ICICI Pru LifeTime Classic is a unit-linked insurance plan (ULIP) that combines investment with life insurance cover. It comes with a 5-year lock-in period, 4 portfolio strategy options, and a maturity age up to 80 years. While it offers market-linked wealth creation, ULIPs cost more than term insurance and may not provide adequate life insurance coverage.

For example, a 35-year-old pays a total premium of ₹7 lakh for a ₹10 lakh sum assured under this plan. The same person needs to pay a total premium of ₹4.07 lakh for a ₹1 crore cover of ICICI iProtect Smart Plus (7 years limited pay and coverage till 70), which results in 10x life cover at 40% less premiums. This guide discusses whether a ULIP is the correct choice for your future needs.

Want insurance that builds wealth, too? LifeTime Classic by ICICI Prudential is one such plan which offers you both life coverage and returns. But before you buy the policy, it is important to understand how this ULIP works, what it costs, and whether a term plan plus separate investing could give you better value. In the next few minutes, you will understand if the plan truly deserves a place in your financial plan.

ICICI Pru LifeTime Classic is a non-participating ULIP that aims to protect your family financially while helping you build wealth for future goals such as retirement or children's education.

The policy offers tax benefits, where premiums paid qualify for Section 80C (old regime) up to ₹1.5 lakh. However, ULIPs issued on or after 1 February 2021 can lose the Section 10(10D) exemption if the annual premium exceeds ₹2.5 lakh, and the death-benefit exception remains.

Key Features of ICICI Pru LifeTime Classic

Feature

Details

Minimum Entry Age

0 years

Maximum Entry Age

60 years for single pay and 58 years for limited/regular pay

Minimum Maturity Age

18 years for single pay and 65 years for limited/regular pay

Maximum Maturity Age

80 years for single pay and 70 years for limited/regular pay

Premium Payment Mode

Single, yearly, half-yearly, and monthly

Policy Term for Limited and Regular Pay

70 years minus age at entry (0 to 45 years) and 65 years minus age at entry (46 to 58 years)

Premium Payment Term

Single pay, limited pay (7 to 30 years) and regular pay (7 to 30 years)

Fund Options, NAV History, and Returns

ICICI Pru LifeTime Classic offers policyholders a choice of fund options, which include:

Core Equity Funds: These funds focus on long-term wealth creation through diversified stock exposure.

Hybrid and Balanced Funds: These combine equity and debt to create a smoother investment experience.

Debt and Liquid Funds: These funds focus on capital stability and lower risk.

Index, Factor, and Thematic Funds: These follow market indices, investment factors, or sector themes.

Net Asset Value (NAV) is the value at which units in your ULIP fund are bought or sold. In ICICI Pru LifeTime Classic, the NAV is declared daily on business days and changes based on market performance. A rising or falling NAV does not indicate guaranteed gains or losses on its own. It reflects how the underlying investments are performing at that point in time.

However, ICICI Pru LifeTime Classic does not have a single net NAV history. Your actual returns and fund value depend on the funds selected, premium redirection choices, and any strategy changes over time.

For additional information about the funds and strategies, please refer to pages 4 to 16 of the policy brochure.

Returns for ICICI Pru LifeTime Classic

Aspect

Figures

Annual Premium

₹1,00,000

Premium Payment Term

7 years

Policy Term

35 years

Sum Assured

₹10,00,000

Projected Value at 4% Gross Return

₹11,04,389

Projected Value at 8% Gross Return

₹46,82,776

Note: Projected values are illustrative for a 35-year-old with investments in Maximiser V (fund option). The illustrative figures are based on assumptions from the ICICI Pru LifeTime Classic brochure. Actual returns are based on market performance.

As per IRDAI norms, insurers present return illustrations at 4% and 8%. However, early-year charges reduce the actual amount invested, which impacts compounding over time. Even if the underlying fund performs around 8%, the net return for the policyholder is closer to 6%.

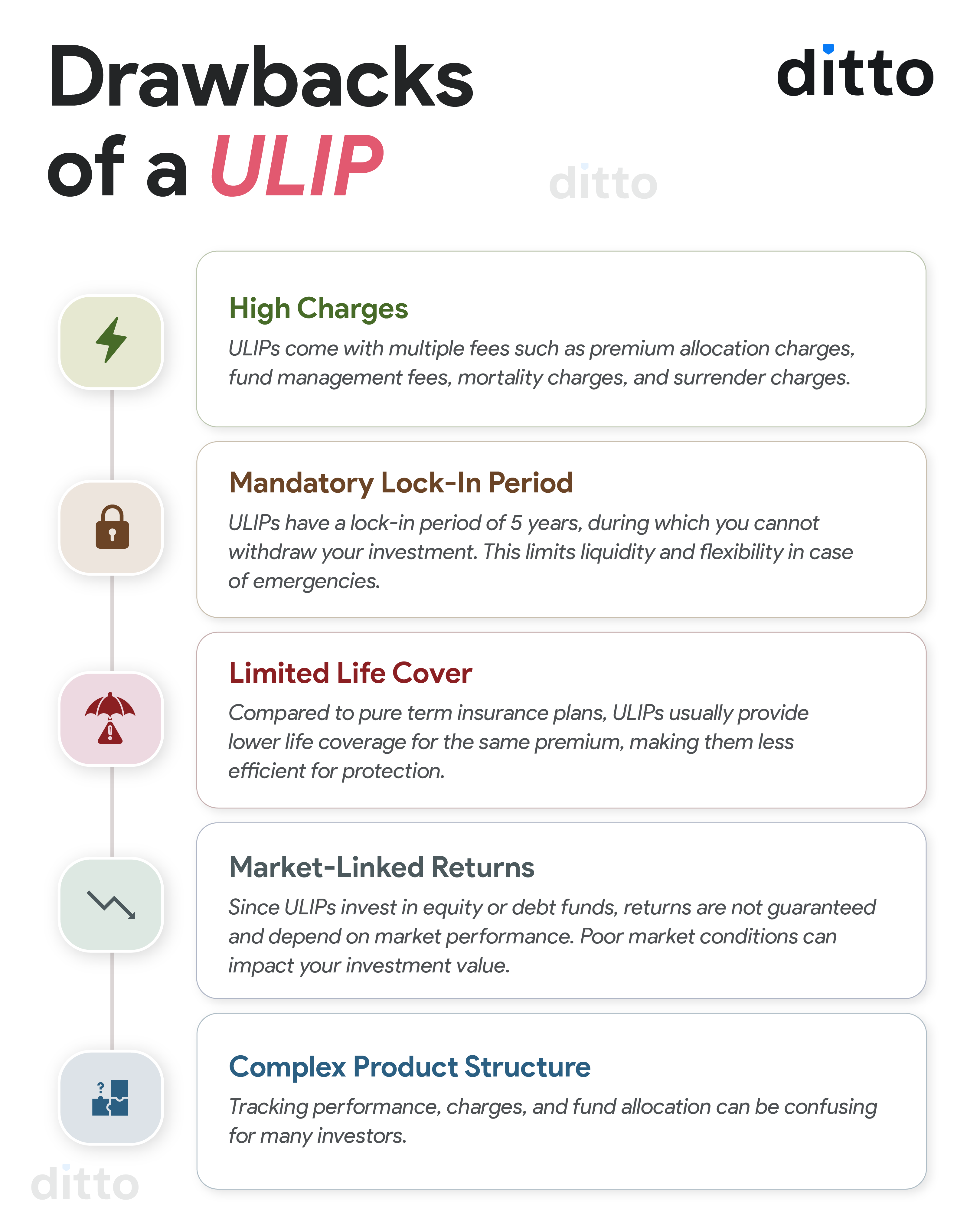

Though ULIPs offer returns on maturity, they come with several drawbacks. See the infographic below for a clear understanding.

Charges, Policy Terms, and Surrender Value

Charges of ICICI Pru LifeTime Classic

Premium Allocation Charges: These charges reduce the amount invested from your premium. They are highest in the early years and gradually reduce over time, with top-ups charged at a flat 2%, impacting early growth more.

Fund Management Charges (FMC): Most funds in this ULIP carry a charge of about 1.35% per year, which is standard for ULIPs. The Money Market Fund is lower at 0.75%, while the Discontinued Policy Fund charges 0.50%.

Policy Administration Charge: This is a recurring charge on your policy. For regular and limited pay, it starts lower in the first five years and increases later, capped at ₹500 per month or ₹6,000 per year. Single pay plans charge ₹60 per month in the initial five years.

Besides the above-listed charges, the policy also includes a mortality charge for life cover, deducted monthly based on age and risk, and a switch charge of ₹100 after four free switches per year, which helps limit frequent fund changes.

Policy terms show limited flexibility. Partial withdrawals apply only after lock-in and full premium payment, while top-ups stop in the last five years. The plan also offers no loan facility.

Surrender Value of ICICI Pru LifeTime Classic

During the Lock-in Period: Surrender does not give immediate access to your fund value. The amount moves to the discontinued policy fund after applicable charges. Risk cover stops, and money stays invested until the lock-in ends or death occurs. The fund earns around 4% p.a. with a 0.50% FMC.

After the Lock-in Period: The process becomes much simpler. The surrender value equals your fund value, including any top-ups. Once paid out, the policy ends completely.

Discontinuance Charge Pattern: Charges remain higher in early years and reduce gradually. They become nil from policy year 5 onward.

Exit within 5 years feels restrictive and costly. After 5 years, surrender turns into a simple fund value decision, which many customers overlook.

Should You Continue or Surrender LifeTime Classic?

Do not continue only because you have already paid a lot. Ask yourself one honest question: If this policy were offered to you today for the remaining term, would you still buy it? That question often brings real clarity.

Your Policy Continues to Make Sense When:

You are past the costly early years, and your goal is long-term, around 10 years or more.

You prefer one product for insurance and investing, and the current fund strategy still suits you.

You can Exit Your Policy if:

It was sold as guaranteed or short-term, and you dislike the fund choices or structure.

You only need life cover, and the lock-in period is over. Make sure to get adequate life cover via a term plan before exiting.

Many people exit too late or too early. The right decision depends on today’s value, not yesterday’s cost.

Note: If liquidity is the real issue, partial withdrawal may be a smarter route. It can give access to funds while keeping the policy active, subject to plan rules.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

Backed by Zerodha

Dedicated Claim Support Team

100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

ICICI Pru LifeTime Classic suits long-term investors comfortable with market-linked ULIPs. It may also work for those who cannot get a term plan due to health or occupation risks. It fits buyers who already have term cover and want a structured, locked-in investment with combined insurance.

However, at Ditto, we do not recommend ULIPs due to the fact that their returns do not justify the cost, and that they have a complex structure. A pure term insurance plan for protection, paired with separate low-cost investments like fixed deposits, is often a more cost-effective and efficient approach.

If you are looking for a term plan from established insurers, explore our guide on the best term insurance plans.

Frequently Asked Questions

What is ICICI Pru LifeTime Classic, and how does it work?

ICICI Pru LifeTime Classic is a ULIP from ICICI Prudential that combines life insurance with market-linked investment. Your premium is split into two parts. One part provides life cover, and the rest gets invested in funds you select. The plan has a mandatory 5-year lock-in period, multiple portfolio strategies, and maturity up to age 80.

It suits long-term goals like retirement or education. It does not suit short-term saving needs or those who want pure risk protection without market exposure.

What are the charges in the ICICI Pru LifeTime Classic plan?

ICICI Pru LifeTime Classic has multiple-layered charges, and they are complex in nature. Premium allocation charges reduce the amount invested, especially in early years. Fund management charges are about 1.35% annually for most equity funds. Policy administration charges can go up to ₹500 per month or ₹6,000 per year.

Mortality charges apply monthly based on age and cover. Switch charges apply after four free switches per year at ₹100 per switch. These charges reduce net returns and impact long-term compounding significantly.

What is the lock-in period for ICICI Pru LifeTime Classic?

The lock-in period for ICICI Pru LifeTime Classic is 5 years as per IRDAI rules for ULIPs. During this period, you cannot withdraw or surrender the policy. If premiums stop within these 5 years, your ICICI Pru LifeTime Classic fund value moves to the Discontinued Policy Fund. The risk cover also stops.

The DPF earns a minimum return of around 4% per year with a 0.50% fund management charge. You can access money only after a lock-in or in case of death.

How do I check my ICICI Pru LifeTime Classic policy status or fund value?

You can check your ICICI Pru LifeTime Classic policy status online through the ICICI Prudential Life website. Log in using your policy number or registered mobile number. Go to the fund value or policy statement section to view details. You will see premiums paid, fund allocation, units, and current value.

You can also download unit statements or contact customer support for updates or any kind of policy change. This helps you track performance and understand how your investments are growing over time.

How to check ICICI Pru LifeTime Classic NAV history?

ICICI Pru LifeTime Classic does not have one NAV because it uses multiple funds. Each fund has its own daily NAV. For example, equity funds and debt funds show different NAV movements.

You can check individual fund NAV history on the ICICI Prudential official website under fund performance. Your overall returns for the policy depend on which funds you chose and the number of switches you made. So your policy performance is personalized and not based on a single NAV.

What happens if I stop paying premiums in ICICI Pru LifeTime Classic before 5 years?

If you stop paying premiums for your policy in the 1st 5 years, the policy moves into discontinuance mode. Your fund value goes to the Discontinued Policy Fund after charges. Life cover ends immediately.

The discontinued policy fund earns around 4% per year with a 0.50% fund management charge. You cannot withdraw money during a lock-in. It becomes accessible only after the lock-in period or in case of death. Early exit usually leads to lower value, so timing plays a major role.

Is the maturity amount from ICICI Pru LifeTime Classic taxable?

Maturity proceeds are generally tax-free under Section 10(10D) of the Income Tax Act, 1961. However, if the total annual aggregate premium exceeds ₹2.5 lakh (across all ULIPs held), maturity gains become taxable as capital gains under the current rules.

Premiums up to ₹1.5 lakh qualify for deduction under Section 80C in the old tax regime. The death benefit paid to nominees remains fully tax-free. Tax treatment depends on premium size and policy structure, so planning matters.

What is the free look period for ICICI Pru LifeTime Classic, and how do I cancel it?

ICICI Pru LifeTime Classic offers a 30-day free look period from policy receipt. You can cancel within this period if you are not satisfied. The insurer refunds the premium after deducting stamp duty, medical tests (if any) and mortality charges for the days covered. These are standard deductions across ULIPs.

You need to submit a cancellation request to your insurer with the correct policy documents. You can do this through customer care or a branch visit for a clean exit.

How do I log in to the ICICI Pru LifeTime Classic account?

You can access your ICICI Pru LifeTime Classic login by visiting the ICICI Prudential Life Insurance website or mobile app and using your registered mobile number, email ID, or policy number. If you face any issues while logging in to your account, reach out to customer support.

After entering the one-time password (OTP), you can view your fund value, units, premium status, and statements in one place. If you are a first-time user, you must complete quick registration. This login helps you track NAV-based fund performance and manage your ULIP easily anytime.

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.