Quick Overview

A ₹25 lakh health insurance plan is a strong base cover for many buyers today. It can comfortably handle major surgeries, long intensive care unit (ICU) stays, or one serious illness in a private hospital. But that may not be the right fit for everyone. Your ideal cover depends on where you live, your age, and whether you are buying for yourself or your family.

In this article, we break down whether ₹25 lakh health insurance is enough, the best plans at this sum insured, and the premiums you can expect.

Is a ₹25 Lakh Health Insurance Enough for You in 2026?

For most working adults and families in India, ₹25 lakh is a genuinely strong base cover. It's the maximum cover we recommend to take for the following reasons:

Medical Inflation

Medical inflation in India leads to rising treatment costs every 2-3 years. A ₹10 lakh cover that feels adequate today may feel like ₹5 lakh in a few years. Choosing ₹25 lakh health insurance reduces the risk of your cover feeling inadequate a few years later.

Difficulty in Increasing Sum Insured

If you are diagnosed with a serious medical condition later, an insurer may reject your request to increase the sum insured. Waiting too long to upgrade your coverage can leave you underinsured at exactly the stage of life when your health risks and treatment costs are both higher.

Black Swan Analogy

While there’s little chance of ₹25 lakh health insurance getting exhausted, an unexpected health emergency could turn your life upside down. Examples of high-cost treatments include cancer care or a bone marrow transplant, which can create a major financial burden.

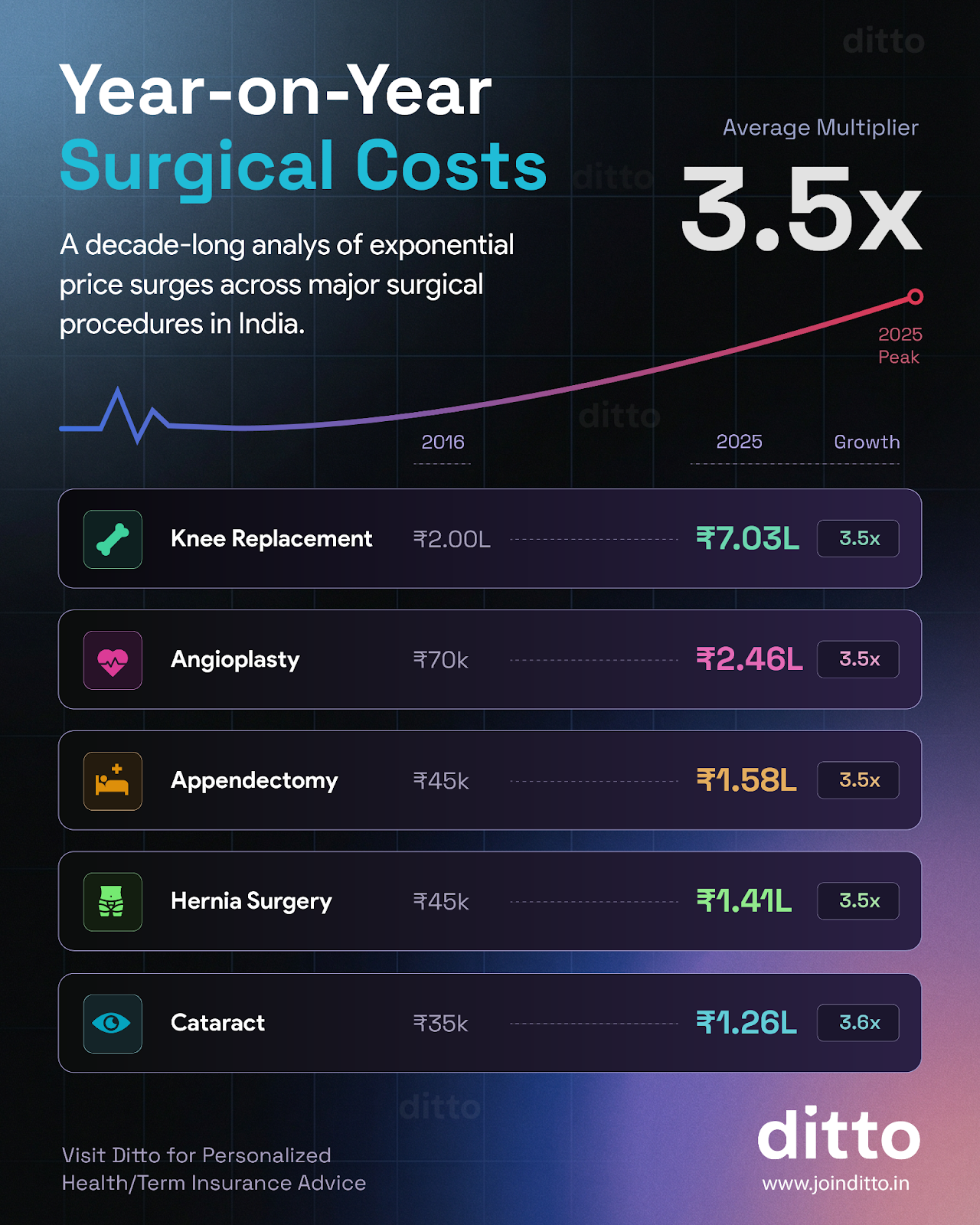

Let’s also take a look at the surgical costs in India that have increased to a great extent between 2016 and 2025:

A ₹25 lakh health insurance plan also gives you a comfortable buffer over these real-world costs.

Best Health Insurance Plans With ₹25 Lakh Sum Insured

Here, CSR stands for claim settlement ratio, ICR denotes incurred claims ratio, and SI implies the sum insured.

For more details, refer to our guide on the best health insurance plans in India 2026.

Premiums For ₹25 Lakh Sum Insured

A ₹25 lakh health insurance plan may sound expensive at first. However, there is very little difference in the premiums you pay for a cover amount of ₹10 lakh, ₹15 lakh, and ₹25 lakh.

To illustrate this, let’s compare the sample premiums of all three options for a tier 1 city (New Delhi: 110001). The plan considered for this calculation is Aditya Birla Activ One MAX.

Here, ‘A’ refers to an adult, and ‘C’ denotes a child.

Note: The premiums are indicative, and the final amount may vary based on your medical profile, age, or location.

Common Mistakes to Avoid While Choosing a ₹25 Lakh Sum Insured

Treating ₹25 Lakh as Sufficient Forever

Rising medical costs each year mean your ₹25 lakh cover, which feels generous today, may not feel sufficient in 10–15 years. Look for plans with strong bonuses and restoration benefits that build effective coverage over time.

Ignoring the Sub-Limits

Some plans that appear affordable at ₹25 lakh may come with co-pays, room rent restrictions, or disease-wise sub-limits. Limitations related to room rent caps trigger a proportionate deduction from your entire claim, meaning you end up paying an amount out of pocket. Always check the fine print on sub-limits before buying health insurance plans.

Not Checking Primary Features

A comprehensive health insurance plan will always have primary features like coverage for pre- and post-hospitalization expenses, to name a few. If your ₹25 lakh health insurance plan does not include these standard features, you can consider switching to another insurer that provides the same features.

Adding Parents to a ₹25 Lakh Floater

When you add a 58-year-old parent to your floater, the premium is calculated based on their age. That significantly increases what you pay. Worse, a hospitalization for the parent can drain the shared sum insured quickly, leaving younger members under-covered for the rest of the year. Separate policies for parents always make more financial sense.

Ignoring Claim Experience

A lower premium does not always mean better value. Claims-related issues make up a large share of customer grievances, so you should also look at the insurer’s service track record, network strength, and claim support experience.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or chat on WhatsApp with us now!

Ditto’s Take on ₹25 Lakh Health Insurance

₹25 lakh health insurance is typically the maximum base cover we recommend for most buyers in 2026. It works particularly well for single individuals in Tier 1 cities and for those in Tier 2 cities who already have corporate coverage and want to supplement it with a personal policy.

That said, it may not always be sufficient for family floaters. Since the sum insured is shared among all members, a single large claim can significantly reduce the available coverage for others within the same policy year. In such cases, opting for a higher base cover can offer more reliable protection.

Frequently Asked Questions

Last updated on: