Quick Overview

Buying insurance can feel confusing, especially when you’re unsure how insurers decide your premium or approve your policy. This is where underwriting comes in. This guide walks you through what is underwriting in insurance, how it works and its effect on your insurance policy. This will help you understand how insurers assess risk and set the terms of your coverage.

Underwriting: How It Works in Health and Term Insurance

Underwriting in health insurance is the process by which insurers review your medical history to decide two things: whether you’re eligible for the policy and what premium you should pay. In simple terms, they assess the financial risk you bring based on existing conditions or potential health issues. This helps insurers price the policy fairly and set the right coverage terms.

In term insurance, underwriting works a bit differently. Here, insurers evaluate your overall mortality risk by looking at factors like age, health, and lifestyle. Using actuarial data, they estimate life expectancy and determine the premium accordingly.

In India, term underwriting also focuses on financial checks, including income, existing cover, and need for insurance, to ensure the sum assured is appropriate and to reduce risks like anti-selection.

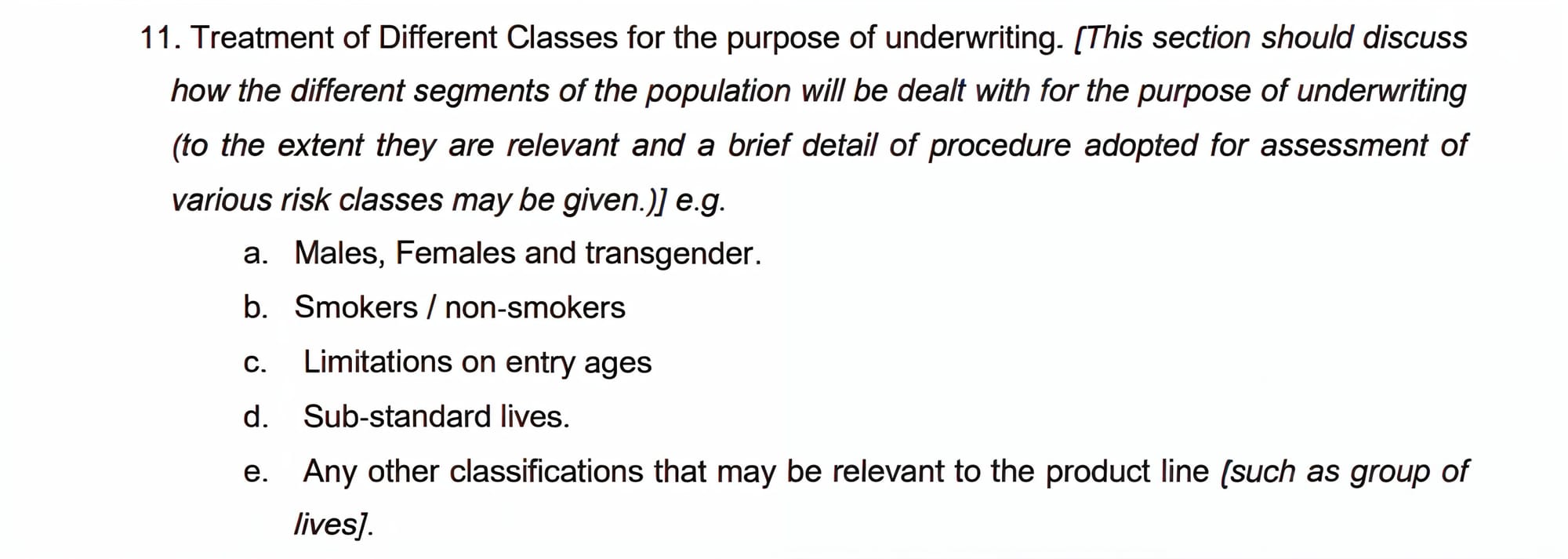

Here’s a snippet from an IRDAI circular explaining how life insurance applicants are classified into different underwriting risk categories.

Why Does Underwriting Exist?

How Does the Underwriting Process Work?

What Are the Risk Categories in Term Insurance Underwriting?

- Preferred Plus: Applicants in this category have excellent health and follow a healthy lifestyle. Hence, they get the lowest premiums.

- Preferred: This category is a bit similar to preferred plus, but with minor health variations like slightly high blood pressure. Premiums are slightly higher than preferred plus.

- Standard: This category includes most applicants and premiums are moderate. It includes average health profiles, higher BMI, or minor health issues.

- Substandard: This category includes higher-risk individuals with serious health conditions. Insurers assign ratings based on risk level, leading to higher premiums depending on severity.

Note: These are commonly used insurance terms. While specific insurers may use different wording, the meaning and intent are generally similar across policies.

Did You Know?

Why is Underwriting Important for Insurers?

How Does Underwriting Affect Your Insurance?

Underwriting directly influences whether you get covered, the terms of your policy, and how much you pay.

- Health Insurance: Based on your risk profile, the insurer may accept the policy as is, apply premium loading, impose waiting periods or exclusions, or reject the application altogether.

- Term Insurance: The insurer may accept, reject, postpone, or offer a counterproposal with revised premium, tenure, or sum assured based on your overall risk assessment.

At Ditto, we’ve seen insurers closely review bank statements during underwriting. Transactions tagged with terms like pharmacy or hospital can prompt follow-up questions to understand their nature and whether they relate to the applicant’s health.

Note: Policy renewals usually don’t trigger fresh underwriting. However, changes like adding members or increasing cover in health insurance, or adding riders or raising the sum assured in term life, may require a new underwriting review.

When Underwriting Makes the Difference: A Claim Story

Why Choose Ditto for Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

If your profile is considered high-risk, the insurer may offer counter offers such as lower coverage or a higher premium instead of outright rejection. Furthermore, Underwriting standards vary across insurers, so a rejection from one may still be accepted by another insurer with certain conditions. To avoid surprises, always disclose your medical and lifestyle details honestly, choose adequate coverage based on your needs, and compare insurers beyond just premiums.

Additionally, contestability periods protect policyholders over time, but they don’t eliminate early-stage risks.

- In term insurance, claims generally cannot be questioned after 3 years unless fraud is proven.

- In health insurance, after 5 continuous years, non-disclosure of pre-existing conditions cannot be used to reject claims.

Being informed helps you secure smoother approvals and a hassle-free claims experience later. In practice, a disclosed risk often leads to loading or waiting periods, while a hidden risk can collapse the whole contract.

Disclaimer: The information mentioned is for general understanding only and may vary by insurer and individual profile. Underwriting decisions, timelines, and terms are subject to change. Always review policy documents and consult a licensed advisor before making a decision.

Frequently Asked Questions

Last updated on: