Overview

You buy a ₹10 lakh health plan today. Ten years from now, that same plan probably won't cover your costs for a week in a good hospital. Medical inflation in India is increasing rapidly at 12%-14%, and an unchanging sum insured quietly loses value every single year you don't upgrade it.

This is exactly where the cumulative bonus in health insurance steps in. It is your insurer's way of growing your cover for free, simply by staying claim-free or by renewing your policy. But not all bonuses are equal.

In this article, we will cover the most popular cumulative bonus add-ons in the market, what they actually offer, and which base plans already come with strong bonus growth. By the end, you will know exactly what to look for before you buy or renew your policy.

What Is a Cumulative Bonus in Health Insurance?

Ditto’s Take: We always recommend an increase in sum insured over a premium discount. A bigger cover protects you against rising medical bills. A discount only saves you a few rupees today.

Now that we know how the cumulative bonus works, let’s have a look at some popular plans that offer it as an add-on.

Care Supreme With Cumulative Bonus Super and Cumulative Bonus Booster

Care Supreme's base plan gives you a 50% bonus every year, up to 100% of your SI built-in. This is given irrespective of claims. Now the plan has 2 add-ons, namely:

- Cumulative Bonus Super: This add-on provides an additional bonus by adding 100% of your sum insured each year, up to a maximum of 500%.

- Cumulative Bonus Booster: This add-on pushes the bonus even higher, letting your cover accumulate 100% of SI annually without an upper cap, as long as you renew without a break.

Note: Both the add-ons keep your bonus intact even if you make a claim. You can opt for any one of them at the time of purchase. Moreover, you can opt to switch between the two options at renewals, which is subject to underwriting, and the already accumulated bonuses will be adjusted accordingly.

Let’s understand how the premiums look for some common profiles:

Note: A stands for adult and C stands for child. The premiums are calculated for a ₹15 lakh SI for healthy individuals residing in Delhi (110010). These are indicative values and may vary by age, location, underwriting, and medical conditions.

Ditto’s Take: The Cumulative Bonus Booster offers better coverage but at a higher cost. So based on your profile and family structure, you can choose one of the add-ons.

ICICI Elevate Power Booster Add-On

The Power Booster add-on under the ICICI Lombard Elevate plan gives you a guaranteed 100% cumulative bonus every single year, with no upper limit. This is on top of the base plan's built-in bonus, which increases your cover by 20% each year, up to 100%. Both bonuses are given irrespective of claims.

This add-on is not available if you opt for the unlimited sum insured option. Here is the sample premium breakup for this add-on.

Note: A denotes adult and C denotes child in this table. We have calculated these premiums for a ₹15 lakh sum insured, for healthy individuals residing in Delhi (110010). Your actual premium can vary depending on age, location, underwriting, and medical history.

Ditto’s Advice: The annual cost of the add-on is not very significant. Since the base plan offers a lower bonus, it is advisable to take the add-on along with a sufficient SI.

Tata AIG Medicare Select Super Charge Bonus Rider

Tata AIG Medicare Select Super Charge Bonus rider adds 100% of your base sum insured at every renewal, regardless of past claims. The cover is capped at a 300% or 500% of the base sum insured. Once you hit the cap, the bonus stops growing, but everything accumulated so far stays protected even if you claim it.

The base plan offers the option to choose between a 50% no-claim bonus up to 100% of the SI or a 1% discount, which can be availed on renewal premiums. Hence, adding the Super Charge Bonus rider makes the policy ready for long-term coverage.

Note: In this table, A is for adult and C is for child. The premiums shown are for a ₹15 lakh sum insured and are calculated for healthy individuals in Delhi (110010). These are approximate values, and the actual premium depends on age, location, underwriting, and medical conditions.

Ditto’s Observation: The cost of the add-on is very minimal, making it an even stronger point to include in the base policy, since by default the plan only offers a no-claim bonus, which will be reduced in the event of a claim.

Star Super Star Bonus

Star Health Super Star plan has an in-built no-claim bonus of 50% per year, capped at 100%. The Super Star Bonus add-on (also called the Guaranteed Bonus) provides a 100% bonus each year, with no cap. This will be given irrespective of claims. Note that this add-on is not available if you opt for unlimited sum insured.

Here’s how the add-on costs look:

Ditto's Observation: This add-on costs very little, so it's an easy buy. Normally, your no-claim bonus only drops if you make a claim, and even then, only the bonus tied to that claim gets reduced at renewal. But since your bonus can still take a hit, it's worth paying a small amount extra to protect it.

Which Plans Offer a High Built-In Cumulative Bonus

If you would rather not pay extra for an add-on, a few plans already include strong bonus features in the base policy.

HDFC Optima Secure Plus

Optima Secure Plus comes with the Infinity Benefit built in. Your cover doubles instantly on day 1 (Secure Benefit), then grows by 100% of your base sum insured each year after that, with no cap and no conditions tied to claims.

For example, a ₹15 lakh cover becomes ₹30 lakh from day 1, and with the infinite bonus, it continues to increase by ₹15 lakh every year, irrespective of claims.

Aditya Birla Activ One Max

Activ One Max offers the Super Credit feature, which gives you a 100% cumulative bonus every year, capped at 500% of your sum insured, maximum up to ₹3 crore, whichever is lower. This is built-in, given irrespective of claims made.

Niva Bupa ReAssure 2.0

ReAssure 2.0 doesn't use the word "bonus" exactly, but its Booster+ benefit offers the same benefit. Unused sum insured carries forward each year. For a ₹20 lakh base, here's what the bonus looks like across variants:

Ditto’s Observation: Unlike a guaranteed cumulative bonus, Booster+ only carries forward the sum insured you didn't use. In years with high claims, the carry-forward is proportionally smaller. It rewards low-claim years rather than guaranteeing fixed annual growth.

Key Insight

Unlimited Sum Insured

Some plans skip the bonus model entirely and offer unlimited health insurance coverage instead. This shows up in the following forms:

- Unlimited Cover From Day 1: Your sum insured has no fixed ceiling. Right from the start of your policy, you can claim up to any amount. Plans like Niva Bupa ReAssure 3.0 and ICICI Lombard Elevate offer this option.

- An Unlimited Cover Usable Once or Twice in the Policy’s Lifetime: You get unlimited coverage for a claim, but only for one or two such claims across the policy's life, not every year. For instance, HDFC ERGO Optima Secure Plus offers the “Limitless” add-on for 1-2 claims, each of an unlimited amount, based on the chosen SI.

Each works differently, so it's worth checking which version a plan actually offers before assuming "unlimited" means the same thing everywhere.

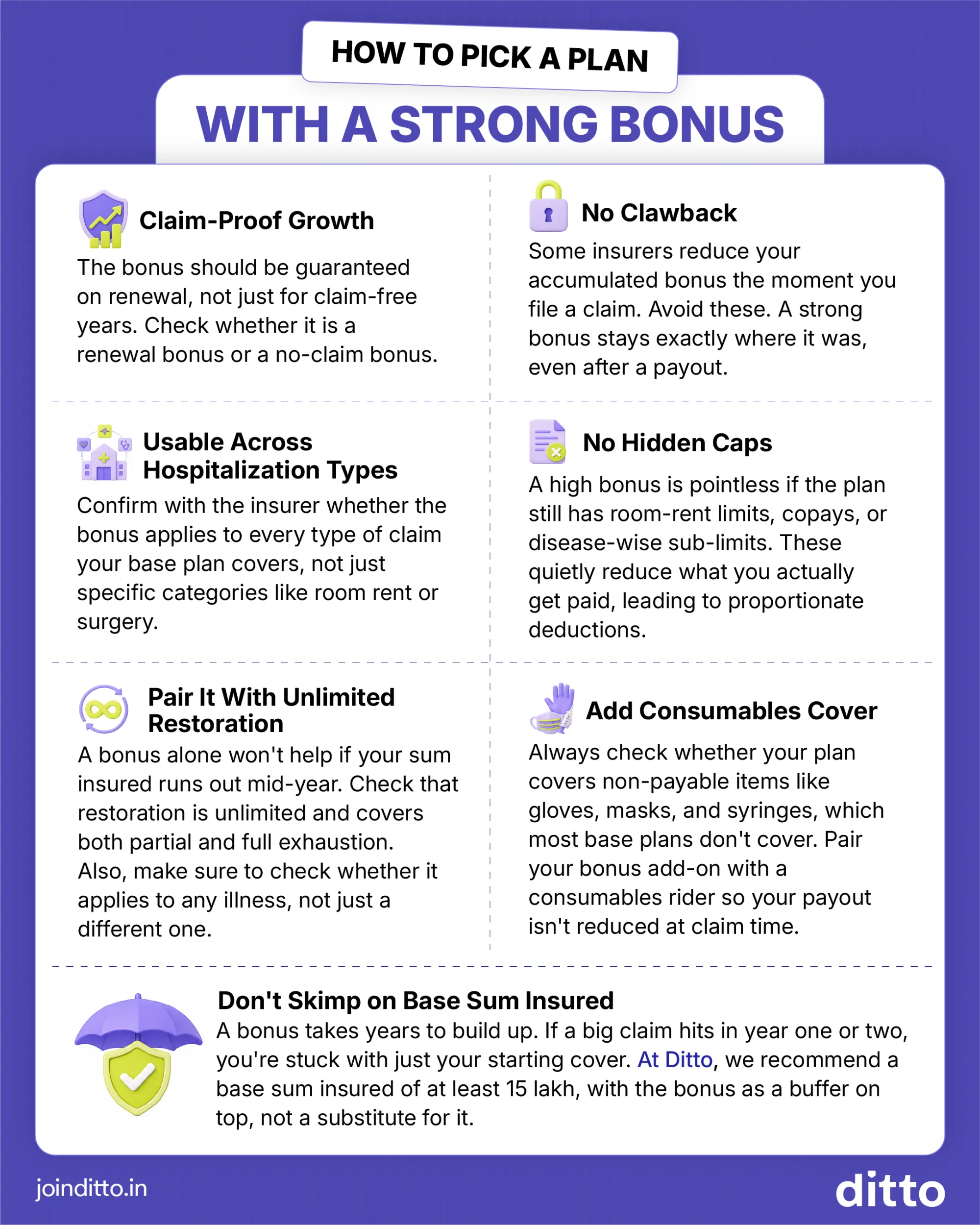

How to Pick a Plan With a Strong Bonus

Have a look at the infographic below to understand how to choose a plan with a strong bonus:

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 24,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call now or chat with our advisors on WhatsApp.

Conclusion

A cumulative bonus is a great way to grow your coverage for free, but it's still just one piece of the puzzle. The real question is whether the plan behind that bonus holds up when you actually need to make a claim.

Before you lock in a plan for the bonus alone, look at the bigger picture. Check the insurer's claim settlement track record, restoration benefits, room rent limits, copay clauses, and consumables coverage. A plan with an unlimited bonus but a weak claims process or a low base sum insured won't serve you well when a real medical emergency hits.

Bottom Line: If you already have a policy, take five minutes to check what kind of cumulative bonus it offers, whether it's a guaranteed bonus or one that resets on a claim. If you're still exploring your options, check out our guide to the best health insurance plans in India to compare across insurers on all fronts, not just the bonus.

Frequently Asked Questions

Last updated on: