Quick Overview

If you’re purchasing health insurance for the first time, you’ll likely come across cover options such as ₹10 lakh, ₹15 lakh, and ₹25 lakh. A ₹15 lakh sum insured may appear adequate, but is it actually enough if a major medical emergency occurs?

In this article, we’ll explain what a ₹15 lakh cover means and what it typically covers.

Is ₹15 Lakh Health Insurance Enough in 2026?

For most people we speak to, a ₹15 lakh base cover is a good starting point. But whether the amount is enough for you depends on various factors.

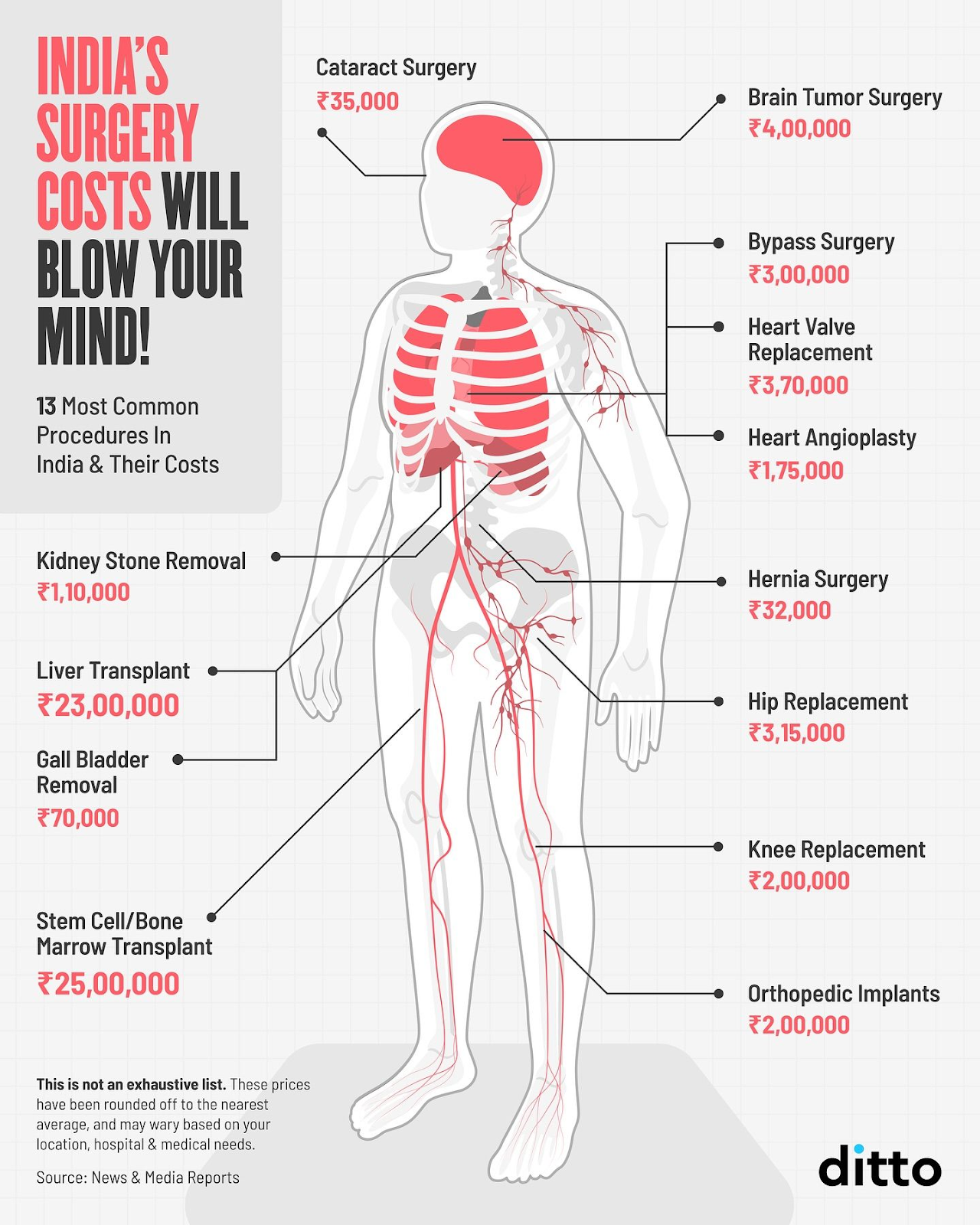

The infographic above gives a quick snapshot of typical surgery costs, so you can assess whether a ₹15 lakh cover matches real-world hospital bills.

- Hospital Bills

In many private hospitals, a serious surgery can easily run into several lakhs. A ₹15 lakh base cover gives you enough room to handle a major hospitalization in a year without stressing about the bill.

- Good Bonuses

The real strength of a ₹15 lakh base cover shows up when you pair it with a strong bonus. For example, Aditya Birla’s Activ One MAX increases your cover by 100% each year as a bonus (irrespective of claims), up to 500%. This means your cover can grow up to about ₹90L with bonuses, but you keep paying premium for only a ₹15L base cover.

- Individual Vs. Family Floater

In an individual policy, the full ₹15 lakh is reserved just for you, which is a solid cover. In a family floater, ₹15 lakh works well when you choose a plan with strong restoration benefits. For example, with unlimited restoration like in Care Supreme, for each new hospitalization in the year, you have access to ₹15 lakh, instead of everyone sharing one common pool.

Best Health Insurance Plans With ₹15 Lakh Sum Insured

In our main guide on the best health insurance plans in India, we picked a handful of policies based on our Policy Rating Framework. All these plans, including HDFC ERGO Optima Secure, Care Supreme, Aditya Birla Activ One Max and Niva Bupa ReAssure 2.0 Platinum +, provide policyholders with a ₹15 lakh cover.

Premiums for ₹15 Lakh Sum Insured

Note: Premiums are for Delhi - 110010, including necessary and mandatory add-ons.

Common Mistakes People Make While Choosing a ₹15 Lakh Cover

Tiny Base, Huge Top-Up

Many people take a small base (like ₹3–5 lakh) and a big super top-up instead of a ₹15 lakh base. Super top-ups are more restrictive, they only pay after you cross a fixed deductible, and the restrictions can impact how much your bill gets paid. For most buyers, a simple ₹15 lakh base cover is easier to understand and more reliable.

Picking A Plan With Restrictions

Room rent caps, disease-wise limits, and co-pays can quietly cut down how much of your ₹15 lakh actually gets used. If your room is above the allowed category or a surgery has a cap or co-pay, a bigger chunk of the bill comes from your pocket. It’s better to choose a comprehensive plan.

Bonus And Restoration

Good comprehensive plans add bonus cover every year and refill (restore) your sum insured when it’s used up, which really helps if your family has more than one hospitalization in a year. Skipping these features can leave your ₹15 lakh exhausted after a single large claim.

Choosing Only By Price

It’s tempting to pick the cheapest ₹15 lakh plan, but lower premiums often mean more restrictions or weaker network hospitals. The smarter move is to balance price with clean terms, so your ₹15 lakh acts like a strong, usable cover.

Why Choose Ditto For Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Here’s why customers like Abhinav love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation with us. Slots are filling up quickly, so be sure to book a call now!

Ditto’s Take on ₹15 Lakh Health Insurance

If you’re buying health insurance for the first time, a ₹15 lakh as a good starting cover, not the final destination. For most people, the ideal range is around ₹15–25 lakh. Starting at ₹15 lakh keeps the premium manageable and can handle big hospital bills and even multiple claims in a year. Over time, you can increase your base cover to ₹20–25 lakh as your income grows.

A ₹15 lakh cover usually works well for:

- Young individuals buying their first health plan

- Couples or small families starting with a floater

- Anyone who wants to start now and gradually move towards ₹20–25 lakh later

That said, if you live in a metro, have parents in the same policy, or a strong family history of serious illnesses, we’d still nudge you towards the higher end of that ₹15–25 lakh range sooner rather than later.

Frequently Asked Questions

Last updated on: