Overview

Most people don’t calculate their health insurance cover. They guess it. ₹5 lakh feels too little. ₹10 lakh feels safe. ₹1 crore feels like the ultimate protection.

But hospital bills do not work according to your sum insured. A cardiac procedure, a cancer diagnosis, or a prolonged ICU stay in the same year can burn through a ₹10 lakh cover faster than you think.

Considering this, ₹10 lakh is the bare minimum worth having. And ₹1 crore is about peace of mind for people who want to walk into a hospital without stressing about running out of cover. But not everyone needs to go that far either.

In this guide, we compare ₹10 lakh vs ₹1 crore health insurance so you can figure out what actually fits your age, city, and family.

Is ₹10 Lakh Health Insurance Still Enough in 2026?

If you are admitted for a serious condition at a well-known private hospital in Bengaluru, Delhi, or Mumbai, your ₹10 lakh plan can quickly get exhausted before you get discharged. Once your sum insured is exhausted, every remaining rupee comes directly from your pocket.

Even with restoration benefit, the restored amount applies to the next claim in the same year and is subject to its own conditions. Try to pick a cover that prevents the “I had insurance, but still had to arrange a few lakhs” moment.

Swapnil, one of our senior advisors, shared a simple rule of thumb.

Start with ₹5 lakh. Then add ₹5 lakh for every “YES” below:

- Do you live in a metro city?

- Do you prefer chain hospitals over local ones?

- Are you above 45?

- Do you have any pre-existing conditions?

Hence, we recommend a cover amount of at least ₹15 lakh to ₹25 lakh to strike a balance between coverage and affordability.

Did You Know?

That said, a ₹10 lakh cover is not always the wrong choice. Here is when it still makes sense:

- Plan for Parents: Premiums jump significantly at older ages when you increase the sum insured. A ₹10 lakh plan you can afford to renew every year without gaps is more valuable than a ₹1 crore plan you discontinue after two years.

- Budget is a Constraint: Some coverage is always better than having no coverage at all. A ₹10 lakh plan with comprehensive coverage (no room rent cap, no disease-wise sub-limits, unlimited restoration, and a good insurer) can go a long way.

- Residing in Smaller Towns: Costs at local hospitals in tier-2 and tier-3 cities are meaningfully lower. ₹10 lakh may be sufficient depending on where you live and the hospitals you would use.

Key Insight

When Does It Make Sense to Go for ₹1 Crore Cover?

If you are young and healthy, it is a good time to lock in a ₹1 crore plan. Premiums start lower when you buy at a younger age. You can avoid loading charges and complete waiting periods while you’re healthy.

Beyond young buyers, here is who genuinely benefits from ₹1 crore health insurance.

Metro Residents

Hospitals in metro cities such as Bengaluru, Delhi, and Mumbai charge significantly more for the same treatment than those in smaller cities. A ₹10 lakh plan may not be sufficient if something serious happens at a renowned private hospital.

Anyone Above 40

The risk of a critical illness like cardiac issues, cancer, kidney failure, and other high-cost conditions rises considerably after 40. The combination of higher risk and higher costs is exactly what a ₹1 crore cover helps with.

People with Family Medical History

If a parent or sibling has a medical history of conditions like diabetes or high blood pressure, your own risk is elevated. It is better to have the cover in place before treatment costs start eating into your savings.

Families on Floater Plans

A floater plan means the coverage is shared between all family members. If two people need hospital care in the same year, the cover runs out twice as fast. A ₹1 crore floater gives the family a larger shared safety net.

Two Ways to Build ₹1 Crore Cover

- Standalone ₹1 Crore Base Plan

You get comprehensive features under a single policy from the one insurer. This includes coverage for consumables, access to modern treatments, no room-rent cap (in most good plans), and a straightforward experience when you need to make a claim. - ₹10 Lakh Base Plan + ₹90 Lakh Super Top-up

Here you have two separate policies. The base plan is used first. Once your ₹10 lakh base plan or your chosen deductible is exhausted, the super top-up kicks in for the rest. The combined premium is lower, but the features of super top-ups can be restrictive. Moreover, the claims process is more complicated because two policies and possibly two insurers can be involved, which means twice the paperwork.

Premium Comparison: ₹10 Lakh vs ₹1 Crore Health Insurance

The premium for ₹10 lakh health insurance plan is just one piece of the picture. Here is how it stacks up against a ₹1 crore policy and a base plan combined with a super top-up so that you can see exactly what each option costs.

Note: A stands for adult and C stands for child. The premiums are calculated for the Care Supreme base plan and the Care Supreme Enhance super top-up for healthy individuals residing in Delhi (pincode 110010). The figures are indicative and may vary based on age, location, medical history, and selected add-ons.

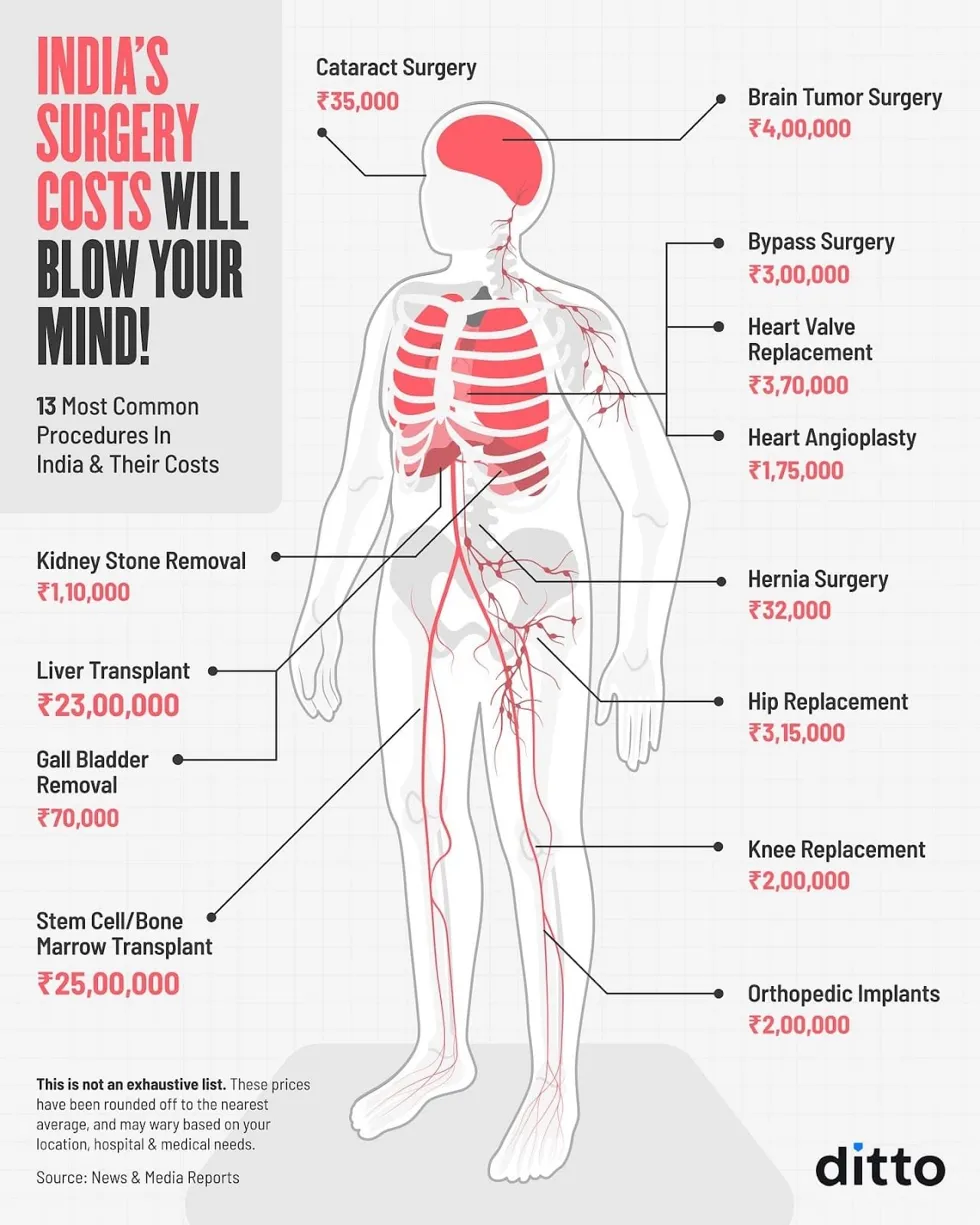

How to Decide the Right Sum Insured for Your Needs?

To give you a sense of what different surgeries actually cost, have a look at the infographic below:

Looking at these costs, there is no single ‘right’ health insurance cover for everyone. The right sum insured depends on where you live, who the policy covers, your current health, and how much premium you can comfortably renew every year.

- If your budget allows, a ₹1 crore base plan is a safer long-term option. This is especially useful if you live in a metro, are buying a family floater, and want protection against rising medical costs.

- If a ₹1 crore plan seems expensive, don’t drop health insurance altogether. Start with a ₹15 lakh-₹25 lakh cover instead. A smaller policy that you can renew comfortably every year is better than a high-cover policy that becomes unaffordable later.

Takeaway

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call now or chat with our advisors on WhatsApp.

Ditto’s Take

A ₹10 lakh sum insured may work as a starting point, but it falls short as a dependable standalone cover in today's healthcare environment, especially in metro cities. A single serious hospitalization can wipe it out entirely. For real financial protection, moving to a higher sum insured is the more practical and future-ready decision. The good news is that it costs less than most people expect. For a 25-year-old in Delhi, the jump from ₹10 lakh to ₹1 crore cover does not even double the premium, but it increases your protection 10 times over.

More than the cover amount, what matters is selecting the right policy. Make sure it has no room-rent cap, comes with restoration benefits, includes a comprehensive bonus, such as unlimited accumulation in Optima Secure+, and is from an insurer with a strong claim settlement record.

Your Next Step: Check your current policy. Review your sum insured, policy features, and renewal date to determine whether you want to increase your coverage. But, if you’re buying your first policy, you can check our comprehensive guide on the best health insurance plans in India as a starting point.

Frequently Asked Questions

Last updated on: