Overview

My Health Care Plan EDG+ positions itself as a premium health insurance solution. It offers several uncommon features such as Age Shield and Smart Tenure. But do these benefits translate into meaningful real-world value?

This review covers the Bajaj MHCP EDGE+ features, benefits, riders, waiting periods, exclusions, and key considerations to help you evaluate the plan with confidence.

Key Features of Bajaj General MHCP EDGE+ (My Health Care Plan EDGE+)

Riders Offered:

- Double Sum Insured Benefit: Doubles your base inpatient sum insured, giving you an additional buffer that can be used across multiple admissible claims within the same policy year.

- Cost of Prescribed External Medical Aid: Covers medically prescribed external aids and support devices after an admissible hospitalization, including braces, supports, and similar equipment, up to 10% of the sum insured (maximum ₹5 lakh).

- Consumable Cover: Covers specified consumables and non-medical expenses for policies with sum insured options of ₹5 lakh, ₹7.5 lakh, and ₹10 lakh, reducing out-of-pocket hospitalization costs.

- Consumables Plus: Covers a wider range of non-medical consumables and hospitalization-related expenses that are usually excluded from standard health insurance plans. The rider is available for policies with a sum insured of above ₹10 lakh.

- Major Illnesses & Accident Multiplier: Automatically doubles the sum insured for specified critical illnesses, such as cancer, kidney failure, major organ transplant, as well as accident-related hospitalizations.

- Super Cumulative Bonus: Enhances the no-claim bonus structure with higher cover growth and bonus protection, subject to policy conditions and annual claim thresholds. Choose a bonus growth rate of 50% or 100% per claim-free year, with the maximum bonus accumulating up to 200%, 500%, or 600%, depending on the selected option and policy terms.

- Fetal Flourish: Pays a lump-sum benefit for specified invasive investigations and treatments arising from complications affecting the unborn baby. A 9-month waiting period applies, and eligibility is limited to individuals aged 18 to 45 years.

- Walk to Win: Rewards healthy habits with renewal discounts based on app-tracked daily step counts. If you walk 7,500 steps daily, you earn a 5% discount, while for 10,000 steps, you receive a 10% discount.

- StepUp Benefit: Allows a one-time increase in the base sum insured at the next available sum insured slab at first renewal, subject to no claims during the policy tenure. However, waiting periods apply to the increased cover.

- Health Limitless: Offers one eligible hospitalization, daycare, or AYUSH claim during the policy term without being subject to the annual sum insured limit. This rider is available for a sum insured of ₹10 lakh and above.

- Insta Shield: Reduces waiting periods for specified chronic conditions such as diabetes, hypertension, asthma, and hypothyroidism. You are covered starting on the 31st day after policy issuance.

- No Claim Discount: Offers a renewal premium discount of 1.5% for claim-free years. However, if you select this rider, the accrued cumulative bonus or super cumulative bonus will not apply.

Did You Know?

Sample Premiums

Note: Premiums shown are indicative estimates derived from the policy rate chart using Zone A (Delhi) and inbuilt covers only. Actual premiums for Bajaj Health Insurance plans may vary due to add-ons, underwriting, location, deductibles, and applicable discounts.

Age Shield and Smart Tenure: What These Unique Features Mean

Age Shield Rider

- Locks Your Entry-Age Premium: Renewal premiums are calculated using your entry age rather than your current age until the first paid claim.

- Useful for Young Buyers: Someone buying the policy at age 25 can continue paying premiums based on the 25-year age band until a claim is settled.

- Not a Lifetime Guarantee: Once a paid claim occurs, premiums move to the applicable current-age band from the next renewal. While the Age Shield Rider can help lock premium calculations to your entry age, insurer-wide repricing can still affect premiums across the portfolio, as seen in the past with certain health insurance products such as Niva Bupa ReAssure 2.0.

- Works Better in Individual Policies: A claim affects only the insured member who made the claim. In a family floater plan, a claim by any insured member terminates the Age Shield benefit for the entire policy.

Smart Tenure Rider

- Creates a Single Coverage Pool: Combines the annual sum insured over the entire policy tenure into a single cumulative fund.

- Helpful for Large Early Claims: A 5-year policy with ₹15 lakh annual cover creates a ₹75 lakh pool that can be accessed from year one.

- Uses Future Coverage Today: Claims reduce the pooled balance, which then carries forward for the remainder of the policy term.

- India-Only Benefit: Applicable only for hospitalization claims incurred within India.

- Major Trade-Off: Choosing Smart Tenure makes you ineligible for add-ons such as Global Cover, International Cover, and Double Sum Insured Benefit. The rider applies to individual sum-insured policies (not to families).

- No Installment Premium Option: Premiums must be paid upfront under the applicable multi-year policy structure.

Coverage, Sum Insured Options, and Global Cover

Take Note: Global Cover does not come with a separate sum insured. Any overseas hospitalization claim reduces your base hospitalization cover. In addition, benefits such as pre- and post-hospitalization expenses, organ donor cover, and road ambulance expenses are not covered under Global Cover.

Beyond policy features, it is equally important to evaluate the insurer behind the product. On this front, Bajaj General has delivered strong operating metrics in recent years, making it a noteworthy player in the health insurance space.

Bajaj General reported strong operating metrics between FY 2022 and FY 2025. It recorded a 96.78% claim settlement ratio, well above the industry average of 91.22%, while reporting just 3.07 complaints per 10,000 claims. The insurer also operates through a network of 12,000+ hospitals, providing broad cashless hospitalization access across India.

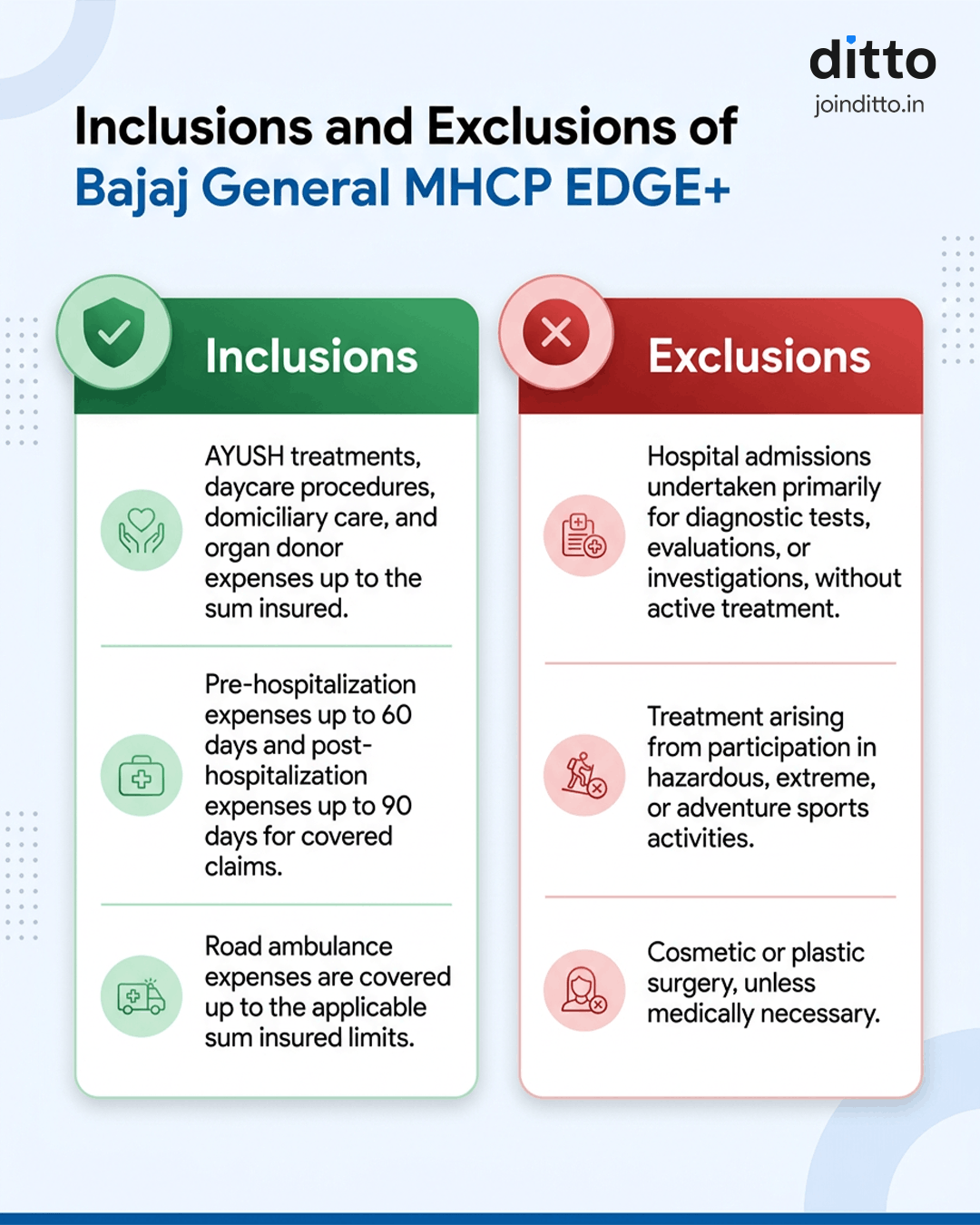

Exclusions and Waiting Periods in Bajaj MHCP EDGE+

Bajaj General MHCP EDGE+ includes standard waiting periods as included in other health insurance plans:

- Pre-Existing Disease Waiting Period: Declared pre-existing diseases and their direct complications are covered after 36 months of continuous coverage, unless reduced via add-ons. If you increase your sum insured, the applicable waiting periods restart only on the enhanced portion, while the existing cover continues as per the completed waiting periods.

- Specific Disease Waiting Period: Certain listed conditions and procedures, such as cataract, hernia, piles, gallstones, hysterectomy, and joint replacement, carry a 24-month waiting period, except when arising from accidents. This waiting period can be reduced to 12 months if the respective variation is selected.

- Initial Waiting Period: Illness-related claims are not covered during the first 30 days of the policy. Accident-related hospitalizations are covered from day one.

Check out the infographic for a clear understanding of what the plan includes and excludes.

Note: For the complete list of inclusions and exclusions, refer to the official policy wording before making a purchase decision.

Should You Buy Bajaj General MHCP EDGE+?

MHCP EDGE+ may suit young families, high-income individuals, and buyers looking for extensive customization.

- Features such as Age Shield, high sum-insured options, Global Cover, and specialized riders make it appealing to those seeking protection against rising healthcare costs and major medical emergencies.

- It can be particularly relevant for buyers who value flexibility and want to tailor coverage to their specific needs.

However, the plan may feel complex for those who prefer a straightforward policy. Multiple rider combinations and compatibility restrictions mean buyers should carefully evaluate both the benefits and trade-offs before purchasing.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right health insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 24,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call now or chat with our advisors on WhatsApp.

Conclusion

Bajaj MHCP EDGE+ stands out for its high coverage limits, innovative features, and extensive customization options. For buyers willing to carefully understand and configure the plan, it can offer meaningful protection. However, the value ultimately depends on selecting the right combination of riders rather than relying on the base policy alone.

From an insurer's perspective, Bajaj General has strengthened its health insurance portfolio considerably in recent years by introducing features such as Age Shield, unlimited restoration, and multi-year coverage options that were previously more common among competitors. Combined with the insurer's strong operating metrics and broad customization options, it emerges as a comprehensive health insurance option worth considering.

In case you wish to explore some simpler plans, refer to our guide on the best health insurance plans in India.

Frequently Asked Questions

Last updated on: