Quick Overview

Health insurance premiums can often feel confusing, especially when prices differ based on age, location, and coverage limits. A premium chart makes this easier to understand by clearly showing how insurers price their plans.

In this blog, we break down the ICICI Lombard Health Insurance premium chart PDFs, explain what affects your premiums, and guide you on how to estimate costs using these documents.

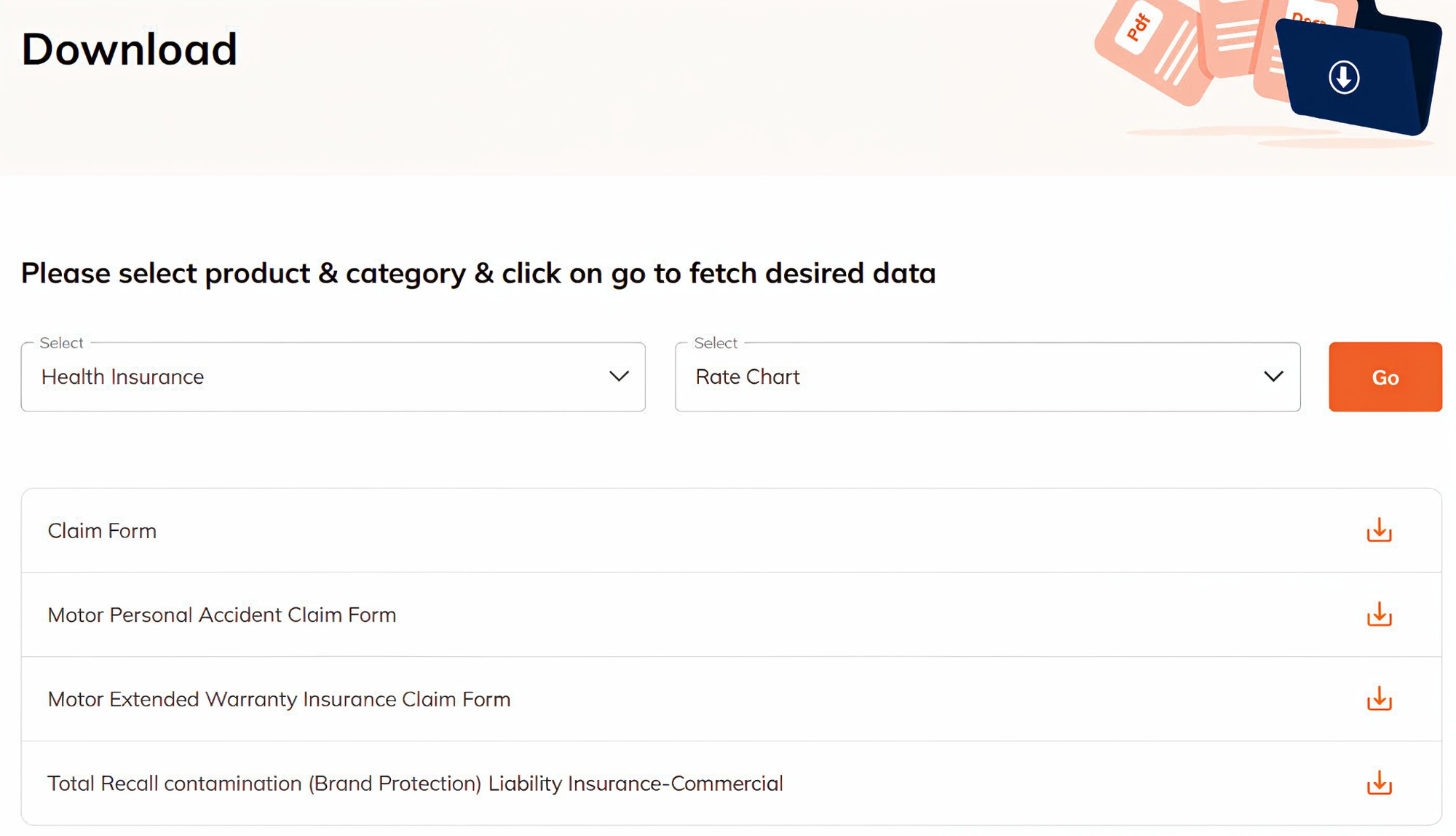

ICICI Lombard Health Insurance Premium Chart PDF Download

Step 1: Visit the Official Website. Go to the ICICI Lombard official website.

Step 2: Navigate to "Info Center" (you will find this at the top as well as the bottom of the page).

Step 3: Click on the "Info Center" to find the “Downloads” section.

Step 4: In the “Downloads” page, you can choose the product and category, then click on Go to fetch the required data.

Step 5: Select “Health Insurance” and “Rate Chart”. You’ll be redirected to a page listing all ICICI health insurance products, where you can download the relevant rate chart.

What Does the ICICI Lombard Health Insurance Premium Chart PDF include?

1. Age-wise Premium Tables: The document contains grids where:

- One axis shows age bands (for example: 18–25, 26–30, 31–35, etc.)

- The other axis shows the sum insured (for example: ₹3 lakh, ₹5 lakh, ₹10 lakh, ₹25 lakh, ₹50 lakh, etc.)Each cell shows the applicable annual premium (excluding GST and discounts).

2. Zone-based Pricing: ICICI Lombard uses zone-based pricing to account for differences in healthcare costs across cities. The PDF usually separates pricing by zones such as:

- Zone A: Major metros

- Zone B: Tier-2 cities

- Zone C: Rest of India

Premiums are generally lower in Zone C compared to Zone A, though the exact difference varies by product and sum insured (it’s not always a fixed 10–20%).

3. Policy Type and Family Structure The chart includes different rate grids for:

- Individual (1A) (A stands for adults and K stands for kids)

- Family floater options like 2A, 2A+1K, 2A+2K, etc.

Each family structure has its own premium table since pricing changes based on the number of members and the eldest adult’s age.

Premium Comparison: ICICI Lombard Elevate vs. Health AdvantEdge

To give you a clearer idea of how premiums vary across plans, here’s a quick comparison between two popular ICICI Lombard health insurance plans: Elevate and Health AdvantEdge.

Note: These are base premiums for a healthy individual living in Delhi (Zone A) with a ₹15L sum insured. Pre-existing conditions (PEDs) haven’t been factored into these prices.

The premiums mentioned are indicative and may change based on your age, city, health history, selected add-ons, and medical inflation.

Factors That Affect ICICI Lombard Health Insurance Premium

1. Age: Age is the most significant factor in the ICICI Lombard health insurance premium chart. As you grow older, the statistical risk of hospitalization increases, which leads to higher premiums. In family floater plans, the premium is calculated based on the age of the eldest insured member. You’ll notice that premiums remain fairly stable between ages 18–35, but tend to rise sharply every 5 years after age 40. Locking in a policy early helps you complete waiting periods while your premium is still at its lowest.

2. Sum Insured: The sum insured is the maximum amount the insurer will pay in a policy year. Note that increasing your coverage does raise your premium, but not in direct proportion. For example, doubling coverage from ₹5 lakh to ₹10 lakh doesn’t double the premium.

3. Family Composition: Premiums differ based on whether you choose an individual policy or a family floater. Family floaters (like 2A, 2A+1K, 2A+2K) are usually more affordable than buying separate individual policies. However, the total premium is still driven by the age of the eldest adult and the number of members covered.

4. Pre-existing Diseases: If you have conditions like hypertension, diabetes, or asthma, they can affect you in two ways. First, there is usually a waiting period of 2–3 years before these conditions are covered. Second, the insurer may apply a medical loading, which means an extra charge over and above the base premium mentioned in the ICICI Lombard health insurance premium chart.

5. City Tier / Zone-Based Pricing: ICICI Lombard uses zone-based pricing depending on the cost of healthcare in your city. Metro cities (Zone A) typically have the highest premiums due to higher treatment costs. Tier 2 and Tier 3 cities (Zone B/C) may attract lower premiums than metros, though the exact difference varies by plan and year. However, if you purchase a lower-zone policy and get treated in a higher-zone hospital, you may have to pay a co-payment from your own pocket. It’s also wise to inform your insurer if you relocate for work or family reasons, as they may reprice your premiums based on the new zone.

Why Choose Ditto for Your Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Here’s why customers like Abhinav love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 5,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation with us. Slots are filling up quickly, so be sure to book a call now or chat with us on WhatsApp!

Conclusion

The ICICI Lombard health insurance premium chart is one of the most practical tools to understand how your age, city, sum insured, and family structure directly affect what you pay every year. That said, premium numbers alone shouldn’t drive your decision. While ICICI Lombard offers competitive pricing and flexible coverage options, it’s equally important to compare features, hospital network, claim settlement experience, and long-term value across insurers.

Disclaimer

Frequently Asked Questions

Last updated on: