Quick Overview

Insurance claims are meant to provide financial support during difficult times. However, not every claim gets approved. For many policyholders, knowing that their claim has been repudiated after paying the premiums for several years can be confusing and stressful, especially when the term itself isn’t widely understood.

In this article, we explain the claim repudiated meaning, how it differs from claim rejection, why insurers repudiate claims in both health and term insurance, and the steps you can take to avoid repudiation or respond if your claim is denied.

Why Do Insurers Repudiate Claims?

From our experience at Ditto, insurers often do not clearly distinguish between claim rejection and claim repudiation in practice. Instead, they usually mention the specific reason for denying the claim in the communication, which helps provide clarity to policyholders.

Common Reasons for Claim Repudiation in Health Insurance

1. Non-Disclosure or Misinformation

One of the most common reasons for claim repudiation in health insurance is providing inaccurate information or failing to disclose medical history and lifestyle habits when purchasing the policy or at the time of a claim.

2. Fraudulent or Inflated Claims

Claims may be repudiated if the insurer discovers fake hospital bills, manipulated invoices, or exaggerated treatment costs during claim verification.

3. Treatment Falling Under Policy Exclusions

If a claim falls under standard exclusions listed by the insurer, like cosmetic procedures and self-inflicting injuries, the insurer may repudiate it after reviewing the case.

4. Waiting Period Violations

Many health insurance policies include waiting periods for specific illnesses and pre-existing conditions. If treatment occurs during this waiting period, the claim may be denied.

Key Insight from IRDAI Guidelines for Health Insurance

Common Reasons for Claim Repudiation in Term Insurance

1. Non-Disclosure of Medical History

If the policyholder failed to disclose major illnesses, medical treatments, or surgeries while buying the policy, the insurer may repudiate the death claim during investigation.

2. Incorrect Lifestyle Disclosures

Lifestyle habits such as smoking, alcohol consumption, or risky hobbies must be declared during policy purchase. Misrepresenting these details can result in claim repudiation.

3. Misrepresentation of Financial or Occupational Details

Providing incorrect information about income, occupation, or employment status can also affect the policy’s validity and lead to claim repudiation, especially in the 1st 3 policy years.

4. Fraudulent Claims

In certain cases, insurers conduct investigations when the cause of death or the circumstances appear unusual. If fraud is suspected, the claim may be repudiated.

Key Insight from IRDAI Guidelines for Life Insurance

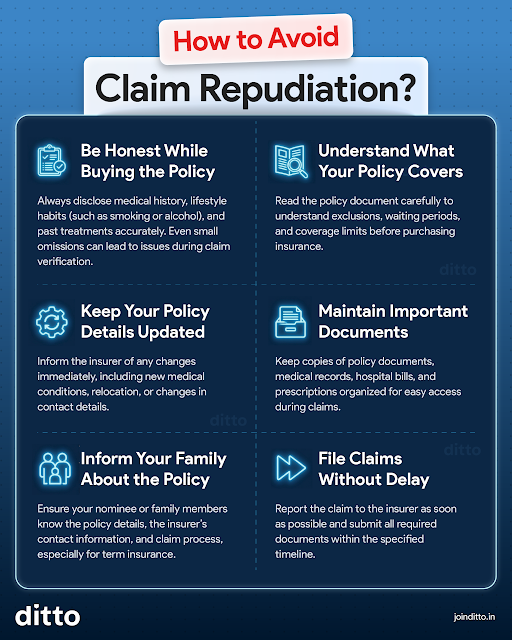

How to Avoid Claim Repudiation?

Refer to the following infographic for a few simple practices to significantly reduce the risk of claim repudiation.

Key Insight from IRDAI Annual Report

What To Do if Your Claim Is Repudiated?

1. Carefully Review the Repudiation Letter

Start by reading the insurer’s communication carefully. Under IRDAI regulations, insurers must clearly mention the reason for repudiation and reference the specific policy clause or condition that led to the decision.

2. Check the Policy Terms and Documents

Compare the insurer's reason for repudiation with the policy wording, exclusions, waiting periods, and disclosures made at the time of purchase. This helps you understand whether the repudiation is based on valid policy terms or a misunderstanding.

3. Contact the Grievance Cell

If you believe the claim was wrongly repudiated, you can reach out to your intermediary or Third Party Administrator (TPA) and raise a complaint with the insurer’s internal grievance redressal system. Provide supporting documents to clarify your case.

4. Escalate to the Insurance Ombudsman

If the issue is not resolved by the insurer, you can approach the Insurance Ombudsman, an independent authority that helps resolve disputes between insurers and customers.

5. Consider Consumer Court if Necessary

In cases involving significant disputes or unresolved complaints, you can escalate to the consumer courts to seek legal resolution.

Note: As per IRDAI, insurers must seek approval from the Product Management Committee (PMC) or Claims Review Committee (CRC) before repudiating a claim to ensure transparency and accountability.

Why Choose Ditto for Your Insurance Needs?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Abhinav below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation with us. Slots are filling up quickly, so be sure to book a call now or chat with us on WhatsApp!

Conclusion

A claim repudiated decision can feel alarming, but it usually stems from clear issues such as incorrect disclosures, policy exclusions, or misunderstandings about coverage terms. In most cases, these situations are preventable when policyholders provide accurate information and fully understand the conditions of their insurance policy.

Before buying or renewing any policy, take the time to review the policy wording, disclose all relevant details honestly, and ensure your family understands the claim process. These simple steps can significantly reduce the chances of disputes later.

Disclosure

Frequently Asked Questions

Last updated on: