Overview

A guaranteed return plan offers certainty, not market-driven growth. These non-linked, non-participating life insurance plans lock in your maturity, survival, or income benefits from day one, giving complete visibility into future payouts.

In the next few minutes, we'll break down how guaranteed return plans actually work, the returns you can realistically expect, the tax rules, and how they compare with other investment options.

What Is a Guaranteed Return Plan?

A guaranteed return plan offers certainty. You know the payout amount at the time of purchase, making it appealing for investors who value predictability over aggressive growth.

Guaranteed Income Plan

Instead of a single maturity payout, you receive a stream of guaranteed income at regular intervals. Depending on the plan, income may start immediately, after a deferment period, or continue for life. Some variants also return premiums or provide a maturity benefit alongside the income stream.

Guaranteed Savings Plan (Lump Sum)

You pay premiums for a fixed period and receive a predefined lump sum at maturity. These plans are commonly used for long-term goals such as children's education, retirement corpus creation, or legacy planning, where capital certainty matters more than maximizing returns.

Examples: SBI Life Smart Platina Supreme, HDFC Life Guaranteed Income Insurance Plan, and ICICI Pru Guaranteed Income For Tomorrow.

How Does a Guaranteed Return Plan Work?

Here’s how a guaranteed return plan works and what’s included in the process:

- Premium Payment Term (PPT): This is the period during which you pay premiums. Most guaranteed return plans follow a limited-pay structure, so you may pay for 5, 10, or 12 years while the policy continues for much longer.

- Policy Term (PT): The policy remains active for the entire policy term, which could be 15, 20, or even 30 years. Your benefits are linked to this overall duration, not just the premium-paying period.

- Guaranteed Benefit Accumulation: Over time, the policy builds value through guaranteed additions and, in some cases, loyalty additions. These benefits are predefined and help increase the final payout.

- Maturity or Income Payout: At the end of the policy term, you receive either a guaranteed lump sum or a guaranteed income stream, depending on the option selected at the time of purchase.

- Death Benefit Protection: If the life assured passes away during the policy term, the nominee receives the death benefit. This ensures financial protection for the family while the savings component continues to serve its purpose.

- Loan Facility for Liquidity: Most non-linked guaranteed plans allow policy loans once a surrender value is acquired. This provides access to funds without surrendering the policy and disrupting long-term benefits.

Note: While guaranteed plans offer fixed policy benefits, they should not be viewed as completely risk-free in the same way as bank Fixed Deposits (FDs). Bank FDs are protected by RBI’s DICGC insurance (deposit insurance) up to ₹5 lakh per depositor per bank. GRP guarantees depend on the insurer's financial strength, IRDAI's regulatory oversight, and mandatory solvency requirements.

Returns, Charges, and Real IRR

Guaranteed return plans deliver stable payouts because insurers invest primarily in government securities and high-quality bonds to support long-term guarantees. Since these assets typically yield around 6.5% to 7.5%, the final policy Internal Rate of Return (IRR) for most investors usually falls in the 5% to 6.5% range after costs. While some illustrations may show higher returns, those often assume ideal conditions such as a young age, a large premium, and a long policy term.

Unlike ULIPs, guaranteed plans do not separately disclose charges such as commissions, administration costs, mortality costs, or insurer margins. These expenses are already built into the product pricing. As a result, the most reliable way to evaluate a guaranteed plan is through its IRR.

Note: If you wish to compute the real return from a guaranteed plan, focus on the IRR rather than the maturity amount alone. Use the benefit illustration of your policy and list every premium paid as a cash outflow and every benefit received as a cash inflow, then calculate the IRR. Use Extended Internal Rate of Return (XIRR) when cashflows occur on different dates, and IRR only when they are evenly spaced each year. This gives the most accurate picture of your actual return.

Tax Benefits and Lock-In Rules

Note: For traditional non-linked life insurance policies issued on or after April 1, 2023, the combined annual premium across all such policies should not exceed ₹5 lakh to preserve tax-free maturity benefits.

Who Should Buy a Guaranteed Return Plan?

- Suitable for investors who prefer certainty and would otherwise keep money in long-term fixed deposits rather than market-linked products.

- Works best for high-income individuals who have already exhausted options like Public Provident Fund (PPF), Employees’ Provident Fund (EPF), and National Pension System (NPS), and want an additional maturity tax-efficient fixed-return avenue.

- Useful for those seeking a guaranteed future income stream, especially for retirement planning, without worrying about market fluctuations.

- Can support estate and legacy planning where life cover and nominee-focused wealth transfer are important priorities.

- Ideal for people who struggle to stay invested during market volatility and benefit from a disciplined, long-term savings structure.

However, such plans may not be suitable for investors seeking high growth, liquidity, or inflation-beating returns through equities and mutual funds. They also fall short as a primary life insurance solution, since the life cover is typically limited to around 10 times the premium, far lower than what the same amount can secure through a term insurance plan. Investors with a long investment horizon and some tolerance for market fluctuations may find diversified equity investments more rewarding over time.

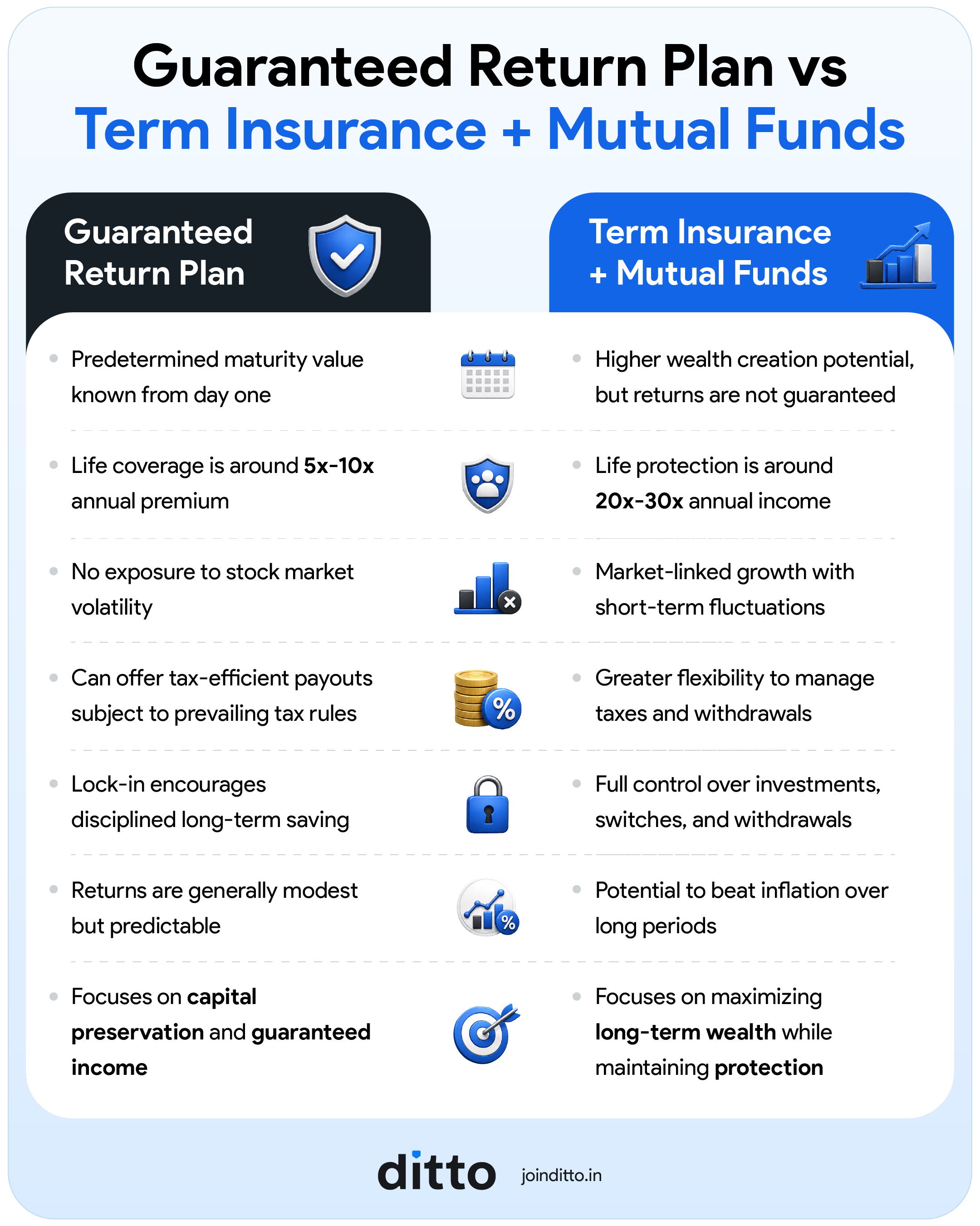

Guaranteed Return Plan vs. Term Plus Mutual Funds

Guaranteed return plans and the term plan plus mutual fund approach solve very different problems. One prioritizes certainty, predictable payouts, and disciplined long-term saving, while the other focuses on maximizing protection and long-term wealth creation through market-linked investments.

Let’s see how the returns work out for the two options.

Sample Premiums

Note: The illustrative values with guaranteed additions are for a 35-year-old. The figures are sourced from the LIC Bima Jyoti brochure. The person invests ₹79,309 for 15 years for an estimated IRR of about 4%. The same money invested in an affordable high-cover term plan with separate mutual fund investments can prove to be more effective.

Key Insights:

- A LIC Bima Jyoti policyholder pays ₹79,309 annually for 15 years and receives a guaranteed maturity benefit of about ₹20 lakh after 20 years, translating to an estimated IRR of roughly 4%.

- An alternative approach is to buy a low-cost term plan (around ₹12,000 annually for ₹1 crore) and invest the remaining ₹67,309 in mutual funds.

- At an assumed modest 6% annual return, the debt mutual fund corpus can exceed ₹22 lakh. At 8% or higher, the wealth gap widens significantly.

- The term insurance route can also provide substantially higher life cover than the insurance component within Bima Jyoti.

- The trade-off is simple: Bima Jyoti offers certainty and discipline, while term insurance plus mutual funds offers higher protection, greater flexibility, and potentially stronger long-term wealth creation for investors comfortable with market risk.

See the infographic below for an understanding of how the options trade off.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 24,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat over WhatsApp with our advisors.

Conclusion

A guaranteed return plan can be a useful tool when your priority is certainty, predictable cash flows, and disciplined long-term saving. However, the real decision should be based on the plan's IRR, surrender value, tax treatment, liquidity constraints, and your ability to stay invested until maturity.

Before investing, compare them with alternatives like Public Provident Fund (PPF), Employees' Provident Fund (EPF), bank FDs, and high-quality corporate FDs, which may offer similar or better risk-adjusted returns. Most importantly, never use a life insurance plan as an emergency fund. Emergency money should remain accessible through savings accounts, bank FDs, or liquid mutual funds, where liquidity is available when you actually need it.

Use guaranteed plans for stability, not aggressive wealth creation. For pure financial protection, term insurance remains the most efficient choice. For long-term wealth building, compare the opportunity cost against mutual funds and other market-linked investments. For short-term capital preservation, fixed deposits and high-quality debt instruments may be more suitable alternatives.

If you wish to explore some comprehensive term plans, refer to our guide on the best term insurance plans in India.

Frequently Asked Questions

Last updated on: