Quick Overview

People often misunderstand how an insurer metric like CSR works and assume a 99% figure implies a claim guarantee, but this is not the truth. This guide explains why relying only on claim settlement ratio alone can be misleading, what it actually means, and how to evaluate insurers using the right set of metrics.

What Is Claim Settlement Ratio and Why It Matters?

CSR in term insurance shows how often insurers settle claims. In contrast, CSR in health insurance usually means most claims are paid, but it doesn’t reflect delays or those that are partially paid.

While looking for an insurer, we recommend choosing one that meets the Ditto CSR benchmark, with life insurers at 97%+ and health insurers at 90%+, to ensure higher claim reliability.

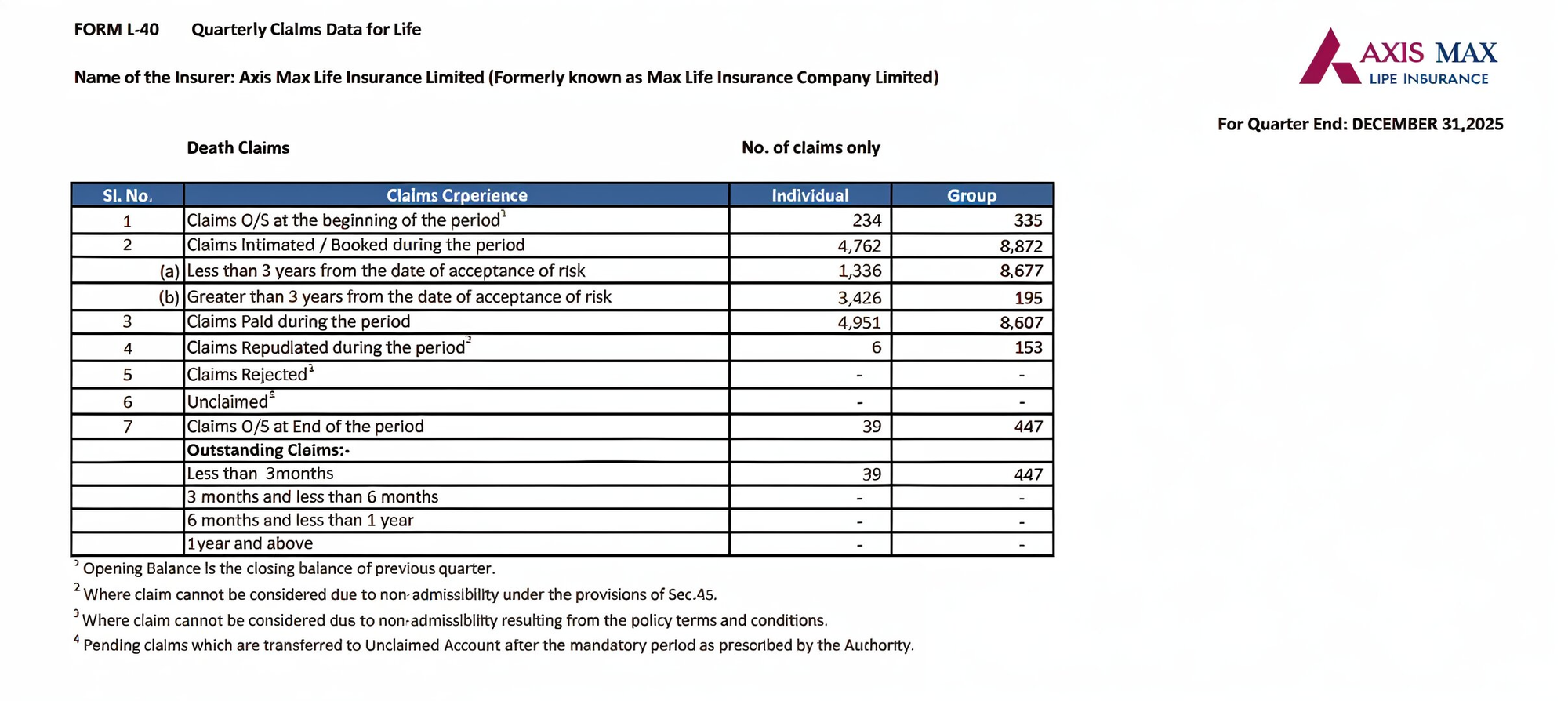

Life Claims Data as of December 2025

Source: Axis Max’s public disclosure

If you are looking for a term plan from insurers with established track records and affordable riders, we recommend the best term insurance plans, which align with your future goals and family needs.

Why Claim Settlement Ratio Alone Can Be Misleading?

- A high CSR does not guarantee that every claim will be approved, as rejections can still occur due to exclusions, documentation gaps, or policy conditions.

- CSR does not indicate the actual amount paid, so partial settlements or deductions are not reflected in the ratio.

- CSR is influenced by the mix of policies and claim types an insurer handles, which can vary widely across companies.

To make more informed insurance decisions, let’s understand the common myths and realities that shape how claims are actually processed in both health and term insurance.

Health Insurance

Term (Life) Insurance

Take Note: CSR is an aggregate across all claim types and products offered by an insurer. A company that primarily sells low-sum, small endowment policies will process a different claims profile than one that primarily offers large individual term plans.

Important Factors Beyond Claim Settlement Ratio

How to Evaluate an Insurance Company the Right Way?

- Read the Policy Wording and Exclusions Carefully: Review exclusions, waiting periods, sub-limits, and claim conditions.

- Check Claim Turnaround Time: Cashless health claims should be processed quickly, and final settlement should not take long. Look for insurers known for faster and more consistent claim processing timelines.

- Compare Coverage Quality, Not Just Statistics: Two policies with similar CSR can offer different coverage. Check room rent limits, co-pay clauses, disease sub-limits, and coverage for modern treatments. For term plans, review riders like accidental death, waiver of premium, and critical illness.

- Evaluate the Third Party Administrators (TPA) Model: Some insurers handle health insurance claims in-house, while others rely on TPAs. In-house claims teams often provide better coordination and faster resolution. Also, check customer support quality and complaint records.

Why Choose Ditto for Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat on WhatsApp with our expert IRDAI-certified advisors.

Conclusion

CSR shows the number of claims that were closed as settled, but it doesn’t reveal whether they were paid fully, quickly, or smoothly. To make an informed choice, consider additional factors:

- For health insurance, check complaints, network hospitals, ICR, and the insurer’s track record.

- For term insurance, consider complaints, ASR, annual claims paid, and solvency.

Disclaimer: The metrics and insights discussed in this article are based on publicly available data from IRDAI reports and insurer disclosures. Always review policy terms, exclusions, and consult a licensed advisor before purchasing insurance.

Frequently Asked Questions

Last updated on: