As a city, Delhi has been in the limelight for long - right from the Mughal era! The city’s fame can be attributed to a wide range of factors - its historical monuments, political significance, affordable & appealing markets, and more!

Unfortunately, one such contributing factor is its pollution level, which causes multiple ailments. While some residents have chosen to shift their residence to nearby locations (say, for example, Gurgaon), that isn’t an option for many. Additionally, the city has quite a high standard of living.

So you are looking at a Tier 1 city where an ailment/accident-related hospitalisation can cost you lakhs. Are you really ready to invest that amount? Or wouldn't it be so much better to opt for a health insurance policy that offers funding in times of medical emergencies? Such a smart financial step requires you to be more responsible and know about health insurance in Delhi, the best plans available, its importance in your city, and how to choose the best providers in detail before applying for a policy.

So, read on!

Pro tip: The health insurance market can be a labyrinth. Instead of spending hours navigating through the hundreds of policies out there, why not book a 30-minute call with our expert IRDAI-certified advisors? We don’t spam or pressure you to buy. Just honest insurance advice

Delhi and Health Insurance

Delhi stands out due to its unique juxtaposition of being a historical city with modern healthcare challenges. As the national capital with a significant influx of domestic and international visitors, the demand for high-quality medical services is constant. The city's healthcare infrastructure is stretched between highly advanced private facilities and under-resourced public hospitals.

Given this disparity, the role of health insurance becomes crucial in ensuring that Delhi's diverse population, from government officials to daily wage earners, has equitable access to healthcare. Additionally, the city's ongoing struggle with air quality issues significantly heightens the health risks associated with respiratory diseases, making health insurance not just a luxury but a necessity for its citizens.

Why do you need health insurance policies in Delhi?

Delhi's residents face a dual challenge: managing the high cost of healthcare and mitigating the risks associated with urban living. The city's medical inflation often outpaces the general inflation rate, leading to a rapid increase in healthcare costs. Furthermore, the lifestyle in Delhi, characterised by high stress, varying air quality, and an increasingly sedentary lifestyle, contributes to the prevalence of lifestyle-related health issues such as cardiovascular diseases, diabetes, and chronic respiratory illnesses. Health insurance mitigates the financial impact of these conditions by covering a wide range of medical expenses, from diagnostic tests and medical treatments to hospitalisation and post-treatment care, ensuring that residents do not have to compromise on quality care due to cost considerations.

Things to remember when choosing health insurance plans in Delhi

When navigating the complex landscape of health insurance in Delhi, several additional factors need consideration:

- Tailored Benefits: Look for plans that offer benefits tailored to urban health needs, such as coverage for pollution-related health issues.

- Flexibility and Portability: Ensure that the insurance plan offers flexibility in terms of adding or removing members and moving between different insurance providers without losing the benefits.

- Limits and Caps: Carefully check for any sub-limits or caps on room rent, specific treatments, and disease-specific caps, which can significantly affect out-of-pocket expenses during a medical emergency.

- Preventive Healthcare: Given the high prevalence of lifestyle diseases, opt for plans that offer preventive healthcare options, including regular health check-ups, vaccination coverages, and wellness benefits.

How to choose the best health insurance plans in Delhi?

Selecting the best health insurance requires a strategic approach:

- Choose the perfect health insurance provider.

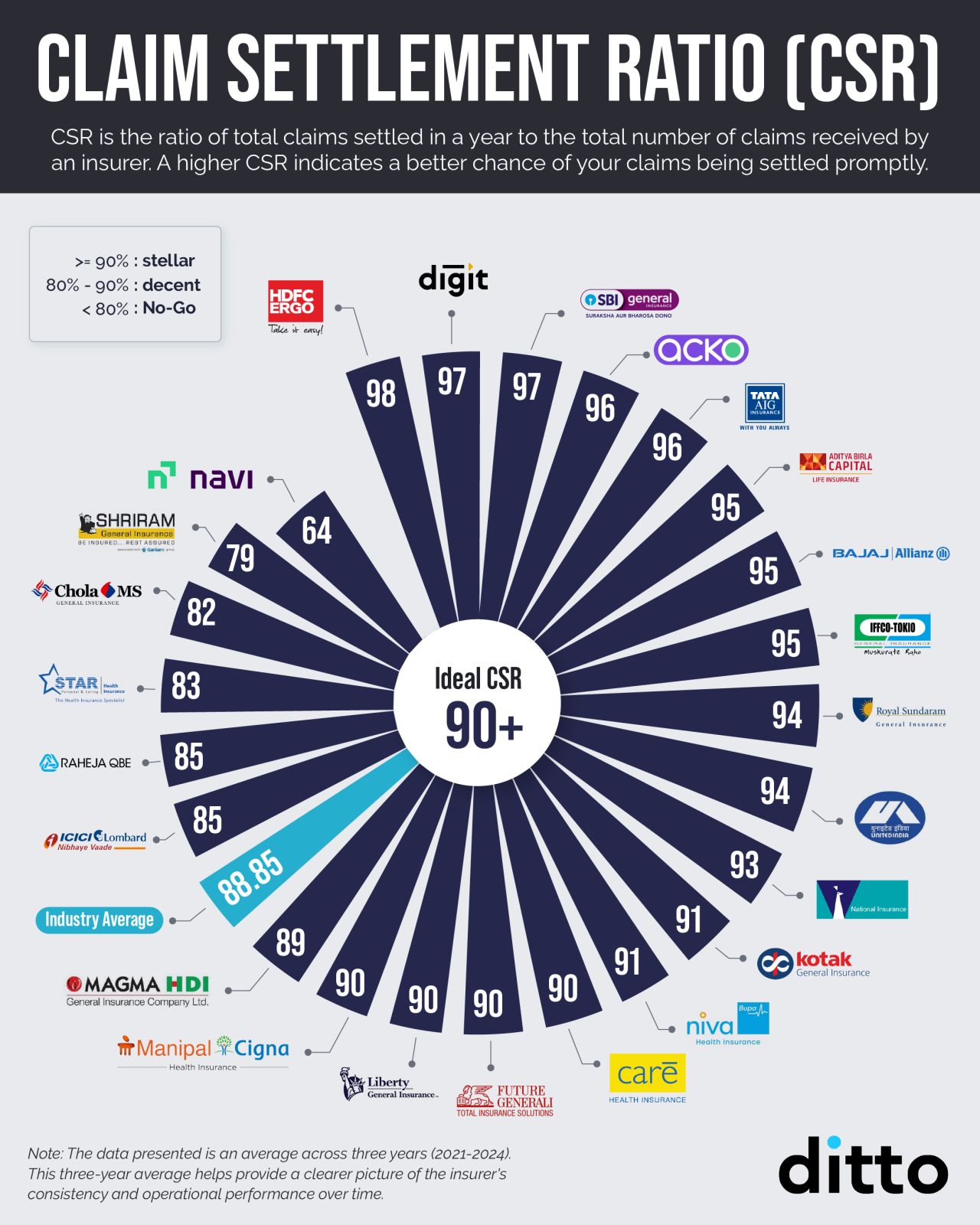

- Claim Settlement Ratio: Calculated as the number of health insurance claims settled in a year against the number of claims raised to the insurer in the year, the Claim Settlement Ratio, or CSR, is one of the crucial metrics used to determine an insurer's credibility. It sheds some light on the insurer's claim settlement track record.

Here is a quick look at the CSR of some of the top health insurance providers (average of data from 2021 to 2024) -

However, it would be good to remember that CSR numbers can easily be misleading since they do not reflect whether the claim has been settled entirely or partially. A CSR of 90 or above is the best way forward for a credible health insurer. On the other hand, if an insurer’s CSR is less than 80, you might start looking around for other providers.

- Incurred Claim Ratio: An insurer's Incurred Claim Ratio (ICR) indicates the provider's future sustainability and, hence, its claim settlement potential. The ICR metric is measured by dividing the total amount spent settling claims against the total amount collected as premiums across the year.

Here is a quick look at the ICR of some of the top health insurance providers (average of data from 2021 to 2024) -

The ideal ICR of a health insurer lies between 50 and 70. An ICR of less than 50 suggests that the insurer is too focused on building its business profits, and an ICR of more than 80 means that the insurer is too focused on settling claims (which might seem great in the short term, but in the long run, the insurer might face a financial crunch).

- Complaint Volume: When choosing a health insurance provider, it's important to consider the number of complaints the insurer receives (per 10,000 claims filed). This metric offers valuable insight into the claim settlement experience of current policyholders. As most complaints arise from delayed or denied claims, the complaint volume strongly indicates the insurer's approach to handling claims and their ability to settle them efficiently.

Here is a quick look at the complaint volume of some of the top health insurance providers (average of data from 2021 to 2024) -

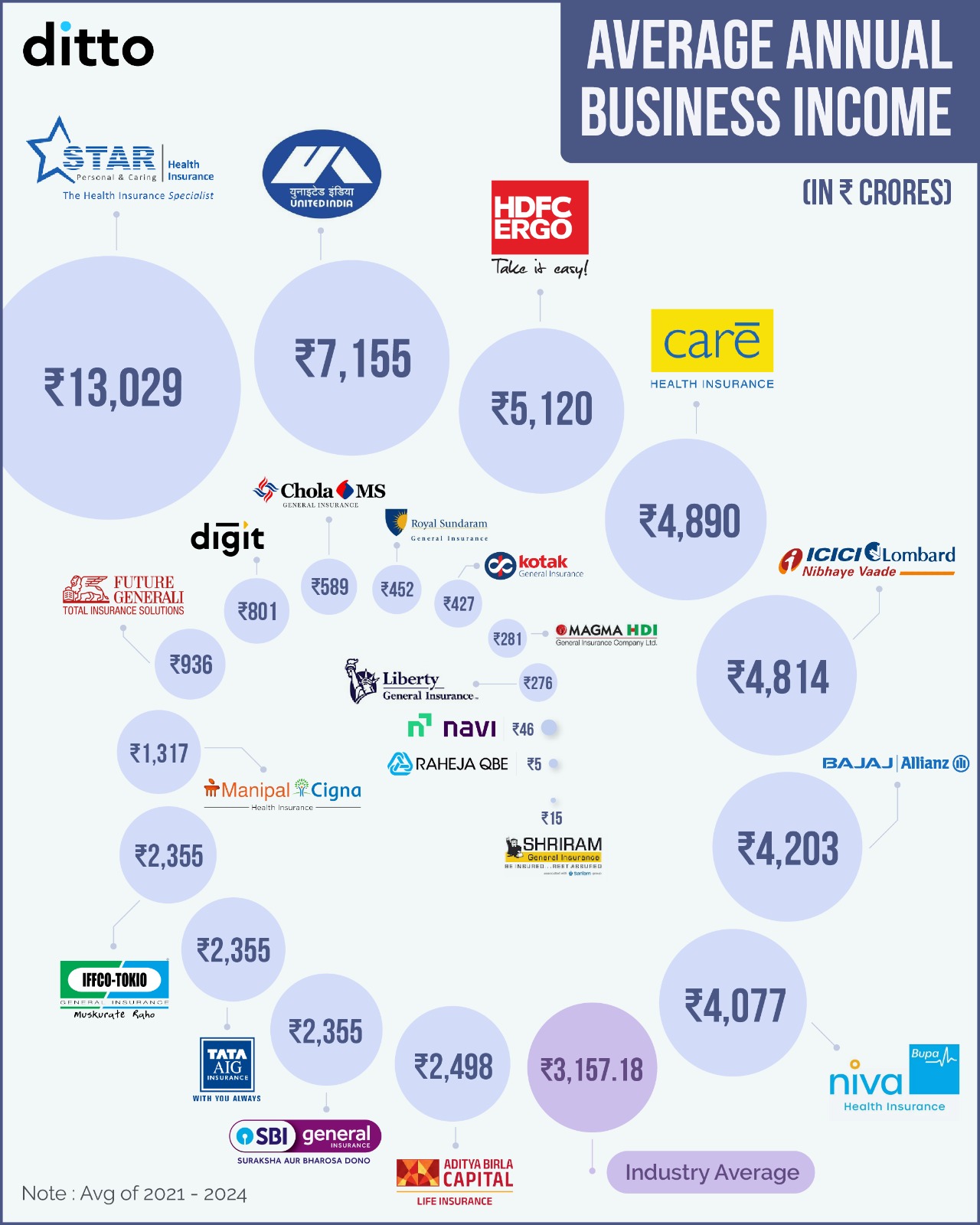

- Annual Average Business Income: While this may not be an exact measure of an insurer’s credibility, understanding their annual business volume helps you gauge the scale of the insurer’s operations and the potential size of its client base. Since you are entrusting a significant coverage amount to the insurer, choosing a medium- or large-sized provider with a strong client base is advisable, as this often reflects their reliability and established track record in the insurance industry.

Here is a quick look at the average annual business income of some of the top health insurance providers (average of data from 2021 to 2024) -

- Understand the Fine Print: Read the policy documents carefully to understand the fine print, including the coverage details, exclusions, and the claims process.

- Annual Limits and Renewability: Verify if the plan has annual limits on claims and whether it offers lifetime renewability, which can be crucial for long-term health management.

- Customer Support: Choose insurance companies known for their strong customer support, as navigating claims and understanding policy benefits can be challenging without effective communication.

- Technology Integration: Consider insurers that provide digital tools for easier management of policies, including mobile apps for tracking claims, health records, and accessing telemedicine services.

What are the Best Health Insurance Plans in Delhi for 2025?

In 2025, the best health insurance plans for residents of Delhi will be those that offer comprehensive coverage tailored to the specific health risks of living in a major metropolitan area. Some notable plans are:

| Best Health Insurance Plans in Delhi | Key Features | Drawbacks |

|---|---|---|

| HDFC ERGO Optima Secure | - No room rent restrictions - No mandatory copayment - No disease-wise sub-limit - 50% Renewal Bonus (up to 100%) - Secure Benefit doubling coverage from day one - Extensive hospital network - Restoration benefit |

- Higher premiums compared to other plans - No add-ons to reduce 3-year waiting period for pre-existing diseases |

| Aditya Birla Activ One Max | - No room rent restrictions - No mandatory copayment - No disease-wise sub-limit - Super Credit benefit (up to 500% loyalty bonus) - HealthReturns program rewarding healthy lifestyle - Unlimited restoration |

- Slightly higher complaint volume and lower track record as compared to peers. |

| Care Supreme | - No room rent restrictions - No mandatory copayment - No disease-wise sub-limit - 50% Renewal Bonus (up to 100%) - Unlimited restoration - Cumulative Bonus Super add-on (additional bonus of 100% p.a up to 500%) |

- Higher complaint volume - No free health check-ups can be availed with an add-on |

| Niva Bupa ReAssure 2.0 (Titanium +) | - No room rent restrictions - No mandatory copayment - No disease-wise sub-limit - Booster+ carry-forward bonus (up to 11X coverage) - Lock the Clock feature - Unlimited restoration |

- Insurer's claim settlement ratio and complaint volume could be better |

| ICICI Lombard Elevate | - Single Private Room (Add-on available to remove restrictions) - No mandatory copayment - No disease-wise sub-limit - 20% No Claim Bonus (up to 100%) - Add-ons for unlimited coverage, maternity, inflation-adjusted cover |

- Insurer’s claim settlement ratio and network of hospitals need improvement |

Each plan is structured to address the multifaceted aspects of healthcare needs in a bustling metropolis like Delhi, ensuring that policyholders can navigate the healthcare landscape effectively without financial hardships.

Last updated on: