Choosing between Care Supreme vs Niva Bupa ReAssure 3.0 is a common dilemma since both are highly comprehensive, feature-packed health insurance plans. If you prioritize unrestricted access to modern treatments and a marginally better claims settlement history, choose Care Supreme. However, if you prefer an unlimited base sum insured, flexible pre-existing disease waiting period coverage, and a Lock the Clock premium feature, Niva Bupa ReAssure 3.0 is the superior choice.

In terms of pricing, a 25-year-old in Delhi pays approximately ₹9,761 per year for Niva Bupa ReAssure 3.0 Black and around ₹13,821 per year for Care Supreme, both for a ₹10 lakh sum insured.

This guide is for anyone shortlisting between these two for a first-time purchase or planning a switch.

Care Supreme and Niva Bupa ReAssure 3.0 are both popular, well-priced, and genuinely comprehensive. While they may seem similar, subtle differences in claim handling, pricing, and plan features can make one a better fit for your specific needs.

In this Niva Bupa ReAssure 3.0 vs Care Supreme Health Insurance review, we will help you choose the right plan with clarity and confidence.

Confused between Care and Niva Bupa Health Insurance for your family? Book a call or WhatsApp us!

They are known for innovative, feature-packed plans at affordable premiums.

ReAssure 3.0 is the upgraded version of their flagship ReAssure 2.0 plan and is available in four variants: Classic, Select, Elite, and Black.

The most distinctive feature of this plan is the Lock the Clock benefit, which allows you to lock in your premiums based on your entry age until a claim is made. Keep in mind that premiums would still increase due to medical inflation or overall repricing.

Care Health Insurance

Care Health Insurance (formerly Religare Health Insurance) has been around since 2012 and is currently the second-largest standalone health insurer in India by premium.

Care Supreme is one of their flagship retail plans.

The standout feature of Care Health insurance plans is that they do not impose loading charges if the plan is being issued. This makes the plans affordable and especially beneficial for those with pre-existing conditions such as asthma, high blood pressure, or diabetes.

Key Feature Comparison: Care Supreme vs Niva Bupa ReAssure 3.0

Features

Care Supreme

Niva Bupa ReAssure 3.0

Sum Insured (SI) Options

₹5 lakh to ₹1 crore

₹5 lakh, ₹10 lakh, unlimited

Entry Age

Adult: 18 years to no limit, child: 91 days to 24 years

Adult: 18 years to 99 years, child: 91 days to 30 years

Exit Age

Adult: no limit, child: 25 years

No limit

Policy Period

1 / 2 / 3 years

1 / 2 / 3 / 4 / 5 years

Copayment

Not applicable

None for Black variant, applies if the room limit is breached in Classic/Select/Elite

Room Rent Limits

No limit

Classic: General room, Select: Twin sharing room, Elite: All except deluxe/suite, Black: No cap

Disease-Wise Sub-Limits

Not applicable

Not applicable

Modern Treatment Limits

No sub-limit

Classic and Select: ₹1 lakh per claim; Elite and Black: No limit

Restoration

100%, unlimited times, any illness

100%, unlimited times, any illness (not applicable for unlimited SI)

Bonus

Inbuilt bonus of 50% per year up to 100% irrespective of claims, Cumulative Bonus Super add-on: up to 500% extra bonus, Cumulative Bonus Booster: extra 100% bonus each year with no limit

Booster+ Benefit: Carry forward of unutilized base sum insured, up to 10x (not applicable for unlimited SI)

Coverage, Exclusions & Waiting Periods Compared: Care Supreme vs Niva Bupa ReAssure 3.0

Let’s have a look at what’s covered and what’s not covered in both plans.

Parameters

Care Supreme

Niva Bupa ReAssure 3.0

Pre-and Post-Hospitalization Expenses

60-180 days

60-180 days

Consumables

Add-on (Claim Shield Plus)

Add-on (Claim Safeguard+)

Annual Health Checkup

Add-on, available from the 31st day of the policy on a cashless basis for a defined list of tests (separate list for those below 18 years of age)

Add-on, available from day 1 on a cashless basis as per defined packages

Daycare, AYUSH, and Domiciliary Treatments

Covered up to SI

Covered up to SI

Outpatient Department (OPD) Coverage

Add-on, available from the 31st day, 4 consultations with a general physician, 4 with specialists on a reimbursement basis, capped at ₹500 per visit

Add-on (Wellconsult+): Choose up to 5x the total premium for consultations, diagnostics, pharmacy, and gym memberships. 20% copayment applicable for reimbursement

Ambulance

Road: Covered up to SI, ₹15 lakh and above,SI below ₹15 lakh, covered up to ₹10,000 per yearAir: Add-on, ₹5 lakh per policy year

Classic/Select: Road ₹2,000, Air: Not applicable Elite/Black: Road up to SI, Air: Up to ₹5 lakh per hospitalization

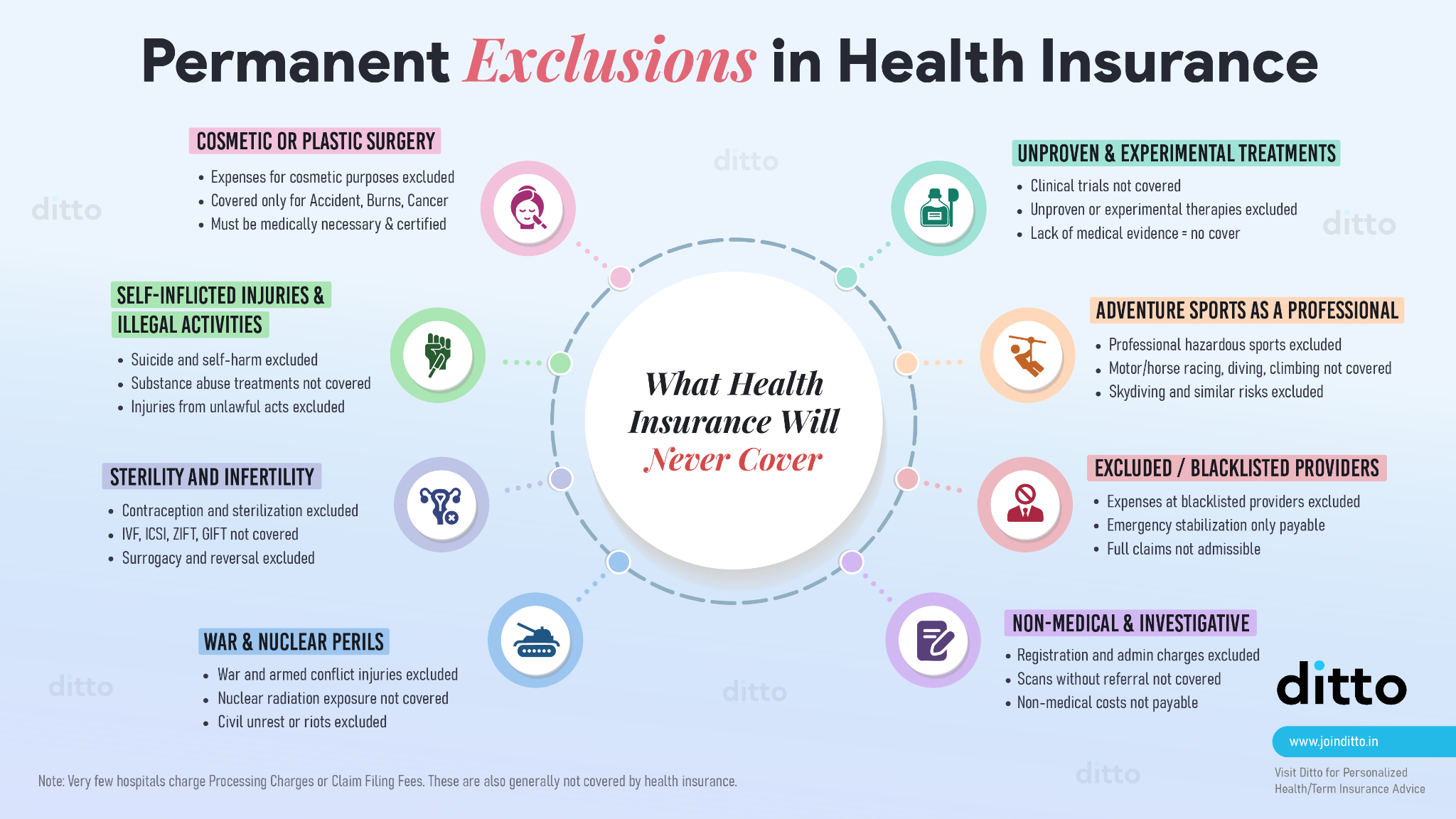

Exclusions

For a full list of permanent exclusions that apply to both plans, refer to the infographic below.

Waiting Periods

Both Niva Bupa ReAssure 3.0 and Care Supreme have identical waiting periods:

Initial Waiting Period (30 days): A mandatory waiting period before any claims can be made, except for accidents, which are covered from day 1.

Specific Illness Waiting Period (2 years): Certain slow-growing conditions, such as cataracts, hernia, or joint replacements, are covered only after 2 consecutive years of coverage.

Pre-Existing Disease (PED) Waiting Period (3 years): Any condition you had before buying the policy, like diabetes or hypertension, will only be covered after 3 years.

Key Insight

Niva Bupa ReAssure 3.0 has an in-built benefit which provides immediate coverage for up to 145 pre-existing conditions from day one, or the standard 36-month waiting period can be chosen. An additional premium (risk loading) may apply based on health details, with two options: coverage with a waiting period or Day 1 coverage for selected conditions.

Care Health offers an add-on called Instant Cover/Instant Cover Plus to reduce the waiting period for a few listed conditions. Along with this, Care also offers a PED reduction add-on to help reduce the waiting period for any condition from 3 years to either 2 or 1 year.

Which Is the Better Insurer: Care Health or Niva Bupa?

To determine which insurer is better, let’s look at the performance metrics for both.

CSR: Care Health’s CSR exceeds the industry average and is slightly higher than Niva Bupa, indicating long-term reliability.

ICR: Both insurers are in the healthy range (50%-80%). The moderate ICR suggests that both insurers are paying claims steadily while also retaining sufficient premiums to ensure long-term stability.

Complaint Volume: The complaint volume for both insurers is significantly high. Since standalone health insurers handle only health policies, their complaint volume is concentrated within a single complex category.

Annual Business: In the case of Niva Bupa vs Care Health, both are large players, but the latter holds a comparatively higher market share, reflecting greater customer trust and reach.

Network Hospitals: Care has a wider hospital network, which may make cashless access easier in more locations.

CTA

Premium Comparison

Profile

Care Supreme

Niva Bupa ReAssure 3.0 (Black)

Individual, Age 25

₹13,821

₹9,761

Family Floater 2A (35, 35)

₹18,332

₹17,040

Family Floater 2A+1C (35, 32, 5)

₹23,046

₹22,286

Senior Citizen 2A (60, 60)

₹58,095

₹50,469

Note: A stands for adult, and C denotes child. These are indicative premiums for a Delhi resident (pincode: 110001) for a ₹10 lakh SI. Your premium will vary based on age, city, medical history, add-ons, and applicable discounts.

We’ve added essential add-ons to make both plans on par with each other:

Niva Bupa: Claim Safeguard+ add-on

Care Health: Annual health check-up, Cumulative Bonus Super, Air Ambulance, Wellness Benefit, Claim Shield Plus

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

Ditto’s Verdict on Care Supreme vs Niva Bupa ReAssure 3.0

Choose Care Supreme Health Insurance if You:

Want unrestricted coverage for modern treatments without sub-limits.

Prefer a simpler plan where key benefits don't depend on picking the right variant.

Prioritize insurer reliability. Care Health's improving CSR and larger network give it a consistent edge.

Are covering older family members or parents with PEDs and don’t want loadings.

Choose Niva Bupa ReAssure 3.0 if You:

Are young (under 30) and want to lock in your premium for years.

Need day-1 PED coverage for the listed 145+ pre-existing conditions, and are okay with loadings.

Want the option of an unlimited sum insured.

Are comfortable with the fact that this is a newly launched plan, so real-world claims performance is yet to be seen fully.

Bottom Line: Ditto's pick for most buyers is Care Supreme. It's a tried-and-tested product with clean features, no hidden sub-limits, and an insurer with a stronger upward claim track record. If you're young and Lock the Clock is a real priority, ReAssure 3.0 Black is a compelling alternative. If you are looking for more options to compare, refer to our comprehensive guide to the best health insurance plans in India.

Frequently Asked Questions

Which is better, Care Supreme or Niva Bupa ReAssure 3.0?

Both are solid health plans, but the right choice depends on your priorities. If you want cleaner features, no sub-limits on modern treatments, and a stronger claim track record, Care Supreme is the better fit. If you are young and want to lock in your premium or need day-1 PED coverage for one of 145 listed conditions, Niva Bupa ReAssure 3.0 wins. At Ditto, we lean toward Care Supreme as the default pick for most buyers because it is simpler and more reliable.

Does Niva Bupa ReAssure 3.0 cover pre-existing diseases from day one?

Yes, but with conditions. Niva Bupa ReAssure 3.0 offers an in-built benefit that provides immediate coverage for up to 145 listed pre-existing conditions from day one of the policy. However, this comes with a risk loading, meaning your premium may be higher based on your specific health details. Alternatively, you can opt for the standard 36-month PED waiting period and avoid the loading. At Ditto, we recommend weighing the extra premium cost against the benefit of early coverage before deciding which route makes sense for you.

Does Care Supreme have sub-limits on modern treatments?

No, Care Supreme does not have any sub-limits on modern treatments. This means procedures like robotic surgeries, stem cell therapy, and other advanced medical interventions are covered up to the full sum insured. Niva Bupa ReAssure 3.0, by contrast, limits coverage for modern treatments to ₹1 lakh per claim in the Classic and Select variants. Only the Elite and Black variants of Niva Bupa ReAssure 3.0 offer unlimited coverage for modern treatments. At Ditto, we see the absence of sub-limits in Care Supreme as a meaningful advantage for long-term policyholders.

Which health plan is better for a 25-year-old, Care Supreme or Niva Bupa ReAssure 3.0?

For a 25-year-old, Niva Bupa ReAssure 3.0 can be a compelling choice because of the Lock the Clock feature. Buying at 25 locks in a lower base premium, and with no claims, that rate stays fixed longer. The annual premium is also lower at around ₹9,761 for a ₹10 lakh cover compared to ₹13,821 for Care Supreme. That said, if you prefer a simpler plan with no variant complexity and a stronger claim history, Care Supreme still holds up well. At Ditto, we recommend Care Supreme for its tried-and-tested performance.

Is Care Health Insurance good for diabetes patients?

Care Health Insurance is a good option for individuals with chronic conditions because it does not impose loading charges for pre-existing conditions such as diabetes or hypertension, when the plan is issued. The insurer also offers a specific Instant Cover/ Instant Cover plus add-on that can reduce the standard waiting period for these conditions to just 30 days, which is shorter than the typical 3-year wait in standard policies. With a solid incurred claim ratio of 58.68%, Care Health demonstrates financial stability in handling such high-risk profiles. This makes it a top-tier choice for families managing long-term health issues.

Is Care Supreme or Niva Bupa ReAssure 3.0 better for covering senior citizen parents?

For senior citizen parents, Care Supreme is generally the safer pick. Care Health's network of 11,400+ hospitals makes cashless access easier across more locations. Importantly, Care Supreme does not impose any copayments, even for PED claims, whereas some Niva Bupa variants impose copayments if room limits are breached. For two adults aged 60, Care Supreme costs around ₹58,095 per year, compared with ₹50,469 for Niva Bupa ReAssure 3.0 Black. At Ditto, we lean toward Care Supreme for parents with pre-existing conditions because it avoids risk loading and delivers a cleaner, more predictable claims experience.

Can I claim a Section 80D tax deduction on premiums paid for Care Supreme or Niva Bupa ReAssure 3.0?

Under the old tax regime, health insurance premiums may qualify under Section 80D. The limit is usually ₹25,000 for self/spouse/children below 60 and ₹50,000 where the insured person is a senior citizen. Parents have a separate limit. So, if you are below 60 and your parents are senior citizens, the combined limit can be ₹75,000. If both you and your parents are senior citizens, it can go up to ₹1 lakh, subject to tax rules. At Ditto, we tell buyers the tax benefits should never be the deciding factor when choosing between two products.

Is the Be-Fit Rider in Care Supreme actually worth buying?

The Be Fit rider in Care Supreme gives policyholders unlimited access to partner fitness centers and wellness facilities for the duration of the policy. It is designed to encourage preventive health habits rather than fund treatment costs. The practical value depends entirely on whether the partner gyms and wellness centers are conveniently located near you. At Ditto, we recommend checking the partner list in your city and full add-on details before paying for this add-on.

Last updated on:

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.