Quick Overview

What if one plan could grow your money and also provide life cover? The ABSLI Fortune Wealth Plan aims to do exactly that. It combines market-linked investments with insurance, but the real picture depends on how costs, features, and structure come together in practice.

This guide walks you through the ABSLI Fortune Wealth Plan review, including ULIP features, charges, death benefits, and key drawbacks.

What Is the ABSLI Fortune Wealth Plan?

The ABSLI Fortune Wealth Plan is a non-participating ULIP that combines life insurance with market-linked investments. It offers multiple fund options across assets, along with tax benefits under applicable laws.

Fund Options, Investment Strategies & Key Features

The ABSLI Fortune Wealth Plan offers 18 funds across debt, hybrid, and equity categories. You get options such as index, large-cap, and small-cap funds, which offer further flexibility.

The plan includes 5 investment strategies, which include options like the “Systematic Transfer” option, which helps you enter equity gradually and reduces timing risk, while “Return Optimiser” locks in gains during volatile phases but can limit upside in strong markets.

For more information about the funds offered, see pages 6 to 8 of the policy brochure.

Key Features of ABSLI Fortune Wealth Plan

Benefits, Charges & How Returns Are Calculated

Benefits of ABSLI Fortune Wealth Plan

- Death Benefit Structure: Under the Classic option, the death benefit paid to nominees will be the higher of the fund Value or the sum assured on the date of death. Under the Assured option, the nominee receives an immediate payout, and the policy continues till maturity.

- Maturity Benefit: If you survive the policy term, you receive the full fund value at maturity. The final payout depends on market performance, so returns are not guaranteed but reflect the performance of your chosen funds over time.

- Guaranteed Additions: The plan adds extra units at defined intervals based on your fund value and premium band. These additions increase the overall fund value and reward long-term continuation of the policy.

- Liquidity & Flexibility: You can withdraw a partial amount after 5 years without any charge, subject to limits. There is also an option to receive maturity proceeds in installments, which can help with planned cash flows instead of a lump sum.

Note: Under the Classic option, the payout cannot be lower than 10 times the annualized premium, adjusted for any partial withdrawals, and it cannot be lower than 105% of the total annualized premiums paid. However, the sum assured can be reduced by any partial withdrawals made during the two years immediately before death. This means that large withdrawals near the claim event may significantly reduce the final death benefit payable.

Charges of ABSLI Fortune Wealth Plan

Premium Allocation Charge

This charge is higher in the initial years and reduces over time. It directly affects how much of your premium is invested, so early returns may feel lower due to upfront deductions.

Fund Management Charge (FMC)

This is charged across all funds and adjusted to NAV daily. Equity-oriented funds usually have higher charges, which can affect long-term returns if not monitored.

Policy Administration Charge

This is applied as a fixed or percentage-based charge in the early years, depending on your premium band. It reduces or becomes negligible in later years, which improves cost efficiency over time.

In addition to the above-listed charges, the plan includes discontinuance and mortality charges. However, fund switches and partial withdrawals are free.

As per IRDAI rules, insurers show return illustrations at 4% and 8%. In reality, charges in the early years reduce the amount that gets invested, which weakens compounding. So even if the fund delivers around 8%, the actual return often stays closer to 6%.

Premiums and Returns for ABSLI Fortune Wealth Plan

Note: Projected values are illustrative for a 35-year-old and based on assumptions from the ABSLI Fortune Wealth Plan brochure. Actual returns are not guaranteed and are based on market performance.

Should You Invest? Pros, Cons & Honest Verdict

The plan offers a wide range of fund choices across debt, hybrids, and equity, which provides real flexibility. The Assured Option stands out because it provides an immediate payout while still building a maturity corpus for the nominee.

However, the charge structure is relatively high, especially in the early years, so a smaller portion of your premium is invested. The life cover is fixed at 10 times the annualized premium, so a ₹1 lakh yearly premium gives ₹10 lakh cover. In comparison, a standalone term plan usually targets 20 to 30 times annual income, which for most earners is far higher and more practical for family protection. If you are looking for a term plan, go through our guide on the best term insurance plans.

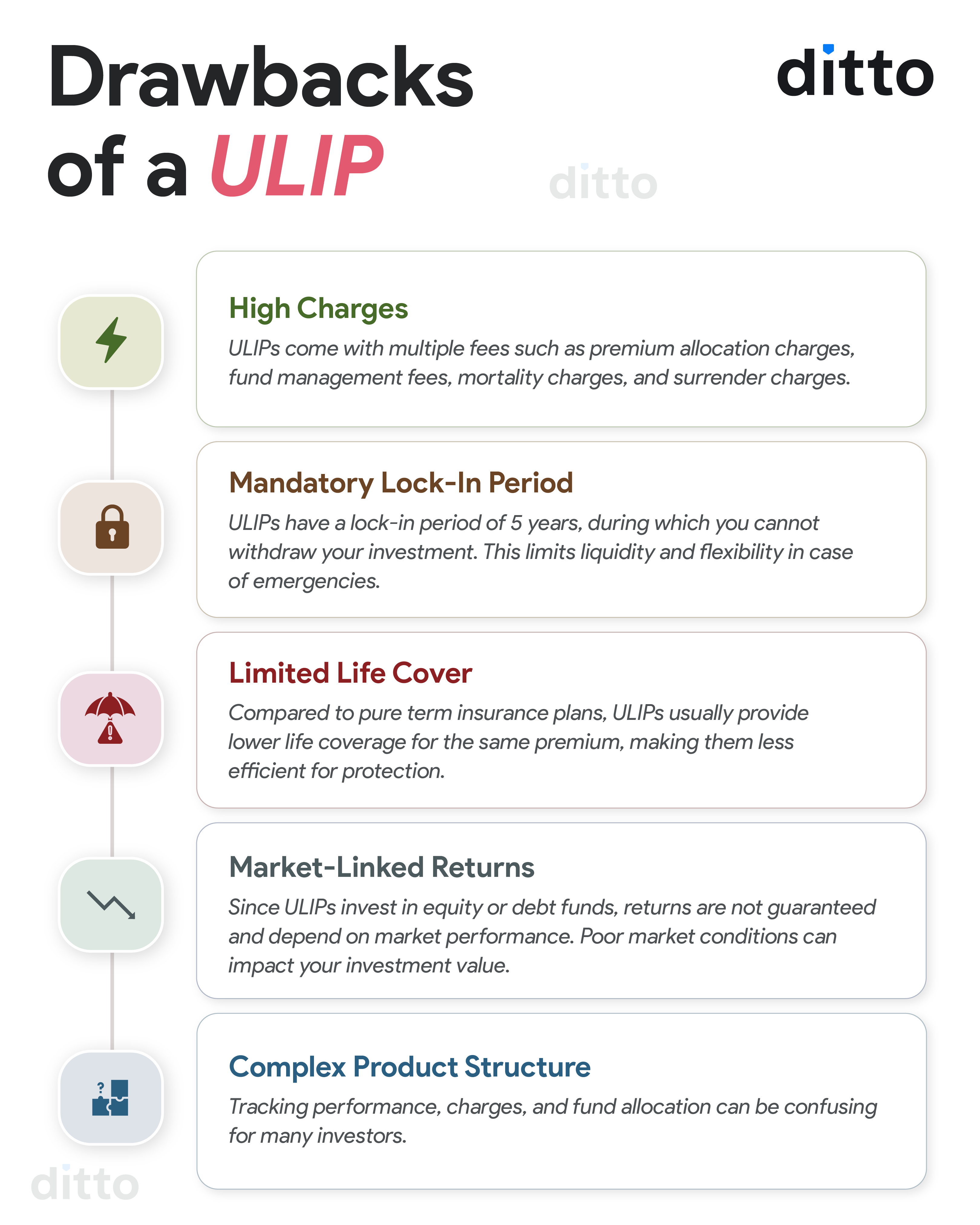

Check out the infographic for a clear understanding of the plan's drawbacks.

Should You Invest in ABSLI Fortune Wealth Plan?

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat over WhatsApp with our advisors.

Conclusion

ABSLI Fortune Wealth Plan is a decent ULIP plan fit for long-term investors and those comfortable with market-linked products. The plan should be your last resort, depending on insurance eligibility and investment preferences.

- Individuals who face rejection for term plans due to medical conditions or high-risk occupations. In such cases, insurers can offer ULIP plans, as they typically have a lower sum assured.

- People with adequate term insurance who want an additional combined investment and insurance product.

- Investors who value structured, long-term investing with a mandatory lock-in period.

If you wish to purchase a term plan from Aditya Birla Life, you can explore Aditya Birla Sun Life Super Term Plan.

Frequently Asked Questions

Last updated on: