Quick Overview

Many Indians trust the Post Office because it’s deeply embedded in everyday life and accessible almost everywhere. This reach includes 650+ IPPB branches, over 1.36 lakh post office access points, and nearly 2 lakh postal staff delivering services at the last mile. But when it comes to health insurance, the Post Office does not offer its own plans. Instead, it helps customers buy policies from private insurers.

So, if you're also planning to buy health insurance through this medium, here’s everything you need to know.

Coverage Offered Under Post Office Health Insurance

India Post Payments Bank (IPPB) acts as a Corporate Agent (IRDAI CA0574) and distributes health insurance policies issued by private insurers. The coverage you receive depends entirely on the insurer and plan chosen, not the Post Office itself.

According to IPPB’s official product listings, the current partner insurers are Tata AIG and Bajaj General Insurance. Availability may vary by state, branch, and campaign.

- Offers comprehensive hospitalisation cover along with 540+ day-care procedures.

- Includes restore benefit, global cover, bariatric surgery cover, consumables, and vaccination benefits.

- Covers up to 7 family members under a single policy.

- Comes with lifelong renewability and a cumulative bonus for claim-free years.

- Applies standard waiting periods for listed illnesses and pre-existing diseases.

- Allows entry from 91 days for children and 18 years for adults, with a maximum entry age of 45 years.

- Offers in-patient hospitalisation cover with no room rent limits.

- Includes pre- and post-hospitalisation cover for 60 and 90 days respectively.

- Covers day care procedures, organ donor expenses, ambulance charges, and AYUSH treatment.

- Provides a sum insured reinstatement benefit.

- Available with sum insured options from ₹1 lakh to ₹5 lakh.

- Comes with standard waiting periods for pre-existing and specific diseases.

- Covers self and spouse aged 18 to 65 years, and dependent children from 3 months to 25 years.

- Does not require medical tests for entry for individuals below 65 years of age.

Note

Post Office Health Insurance 755 Plan Details

India Post Payments Bank, in association with insurance companies, offers a personal accident insurance scheme with coverage of ₹10 lakh and ₹15 lakh, with annual premiums starting from ₹520 and going up to ₹755. This Post Office health insurance 755 plan includes accidental death, permanent and partial disability, hospitalization cash, and accident-related medical expenses.

Eligible IPPB savings account holders aged 18–65 can enrol digitally within minutes using biometric authentication through postmen. The plan also offers education and marriage assistance for children, funeral expenses, and covers accidents such as road accidents, snake bites, and lightning strikes.

Post Office Health Insurance 899 Plan Details

India Post Payments Bank, in partnership with Niva Bupa, offers a low-cost ₹15 lakh top-up health insurance plan starting at ₹899 per year for individuals (₹1,399 for two adults, ₹1,799 for two adults + one child, ₹2,199 for two adults + two children). It’s available for ages 18–60, and children can be included from 91 days old. The plan has a ₹2 lakh deductible that must be met out of pocket or with another base policy.

If you want to learn more about how top-ups and super top-ups work in health insurance, refer to the linked article.

Notes

Benefits of Buying Post Office Health Insurance

Offline Access

Reputed Insurers

Assistance for Customers

Standardised Premiums

Limitations and Exclusions Under Post Office Health Insurance

- IPPB primarily provides banking services, with insurance offered only as a commission-based add-on. As a distributor, the Post Office does not underwrite policies or handle claims, so product depth and long-term insurance advisory are not its primary focus.

- Since only partner insurer plans are available, your choice is limited, and you may miss better policies available elsewhere in the market.

- Many affordable micro-plans offer limited coverage with lower sum insured options, room rent restrictions, sub-limits, and longer waiting periods. Suitability assessment is basic, and agents may not evaluate specific needs, such as pre-existing diseases, maternity requirements, chronic conditions, hospital preference, or family medical history.

- Claims are handled entirely by the insurer or TPA, so the post office cannot escalate or resolve disputes end-to-end.

- Waiting periods and standard exclusions (self-harm, cosmetic procedures, etc.) also apply. Check out the linked article to understand what post office health insurance schemes generally do not cover.

How to Apply for Post Office Health Insurance

- Visit your nearest Post Office or India Post Payments Bank (IPPB) branch to apply offline.

- An IPPB agent, postman, or Gramin Dak Sevak will help you select a plan, fill in the proposal form, and complete biometric authentication if required.

- After submitting the application and making the payment, the policy is issued directly by the insurer and shared digitally or in physical form, depending on the plan.

- Post Office health insurance plans usually require minimal paperwork. For a detailed list of required documents, you can refer to the linked guide.

Note

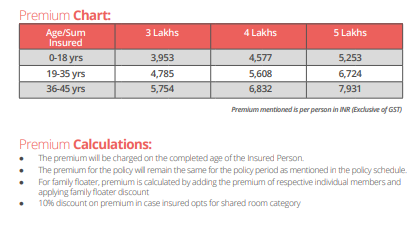

Premium Calculation for Post Office Health Insurance

The premium you pay for Post Office health insurance depends on multiple factors decided by the insurer, not the Post Office or IPPB. Key factors typically include age, location, sum insured, number of people covered, policy tenure, and medical history.

To get an idea about the premium amounts you may have to shell out for post office health insurance schemes, check this illustrative sample taken from the TATA AIG Medicare brochure.

Note

Claim Process for Post Office Health Insurance

Claims under Post Office health insurance are handled entirely by the insurer or its TPA. Depending on the hospital and situation, you can opt for a cashless claim at a network hospital or file a reimbursement claim after paying the bills upfront. Claim settlement timelines and documentation requirements vary by insurer and policy terms.

For a detailed, step-by-step explanation of cashless vs reimbursement claims and time limits for filing them, read the linked guide.

Tax Benefits on Post Office Health Insurance

Premiums paid for Post Office health insurance policies qualify for tax deductions under Section 80D of the Income Tax Act, 1961, subject to the applicable limits under the Old Tax Regime. You can claim separate deductions for premiums paid for yourself, your family, and your parents, with higher limits available if parents are senior citizens.

Who Should Consider Buying Post Office Health Insurance?

- First-time health insurance buyers who prefer an offline, assisted purchase experience through a trusted and familiar channel.

- Individuals in rural or semi-urban areas who value doorstep support via postmen or IPPB agents.

- Customers looking for basic or supplementary coverage or are comfortable comparing plan features with insurer-issued policies.

Why Talk to Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Abhinav below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation here. Slots are filling up quickly, so be sure to book a call now or chat with us on WhatsApp.

Ditto’s Take

Buying health insurance via the post office is convenient, but remember, IPPB only distributes the policy, while the insurer controls coverage, pricing, and claims. Micro or partner-linked plans may look affordable, but long-term continuity and suitability need careful evaluation.

Disclaimer

Frequently Asked Questions

Last updated on: