Quick Overview

Medical emergencies can arrive without warning, and even a short hospital stay can drain your savings. A ₹3 lakh health insurance plan offers basic coverage, but is insufficient given the rising medical inflation in India.

This guide helps you understand whether a ₹3 lakh health insurance plan is sufficient for your needs and how it compares to higher coverage options in today’s increasing medical costs.

Is a ₹3 Lakh Health Insurance Enough for You in 2026?

A ₹3 lakh cover can be sufficient for young, healthy individuals residing in smaller cities. However, the health cover might fall short when we consider the following:

- Medical Costs: Healthcare expenses in India have increased sharply in recent years. A short hospital stay for surgery or illness can easily cost ₹4–5 lakh in a private setup, and more for complex treatments. This means a ₹3 lakh cover may get fully used in just one claim and will not be enough even for a single hospitalization.

- Location: In smaller towns, ₹3 lakh may still comfortably cover basic treatments. However, in metro cities like Mumbai, higher consultation fees, room rents, and procedure costs can quickly exhaust the same cover.

- Hospital Choice: Premium private hospitals with advanced technology and experienced specialists charge significantly more. Even routine procedures can become expensive due to diagnostics and robotic surgeries, which can drain a ₹3 lakh limit faster than expected.

- Family Floaters: When ₹3 lakh is shared among multiple members, even a single hospitalization can reduce or exhaust the family's cover. This makes it risky, especially if more than one claim arises in a year.

- Health Factors: If you have conditions such as diabetes, hypertension, or heart disease, the likelihood of hospitalization increases. These conditions may also require repeated treatments, making a higher sum insured more practical and safer.

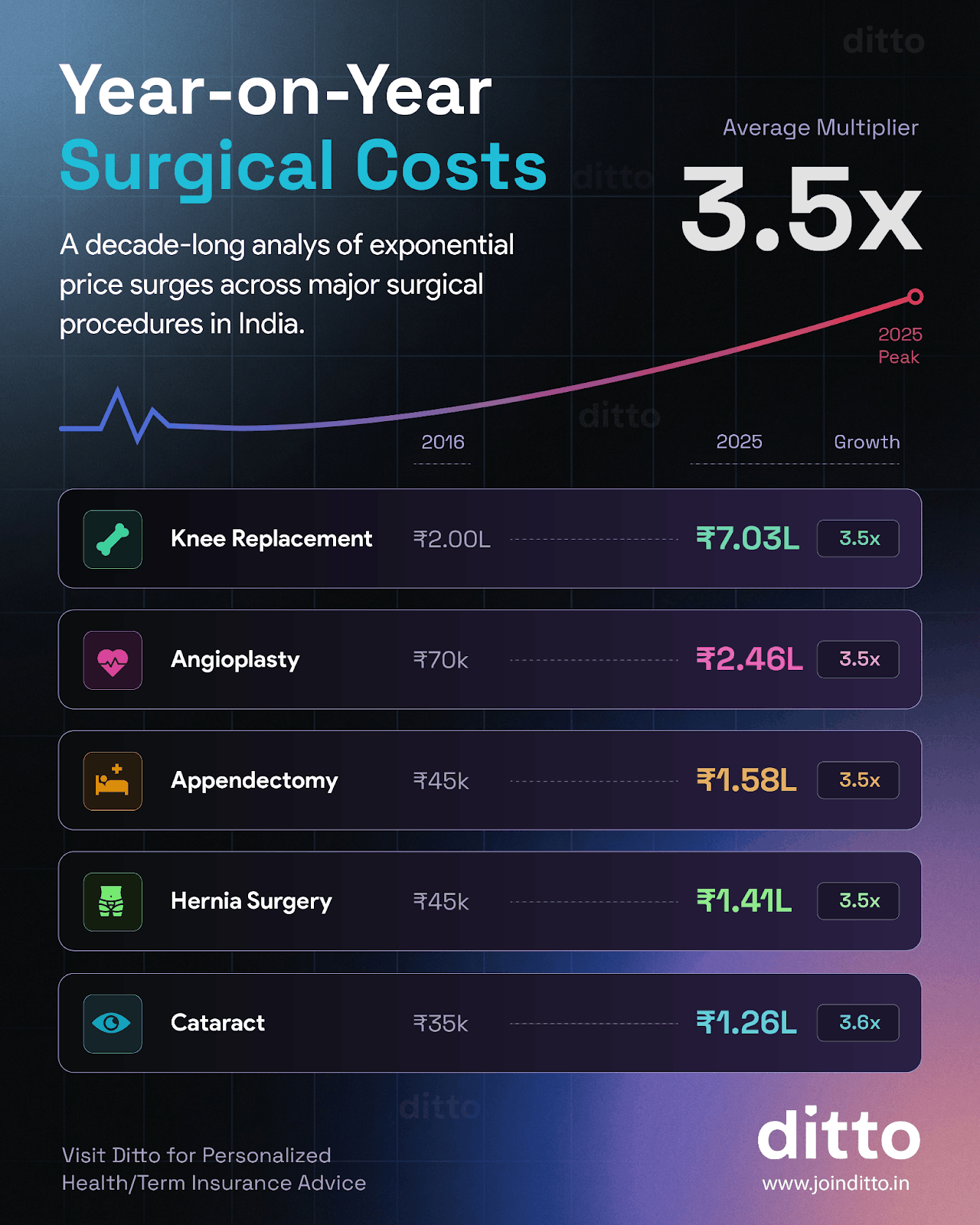

Take a look at the infographic to understand how medical costs have increased from 2016 to 2025.

Note: A ₹3 lakh base can be paired with a super top-up, but gaps remain. Super top-ups apply the deductible to total annual medical expenses, not each claim, so smaller or spread-out bills can still lead to out-of-pocket costs.

Best Health Insurance Plans With ₹3 Lakh Sum Insured

When evaluating the best health insurance plans, it’s important to look beyond a ₹3 lakh cover, as it often falls short in today’s high-cost medical environment. In fact, most insurers today don’t actively offer such low coverage, as they fall short of modern healthcare needs. Instead, opting for a ₹15–25 lakh cover ensures more comprehensive protection.

A ₹3 lakh sum insured today works more as a basic safety net than a comprehensive cover. ₹3 lakh plans may suit tight budgets or act as a supplement to employer cover, but for long-term security, ₹15 lakh is closer to what can be considered truly comprehensive today.

Popular Plans With Sum Insured Offered

Note: The minimum sum insured offered by the insurer also depends on your location.

Premiums For ₹3 Lakh Sum Insured

The premium for ₹3 lakh health cover is lower, making it seem cost-effective. Many assume this justifies the limited coverage. However, the premium gap relative to a ₹15–25 lakh plan is not proportionate to the protection gained. Paying slightly more offers far stronger, comprehensive coverage that better matches today’s medical costs and reduces out-of-pocket risk.

For instance, here’s a comparison of sample premiums across three coverage options for people living in New Delhi. The illustration uses the Aditya Birla Activ One Max plan to show how the premium increases relative to the jump in coverage.

Note: In the table, ‘A’ stands for adult, and ‘C’ denotes a child. The premiums are indicative, and the final amount may vary based on your age, location, and insurer’s underwriting.

Common Mistakes to Avoid While Choosing a ₹3 Lakh Sum Insured

Thinking ₹3 Lakh is Enough

Medical costs have risen sharply. Even a short hospital stay or a common knee replacement can cost ₹7–9 lakh. This means your entire cover can get exhausted in just one claim.

Using it for Family Coverage

When multiple members share ₹3 lakh, one hospitalization can consume most of the cover. This leaves little to no protection for the rest of the family that year.

Not Planning for Repeat Hospital Visits

Health issues often require follow-ups or multiple admissions. A single claim can exhaust the cover, making it difficult to manage additional medical expenses later.

Choosing Only Based on Low Premiums

A lower premium may feel like a smart saving, but it often comes with limited coverage. When a real medical emergency happens, the gap between costs and coverage becomes very clear.

Ignoring Where You Live

In cities like Bengaluru or Delhi, hospital charges, room rents, and doctor fees are much higher. ₹3 lakh may not last beyond basic treatment.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or chat over WhatsApp with our advisors.

Conclusion

A ₹3 lakh sum insured may work as a starting point or a temporary buffer, but it falls short as a dependable standalone cover in today’s high-cost healthcare environment. Even a single major hospitalization can quickly exhaust it. For real financial protection and peace of mind, moving to a higher sum insured is a far more practical and future-ready decision.

Frequently Asked Questions

Last updated on: