You’ve probably heard the question before, “Is term insurance worth it if there’s no return?” It’s one of the biggest reasons people hesitate to buy term plans. After all, nobody likes the idea of paying premiums for decades and getting nothing back. In fact, it is estimated that around 5% of the policies sold in India are term insurance policies.

But why is this the case? After all, term insurance was never meant to be an investment. Its actual value lies in pure protection. It does not give you any returns. It’s designed to give your family a financial safety net if something happens to you, not to grow your wealth or offer maturity benefits. So instead of asking “What do I get from this?”, the better question is “What happens to my family if I’m not around?”.

Once you look at it that way, the utility of term insurance becomes crystal clear.

Heads Up: It takes an average person up to 5 hours to read & analyze a policy, and 10 hours or more to compare different plans and make a decision.

This is why we propose a better alternative - taking a FREE consultation with Ditto’s certified advisors. We have a spam-free guarantee, and we’ll never push you to buy a plan. Don’t delay this - we have limited slots every day, so book a quick call here before they run out.

Is Term Insurance Good in 2025?

Term plans offer pure risk cover. This means your nominee receives a lump sum if you pass away during the policy period. If you survive the term, there’s no payout. But in return for giving up maturity benefits, you get something incredibly valuable: high coverage at a very low cost.

This makes it the most cost-effective form of life insurance. For instance, a healthy 30-year-old can get a ₹1 crore cover for as little as ₹10,000 - 12,000 annually, roughly the cost of one restaurant meal per month.

Unlike savings-linked policies, term plans are straightforward. There are no complex bonus structures or market-linked NAVs to track. Just straightforward protection for your family.

Term insurance is good because it delivers high coverage for low premiums when you need it most.

Benefits of Term Insurance

One of the biggest advantages of term insurance is its affordability. Whether you’re buying ₹50 lakh or ₹1 crore of coverage, the premiums are significantly lower than traditional life insurance plans.

Another major benefit is financial protection for your dependents. If you’re the sole or primary earner, a term plan ensures that your family isn’t left struggling with EMIs, school fees, or basic living costs if something happens to you.

You also get tax benefits: premiums qualify for deduction under Section 80C under the old regime, and the death benefit is exempt under Section 10(10D), subject to certain conditions.

Finally, term plans come with optional riders, such as critical illness cover, accidental death benefit, and waiver of premium. These enhance your protection and address real-world risks, often at marginal additional cost.

Term plans offer strong benefits, affordability, protection, and tax relief, without the complexity of savings-based insurance.

Why Term Insurance is a Good Fit for Most Indians

In India, the average household depends heavily on a single earning member. Whether you’re supporting aging parents, a spouse, or school-going kids, your income likely covers everything from rent to groceries to future aspirations.

A term insurance plan acts as a replacement for that income. If something happens to you, your family won’t have to depend on relatives or dip into savings just to manage daily life.

It also ensures that your loans don’t become a liability for your loved ones. Home loans, personal loans, and even credit card dues don’t disappear when you do. A term plan can wipe them off instantly.

Lastly, it helps your family maintain their current lifestyle, without cutting back on essentials like education or healthcare.

For most Indian households, term insurance provides critical income protection and debt relief in the event of the worst-case scenario.

When is Term Insurance Not a Good Fit?

If you’re financially independent with zero dependents, then term insurance might not be necessary. For example, a 45-year-old with no spouse, no kids, and enough investments to last a lifetime may not need life insurance at all.

Similarly, if you’re looking for returns, term plans will disappoint. That’s where products like ULIPs or endowment plans come in, but they’re significantly more expensive and often give subpar returns compared to mutual funds or PPF.

At Ditto, we often recommend keeping insurance and investments separate. If you want to grow your money, invest in a good fund. If you want to protect your family, get a term plan. Mixing the two usually results in average outcomes on both fronts.

Skip term insurance only if no one depends on you financially and you don’t expect future dependents as well, but don’t ditch it just because it doesn’t offer returns.

Term Insurance vs Other Life Insurance Policies

When you compare term plans with other types of life insurance, like endowment, whole life, or ULIPs, the most significant difference is cost and purpose.

- Traditional plans combine savings and protection. But the premiums are 5–10x higher, and the actual life cover is often too low to be meaningful.

- ULIPs offer market-linked returns but come with high charges and a five-year lock-in period. They’re also vulnerable to market risks.

With a term plan, you’re buying pure protection. And if you invest the premium savings elsewhere, say in mutual funds or PPF, you usually end up with better returns and sufficient coverage.

Here’s a table summarizing the same:

| Feature | Term Insurance | Endowment / Whole Life | ULIP (Unit Linked Insurance Plan) |

|---|---|---|---|

| Purpose | Pure protection | Protection + Savings | Investment + Insurance |

| Premiums | Low | 5–10x higher than term | Moderate to high |

| Life Cover | High (₹50L–₹1Cr+ possible) | Low (often inadequate) | Moderate |

| Returns | None | Guaranteed (but low) | Market-linked |

| Charges | Minimal | Moderate (admin fees, etc.) | High (fund management, allocation charges) |

| Lock-in Period | None | Applicable | Applicable |

Term insurance, combined with separate investments, beats savings-linked life insurance for most people.

Should You Consider Return of Premium (ROP) Plans?

Return of Premium (ROP) plans are a hybrid version of term insurance. If you survive the term, the insurer returns all the premiums you paid, excluding GST and rider costs.

At first glance, this sounds like a win-win. But there’s a catch: the premiums are 70-100% higher than regular term insurance. And you could generate better returns by simply buying a plain term plan and investing the premium difference in a mutual fund or fixed deposit.

That said, ROP plans can be beneficial for risk-averse individuals who are uncomfortable with the “use it or lose it” concept of term insurance. Please be aware that what you receive is your money, not any additional amount.

ROP plans offer psychological comfort, but aren’t as cost-efficient as plain term insurance with separate investments.

Who Should Buy Term Insurance?

Here’s our expert insight: if someone depends on your income, you should consider term insurance. This includes salaried employees, freelancers, small business owners, and even homemakers who are co-borrowers on loans. If your absence would create a financial gap for your spouse, children, parents, or even a sibling, then a term plan ensures they don’t have to struggle to maintain their lifestyle or meet future goals.

Common Myths About Term Insurance

Let’s bust a few myths that stop people from making wise choices:

- “It’s a waste if I outlive the term.”Not true. The goal is protection, not returns. It’s like fire insurance, you hope you never need it, but it’s invaluable when you do. Remember, you should always have protection.

- “Only earning members need term insurance.”Not necessarily. Even homemakers, freelancers, or co-borrowers on loans should consider coverage if their absence would financially strain the household.

- “I’ll buy it later.”Waiting drives up your premium. A 30-year-old might pay ₹10,000/year for ₹1 crore coverage. By 40, that could double, or worse, your health might decline and disqualify you.

Myths around returns, timing, and eligibility often delay critical protection; don’t fall for them.

Who Should Buy Term Insurance and When?

The best time to buy term insurance is when you have people depending on your income, be it a spouse, children, or aging parents. The earlier you buy, the lower your premiums will be.

You don’t have to be salaried. If you’re a freelancer, business owner, or even a homemaker with joint loans, term insurance can help protect your household from future financial stress.

And yes, even young professionals in their 20s should consider it. Not because they need huge coverage now, but because locking in a low premium early can save lakhs over the policy term.

If anyone depends on your income, you need term insurance, and the earlier you buy, the better.

Best Term Insurance Plans in India in 2025

In case you’re looking for some of the top policies in the country, take a look at this table:

| Feature | Term Insurance | Endowment / Whole Life | ULIP (Unit Linked Insurance Plan) |

|---|---|---|---|

| Purpose | Pure protection | Protection + Savings | Investment + Insurance |

| Premiums | Low | 5–10x higher than term | Moderate to high |

| Life Cover | High (₹50L–₹1Cr+ possible) | Low (often inadequate) | Moderate |

| Returns | None | Guaranteed (but low) | Market-linked |

| Charges | Minimal | Moderate (admin fees, etc.) | High (fund management, allocation charges) |

| Lock-in Period | None | Applicable | Applicable |

Why Talk to Ditto for Your Term Insurance?

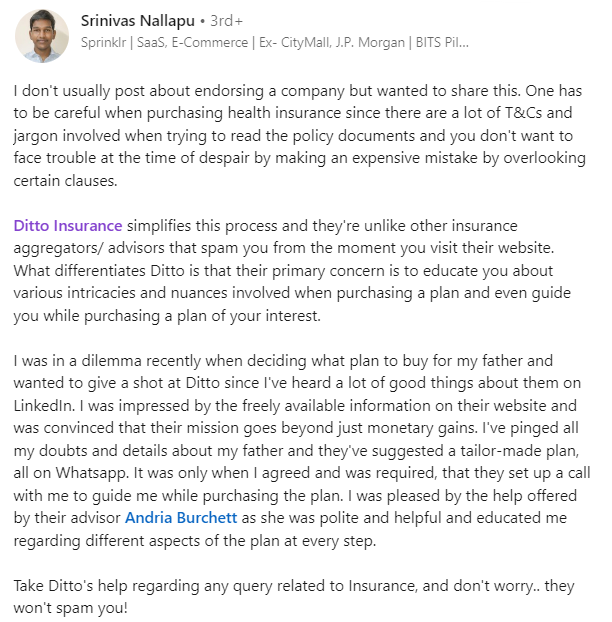

At Ditto, we’ve assisted over 3,00,000 customers with choosing the right insurance policy. Why customers like Srinivas below love us:

✅No-Spam & No Salesmen

✅Rated 4.9/5 on Google Reviews by 5,000+ happy customers

✅Backed by Zerodha

✅100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now!

Conclusion: Is Term Insurance Good for You?

If you’re still wondering whether term insurance is worth it, here’s a quick summary to help you decide:

- If your absence would cause financial stress for your family, term insurance is non-negotiable. It covers everything from monthly expenses to long-term liabilities, ensuring your loved ones don’t struggle to maintain their lifestyle.

- It’s the most affordable way to secure large coverage. For a relatively small annual premium, you can create a multi-crore safety net — something that’s nearly impossible with savings-linked plans.

- Insurance and investments work best when they’re separate. Term insurance gives you the protection you need while allowing you to invest the premium savings more efficiently elsewhere.

Bottom line: If protection is your goal, and affordability is key, term insurance is the smartest choice you can make. Need help choosing the right one? Chat with a Ditto advisor to find a plan that fits your needs and budget.

Last updated on: