Quick Overview

Your bank feels like the safest place for your money, but what happens if the bank itself runs into trouble? That’s where deposit insurance in India comes in. It protects your savings up to a fixed limit, which ensures you don’t lose everything if a bank fails.

The idea of deposit protection in India dates back to 1948, after a banking crisis in Bengal. It gained urgency in 1960 following the collapse of two major banks, Palai Central Bank Ltd. and Laxmi Bank Ltd., which further highlighted the need to safeguard depositor money.

This guide breaks down how DICGC deposit insurance works, what’s covered, and how it protects your money when a bank fails.

What Is Deposit Insurance and How Does It Work in India?

Deposit insurance in India safeguards your bank deposits in case a bank fails and is managed by the DICGC. As per the DICGC Annual Report, ₹476 crore worth of claims were settled in the year 2024–25.

Deposit Insurance works in a simple way:

- Your deposits are automatically insured when you keep money in an insured bank.

- Coverage is provided by the DICGC, and all accounts at the same bank are combined under a single limit.

- If a bank fails, depositors receive the insured amount.

For example, if you have ₹3 lakh in a savings account and ₹4 lakh in a fixed deposit in the same bank, your total deposit is ₹7 lakh. However, if the bank fails, you will receive only ₹5 lakh, as that is the maximum insured limit per bank.

How Much Premium is Paid?

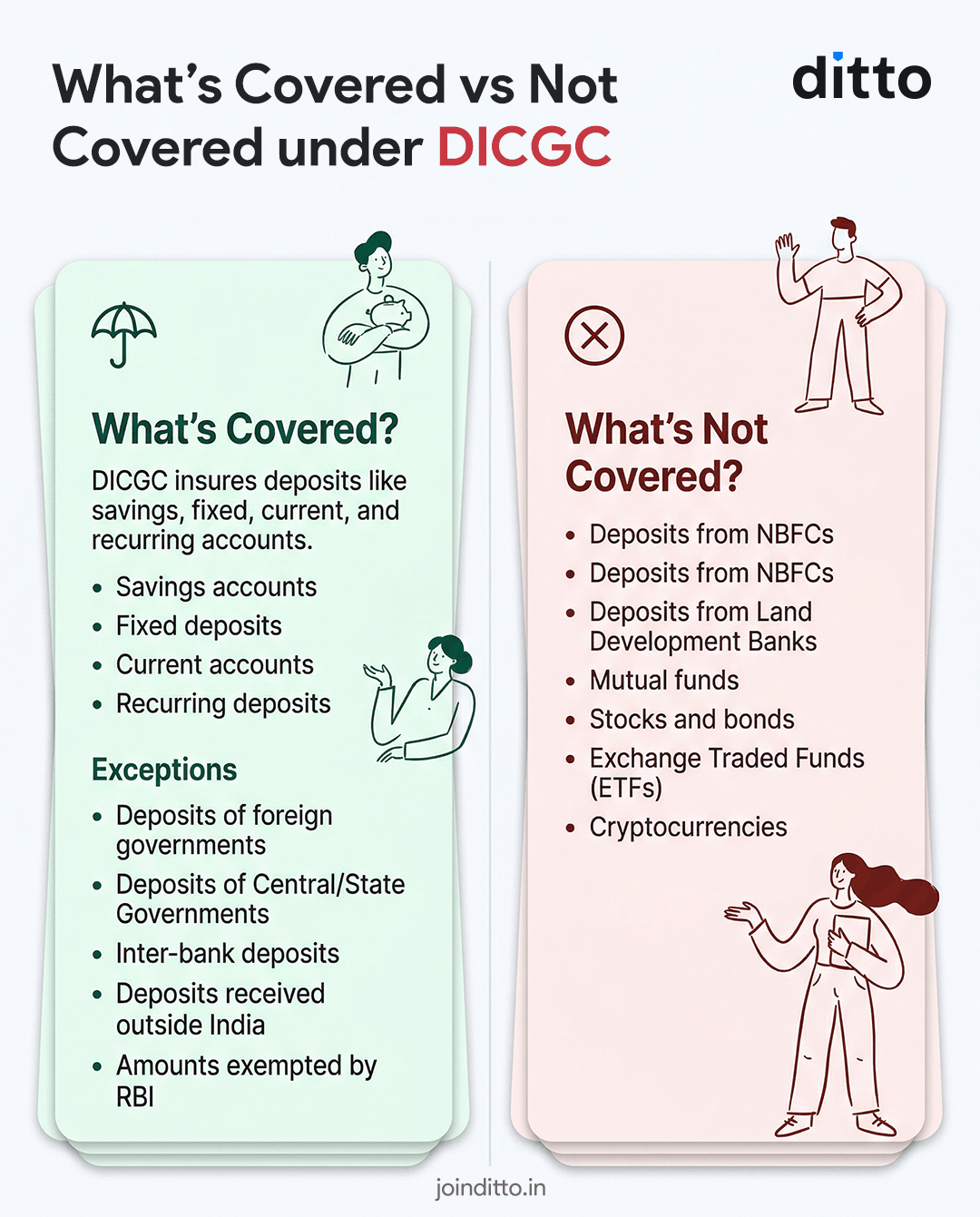

DICGC: Coverage Limit, Eligible Deposits & What's Not Covered

Deposits are insured up to ₹5 lakh per depositor per bank with all accounts in the same bank combined. The deposit insurance limit was increased from ₹1 lakh to ₹5 lakh in 2020. Coverage applies across commercial and cooperative banks.

The deposit-linked insurance scheme does not cover deposits held with Non-Banking Financial Companies (NBFCs), government deposits, interbank deposits, or investments such as chit funds, as these fall outside its deposit insurance framework.

Take a look at the infographic for a better understanding of what's covered and not covered in the scheme:

Note: You can access the list of insured and deregistered banks on the official DICGC website.

Cases Where DICGC Protection Proved Its Worth

When Does DICGC Pay Depositors?

- Bank under Moratorium: When the RBI notices that a bank is in serious trouble but doesn't shut it down immediately, it places it under All-Inclusive Directions (AID). Under such circumstances, DICGC must settle eligible deposits within 90 days as per the 2021 amendment.

- Bank in Liquidation: If a bank shuts down, a liquidator prepares and submits the depositor claim list. After receiving this list, DICGC pays insured amounts within 2 months. The overall timeline may extend due to claim verification and processing.

Did You Know?

Employee Deposit Linked Insurance (EDLI) Scheme Explained

The EDLI Scheme is a life insurance benefit provided by the Employees' Provident Fund Organization (EPFO) for employees enrolled in EPF. It offers financial protection to the nominee if the employee passes away during service.

The payout depends on the employee’s last drawn salary and EPF balance, with a minimum benefit of ₹2.5 lakh and a maximum of ₹7 lakh. There is no separate premium, as the employer contributes 0.5% of wages towards the scheme and claims are settled within 20 days.

Note: EDLI benefits are not restricted by location. Claims are payable even if the death occurs outside India, provided the employee was in service with an EPF-covered establishment at the time of death.

How to Maximize Your Deposit Protection in India?

Review and Rebalance Regularly

Monitor your deposits periodically. Interest accumulation can push your balance above ₹5 lakh, so reallocate funds when needed to stay within insured limits.

Choose Reliable Banks

Prefer scheduled commercial banks or well-established cooperative banks. Stronger institutions reduce risk and improve the chances of smooth claim settlement if needed.

Use Different Ownership Types

Hold deposits in different capacities, such as individual and joint accounts. Each ownership category is treated separately, which can help extend your overall insured coverage when structured carefully.

Spread Deposits Across Multiple Banks

Keep your deposits below ₹5 lakh per bank, as DICGC coverage applies per depositor per bank. When you split funds across banks, it ensures each portion stays fully protected.

Why Choose Ditto for Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Abhinav below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or chat on WhatsApp with us now!

Conclusion

Deposit insurance by the Deposit Insurance and Credit Guarantee Corporation is a strong safeguard that builds trust in the banking system and protects your savings if a bank fails. It offers real peace of mind, especially for everyday depositors.

However, opening multiple accounts in the same bank does not increase protection, as all balances are combined. A more practical approach is to spread funds across a few reliable banks and manage your deposits wisely.

Frequently Asked Questions

Last updated on: