Is SBI Life Insurance Good?

SBI Life Insurance was incorporated on October 11, 2000, and is registered with the Insurance Regulatory and Development Authority of India (IRDAI) under registration number 111. Since then, it has grown into one of the leading listed life insurance companies in India.

This guide helps you understand whether SBI Life Insurance is good or bad for you, based on its features, performance, and overall value.

SBI Life Insurance: Performance Metrics

Note: The above metrics reflect the overall performance of SBI Life Insurance and are not limited to its term products.

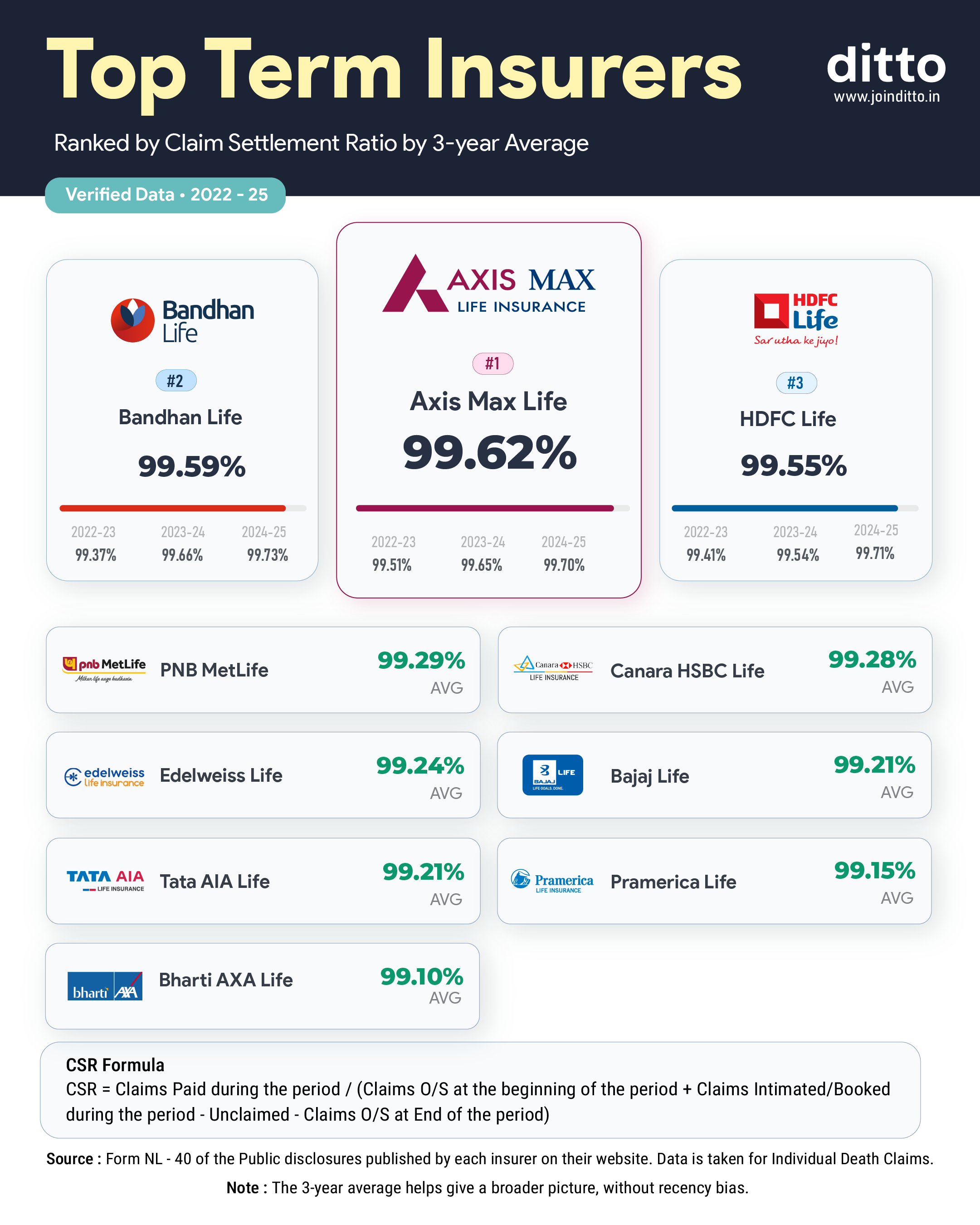

Top 10 Term Insurers by CSR

SBI Life has a high CSR, but it does not rank among the top 10 insurers on this metric. Check the infographic to see which insurers make the top 10 list.

Plans Offered by SBI Life Insurance

- Smart Shield Plus: The policy offers multiple cover options, including level, increasing, and future-ready protection. It also includes optional features like the Better Half Benefit, whole life cover, and an Accident Benefit Rider for added protection.

- eShield Insta: A simple, digital-first term plan that offers both pure protection and a Return of Premium (ROP) option. It starts with a ₹10 lakh cover and offers policy terms up to 10 years. The ROP variant also provides a maturity payout and builds surrender value over time.

- Smart Shield Premier: The policy is designed for high coverage needs with a minimum sum assured of ₹2 crore. It offers both level and increasing cover options, flexible payout choices, an optional Accident Benefit Rider, and coverage up to age 85 in a simple, easy-to-understand structure.

Note: Other term plans offered by SBI Life Insurance include Smart Swadhan Neo, Smart Swadhan Supreme, Saral Swadhan Supreme, and Saral Jeevan Bima. Applicants are advised to review the availability, features, and eligibility criteria for each plan on the insurer’s official website before making a decision.

Point to Note

Key Benefits of SBI Life Insurance

- Strong SBI-Backed Distribution: Backed by State Bank of India, SBI Life has a deep reach across India through agents and over 1000 offices. This makes servicing and support easier across both urban and semi-urban locations.

- One of the Largest Life Insurers: SBI Life is the second-largest life insurer after LIC (Life Insurance Corporation of India) by business volume in India.

- Financial Strength and Stability: With a high solvency ratio and a large portion of investments in AAA and sovereign instruments, SBI Life offers strong balance-sheet quality. This is important for long-term commitments like savings and retirement plans.

Premiums Across Plans and Ages

Note: The listed premiums are for non-smoker profiles residing in Delhi, with a sum assured of ₹2 crore (coverage until age 70, without first-year discounts). The premiums are slightly lower than those of other plans, as Smart Shield Plus misses out on in-built features like waiver of premium (WOP). HDFC offers the WOP as an inbuilt feature, while Axis Max offers it as a rider.

Drawbacks of SBI Life Insurance

- Some insurers outperform SBI Life on key claim metrics, with Axis Max Life (99.62%) and HDFC Life (99.55%) showing comparatively stronger claim settlement performance over FY 2022 to FY 2025.

- SBI term plans lack several modern features commonly found in most term policies, including terminal illness benefit, auto cover continuance, and health management benefits.

- The insurer falls short by not offering useful riders like critical illness, which may limit overall coverage flexibility.

Who Should Opt For SBI Life?

- Individuals looking for flexible coverage with options like level cover with future proofing benefit, spouse-linked benefits, and multiple payout choices.

- Those who prefer simple, short-term, or digital-first insurance solutions for basic protection needs.

- High-income individuals seeking ₹2 crore or higher coverage with a clean, straightforward term plan and minimal complexity.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Vijay below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right term insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or WhatsApp us now, slots fill up fast!

Conclusion

SBI Life has consistently maintained a high claim settlement ratio with relatively low complaint volumes. It also offers simple, easy-to-understand plans, making it a dependable choice for many buyers.

However, compared to newer term plans, it feels slightly dated, with fewer modern features and rider options. For more flexibility and value, consider the best term insurance companies aligned with your long-term goals.

Frequently Asked Questions

Last updated on: