Quick Overview

HDFC Life Insurance, founded in 2000 as a joint venture between HDFC and Standard Life (now Abrdn), is India’s leading private-sector life insurer and a publicly listed company with HDFC Bank as the majority stakeholder. This guide walks you through the plans offered by HDFC Life and its features.

Performance Metrics of HDFC Life

Term Plans Offered by HDFC Life

1. HDFC Life Click 2 Protect Supreme Plus (Flagship): Click 2 Protect Supreme Plus is a comprehensive term policy offering flexible smart exit, wellness benefits, premium break options, and enhanced protection features tailored to different life stages.

Some of its features are:

- Offers three variants: Life (with level or increasing cover options), Life Plus (with an added accidental death cover), and Life Goal (decreasing cover option).

- Provides terminal illness cover up to ₹2 crore (Accelerated), payable if two doctors certify in writing that the insured has less than six months to live. However, this is not applicable if the diagnosis happens after age 80.

- Instant Payout on Claim Intimation, where a portion of the death benefit is paid to the nominee within one working day after claim intimation (subject to necessary documentation and a 1-year waiting period). If the sum assured is ₹1 crore or more but less than ₹2 crore, an instant payout of ₹2 lakhs is provided. For covers of ₹2 crore and above, ₹5 lakhs is paid. However, this benefit is not available if the sum assured is below ₹1 crore.

- Premium Break Benefit allows for a one-year premium deferment after five policy years, provided coverage continues. This can be used multiple times during the policy term, with a 5-year gap between usages, and deferred premiums must be paid later. If death occurs during a premium break, deferred premiums are deducted from the final payout.

- Special Premium Break for Women allows female policyholders to defer premiums for 12 months in case of pregnancy (can be exercised during pregnancy or within 6 months of labor) or the death of a spouse within 6 months from the date of death (after 2 policy years).

- Smart Exit allows you to surrender the policy and recover all premiums after 25 years, subject to certain conditions and a minimum 31-year term.

Add-ons You Can Opt For:

- Critical Illness Rider: Covers 60 specified critical illnesses for up to 15 years. Provides a lump-sum payout on diagnosis to help with treatment and income loss.

- Accidental Income Benefit: Pays 1% of the rider sum assured every month for 10 years in case of total and permanent disability due to an accident.

- Waiver of Premium Rider: Waives future premiums for the entire premium payment term, while keeping the policy active, on diagnosis of covered critical illnesses or disabilities.

- Waiver of Premium on Accidental Death of Husband: In case of the accidental death of the husband, future premiums are waived while coverage continues. This is available only for married women.

- Life Stage Option: Allows an increase in sum assured on key life events such as marriage, childbirth, or home purchase (via loan). However, it is subject to financial eligibility and caps.

- Education Income Benefit: On the death of the policyholder, the total payout payable will be equal to 10% of the SA (up to a maximum of ₹10 lakhs). The payouts will be made in equal installments till the child turns 25 (based on the chosen frequency). However, only one child can be covered.

- Spouse Cover Option: Offers an additional death benefit (up to 50% of base sum assured) to the spouse after the life assured’s death. Comes with strict eligibility rules and is generally not recommended if the spouse is working.

Besides these, the plan also offers an ROP option, parent protect care, and the option to renew your plan at maturity.

Annual Premiums Across Ages

Note: The listed premiums are indicative in nature for healthy, non-smoker profiles, living in a tier-1 city like Delhi (pincode: 110051), covered for a sum assured of ₹2 crores till the age of 70 (without first-year discounts).

2. HDFC Life Click 2 Protect Elite Plus: The Elite Plus term plan is a reasonable choice for affordable, high-cover term insurance. It offers essential protection features, but falls short in some areas, such as the absence of an in-built terminal illness benefit and limited options to increase cover over time. It offers a sum assured of ₹2 cr to ₹5 cr.

Some of its Features Are:

- Death claim intimation, ₹5 lakh is paid within one working day after document submission. Once the claim is approved after the 1-year waiting period, the balance is paid. If rejected, the ₹5 lakh is recovered.

- Get back all premiums paid with the Smart Exit Benefit and option to defer premiums for 12 months while coverage continues with a premium break.

- Key add-ons include a Critical Illness rider covering 60 illnesses for up to 15 years, Waiver of Premium on CI/disability, and an Accidental Income benefit paying 1% monthly for 10 years. Accidental death benefit and ROP riders are also available.

Annual Premiums Across Ages

Note: The listed premiums are indicative in nature and for a non-smoker profile, with a sum assured of ₹ 2 crore (Coverage till age 65, without first-year discounts).

3. HDFC Life Click 2 Protect Ultimate: The policy offers solid protection but comes with several limitations, like higher premiums and an absence of essential riders. It offers a sum assured of ₹1 cr to ₹3 cr, only for salaried folks residing in tier-1 cities.

Some of its Features Are:

- Smart Exit Benefit allows policyholders to surrender their policy and get back all premiums paid, with similar t&c as for the other 2 plans.

- Terminal Illness Benefit provides coverage up to ₹2 crore with a waiting period of 6 months from policy issuance.

- The plan offers a 100% claim guarantee, except in specific cases. Claims are not payable if death occurs due to suicide within the first policy year or as a result of intoxication, and as per other t&c.

Annual Premiums Across Ages

Note: The listed premiums are for a non-smoker profile, with a sum assured of ₹ 2 crore (Coverage till age 65, without first-year discounts). The premiums are indicative in nature as they can vary based on your age, health conditions, lifestyle choices, underwriting decisions, etc.

Besides the plans discussed above, HDFC Life’s older Click 2 Protect Life has limited availability in 2026 and is largely being phased out.

HDFC Life Click 2 Protect Supreme Plus Across Term Policies

Note: The listed premiums are indicative in nature and for a non-smoker profile, male with a sum assured of ₹2 crore (Coverage till age 70, without first year discounts).

Key Insight: Despite higher premiums, C2P Supreme Plus stands out for HDFC Life’s strong brand, scale, reliable post-sales service, rich feature set, and improved discounts, making it a dependable and well-rounded term insurance option.

Inclusions and Exclusions of HDFC Term Insurance

Note: As per IRDAI rules, if the policyholder dies by suicide within the first year of buying or reviving the policy, the insurer will reject the claim and refund around 80% of the total premiums. Exclusions may vary from plan to plan.

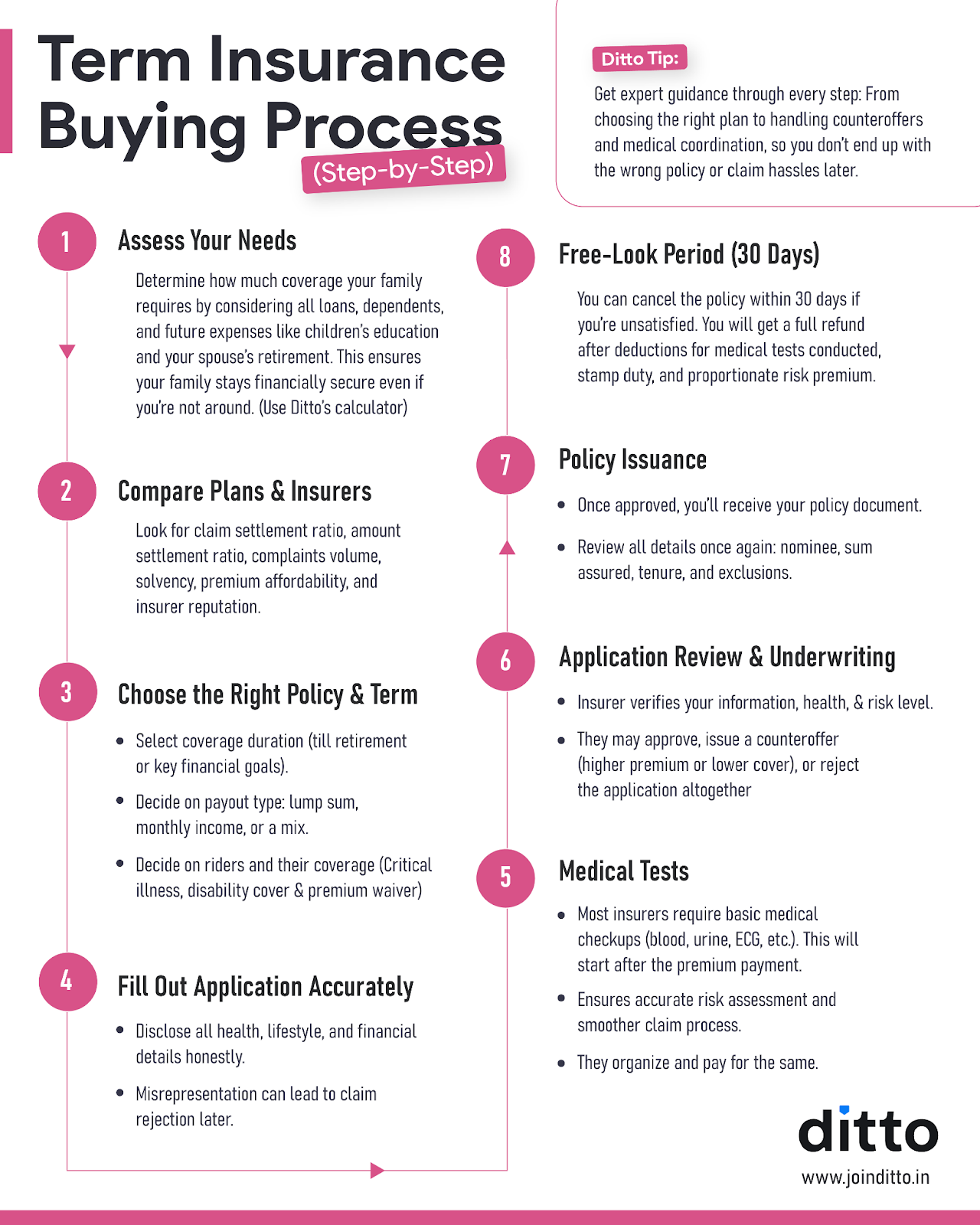

How To Buy HDFC Life Term Plans Online in 2026?

What are the Documents Required To Buy HDFC Life Term Insurance Plan?

- Identity proof like Pan card or a Passport

- Address proof like Aadhaar card or a utility bill

- Age proof, like a birth certificate

- Income proof like Salary slips, Form 16 or bank statements

- Recent passport-size photo

- Medical tests, if required, based on age or cover amount

What are the Things To Consider Before Buying HDFC Term Plan?

Before buying an HDFC term plan, you must assess the right sum assured, policy term, and premium affordability. Review the insurer’s metrics, rider options, and long-term features to ensure the plan aligns with your family’s financial needs.

Learn more about what to consider when purchasing a term plan.

Note: It is important to estimate the correct term cover you require. To get a better understanding, use this online calculator to find the ideal cover for you.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why do customers like Vijay below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat with us on WhatsApp!

Ditto’s Take on HDFC Term Insurance

In 2026, HDFC Term Insurance is a preferred choice for individuals seeking reliable and flexible life coverage. For most people, we recommend choosing the current feature-rich flagship plan, C2P Supreme Plus, as it offers greater flexibility, multiple rider combinations, and broader overall coverage.

HDFC Life is our partner. If you’d like expert advice on whether HDFC Term plans fit your long-term needs, book a call with us. At Ditto, we recommend comprehensive plans, which align with your long-term goals. Explore more about how our experts evaluate term plans through Ditto’s cut.

Frequently Asked Questions

Last updated on: