. In case of accidental death within 180 days, the rider pays a lump sum amount. If an accident leads to disability, the same amount is paid in monthly installments over 10 years.

Accident Benefit Rider: This rider can be added during the premium paying term if at least 5 years remain. It provides cover only during the premium payment period. In case of accidental death within 180 days, a lump sum equal to the rider's sum assured is paid. The rider cover cannot exceed three times the base sum assured, and its premium is capped at 30% of the base plan premium.

Guaranteed Benefits: This plan offers a simple structure with fixed outcomes. The maturity value and death benefit are not linked to market performance. LIC clearly defines the benefits upfront, so you know exactly what to expect without any bonus uncertainty. You can also see all these values clearly laid out in the benefit illustration provided with the policy.

The maximum sum assured is ₹2 lakh, which is too low for most families. It may not cover income loss, loans, or long-term needs like education and household expenses.

Modest Returns

Based on LIC’s illustration, net returns are around 4% to 5% per year. This makes it more of a low-return savings plan than a strong wealth-building option.

No Bonus Benefit

This is a non-participating plan, so you do not receive any bonuses. The payout stays limited to the guaranteed structure with no benefit from insurer profits.

Early Exit Can Be Costly

Surrender value builds slowly. There is no value in the first year, and only partial value after two years, which can lead to a loss if you exit early.

Premium Comparison Across Policy Term

Age

12 Years Policy Term (7 PPT)

15 Years Policy Term (10 PPT)

20 Years Policy Term (15 PPT)

25

₹13,270

₹9,015

₹5,800

35

₹13,325

₹9,080

₹5,900

45

₹13,530

₹9,340

₹6,250

Note: These sample premiums are illustrative and based on a ₹1 lakh sum assured. The figures are sourced from the LIC Jan Suraksha brochure.

Did You Know?

If your Jan Suraksha policy is active, it continues to earn Guaranteed Additions over time. However, a basic sum assured of ₹1 lakh to ₹1.95 lakh does not provide additional guaranteed benefits. Once you choose ₹2 lakh, you receive an additional 0.25% guaranteed premium addition, which slightly improves your overall returns.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

Backed by Zerodha

Dedicated Claim Support Team

100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

LIC Jan Suraksha is built for simplicity and accessibility. It works well for low-income or first-time buyers who want a small, guaranteed savings plan with basic life cover from a trusted insurer. However, it is not designed for meaningful financial protection as:

It offers limited flexibility compared with comprehensive term plans and larger savings products, which usually provide more customization options, higher coverage, and better payout structures.

LIC Jan Suraksha lets you choose only one of the two available optional riders.

The plan lacks modern-day features like instant payouts upon claim intimation, and you also miss out on essential riders such as critical illness or waiver of premium options.

If you need real protection and flexibility, it is worth exploring the best term insurance plans that align better with your long-term financial goals.

Frequently Asked Questions

What are the LIC Plan 880 details?

The LIC Jan Suraksha Plan (Plan No. 880) is a non-linked, individual micro insurance plan from LIC of India. It is designed for economically weaker sections and informal sector workers who need affordable and simple life cover. The plan combines a small savings element with basic protection and pays a lump sum at maturity. It follows IRDAI’s Micro Insurance Regulations, 2015, which focus on low-cost and easy-to-understand products. The entry age ranges from 18 to 55 years, and the sum assured is between ₹1 lakh and ₹2 lakh, which makes it suitable for small, structured financial support.

Is the LIC 880 plan (Jan Suraksha Plan) a term plan or an endowment plan?

LIC Jan Suraksha is not a pure term plan. It is closer to a micro endowment plan that combines basic life cover with a savings component. Unlike term insurance, it pays a maturity benefit if you survive the policy term. The structure is simple and aligned with IRDAI’s Micro Insurance Regulations, 2015. While this works for small savings needs, it does not offer strong financial protection. If your goal is income replacement or long-term security, a proper term insurance plan with higher coverage is a more suitable choice than relying only on Jan Suraksha.

What is the LIC Jan Suraksha policy premium chart by age?

Premiums under the LIC Jan Suraksha Plan vary based on age and the premium paying term. For a ₹1 lakh sum assured, a 25-year-old pays around ₹13,270 annually for a 12-year term, ₹9,015 for a 15-year term, and ₹5,800 for a 20-year term. At age 45, premiums increase to about ₹13,530, ₹9,340, and ₹6,250, respectively. These figures come from the official LIC Jan Suraksha brochure and are illustrative. Premiums rise with age because the risk of mortality increases. This makes early entry more cost-effective for long-term policyholders.

What is the eligibility for the LIC Jan Suraksha Plan?

To buy the LIC Jan Suraksha Plan, you must be between 18 and 55 years of age at entry. The policy can continue up to a maximum maturity age of 70 years. You can choose a policy term between 12 and 20 years, and the premium paying term will always be 5 years shorter than the policy term. The sum assured ranges from ₹1 lakh to ₹2 lakh. Premiums can be paid yearly, half-yearly, quarterly, or monthly. These conditions are designed to keep the plan simple and accessible for first-time buyers and low-income individuals.

What is the death benefit in the LIC Jan Suraksha Plan 880?

The death benefit under LIC Jan Suraksha is structured to provide basic financial support. The nominee receives the higher of seven times the annualized premium or the basic sum assured. In addition, the payout will never be less than 105% of the total premiums paid up to the date of death. This ensures a minimum return of premiums. The benefit can be taken as a lump sum. While this offers flexibility, the overall coverage remains limited due to the low sum assured.

What happens if I miss a premium payment in the LIC Jan Suraksha Plan?

LIC Jan Suraksha includes an auto cover feature that protects your policy if you miss a premium payment. If you have paid at least three years of premiums, your life cover continues for six months from the first missed payment. If you have completed five or more years, the cover can continue for up to two years. This feature helps prevent immediate policy lapse and gives you time to restart payments. It is useful for people with irregular income, as it maintains protection for a limited period without immediate financial pressure.

What riders are available with LIC Jan Suraksha Plan 880?

LIC Jan Suraksha offers two optional riders. The Accidental Death and Disability Rider provides a lump sum on accidental death within 180 days and a monthly payout over 10 years in case of disability. The Accident Benefit Rider covers accidental death during the premium paying term. You can add these riders only if at least five years remain in the premium-paying term. The rider sum assured cannot exceed three times the base sum assured. Also, the total rider premium cannot exceed 30% of the base plan premium. However, the plan lacks important riders like waiver of premium.

What is the surrender value of the LIC Jan Suraksha Plan, and what happens if I exit early?

Exiting the LIC Jan Suraksha Plan early can lead to a loss. There is no surrender value in the first year. After two years of premium payments, a partial surrender value becomes available, but it is lower than the total premiums paid. The value improves gradually over time. The exact amount depends on how long you stay invested and when you exit. This means the plan works best if you continue until maturity. Early surrender, especially in the initial years, significantly reduces the overall benefit.

Should I choose the LIC Jan Suraksha Plan or a private term insurance plan?

If your goal is strong financial protection, a pure term insurance plan is a better choice than LIC Jan Suraksha. The maximum cover under Jan Suraksha is ₹2 lakh, which is not enough for income replacement or major financial needs. In comparison, term plans from private insurers offer coverage of ₹1 crore or more at affordable premiums. Jan Suraksha works as a small savings plan with basic cover, but it cannot replace proper life insurance. It is better to compare pure term plans if you want meaningful long-term protection for your family.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.