Axis Max Life Insurance is a joint venture between Axis Bank (20%) and Max Financial Services (80%). Formerly known as Max Life Insurance, it was rebranded on December 13, 2024. The company now operates with over 400 branches across India and abroad. Axis Max Life’s claim settlement ratio stands at an impressive 99.70% in FY 2024-25.

Axis Max Life Insurance is a leading private insurer that blends strong distribution through Axis Bank with a wide range of modern, flexible life insurance plans designed for today’s evolving financial needs.

This guide walks you through Axis Max Life Insurance, covering its plans, features, performance metrics, and whether it fits your long-term financial protection needs.

Looking for a term plan offered by Axis Max Life? Book a free call or chat on WhatsApp with a Ditto advisor, and let us help you out.

Did You Know?

In a March 6, 2026, stock-exchange filing, Max Financial Services announced it is considering a merger with Axis Max Life Insurance, subject to regulatory approvals. The move aims to list Axis Max Life separately, allowing Max Financial shareholders to hold shares in the insurer directly.

Axis Max Life Insurance: Performance Metrics

Metrics

Average FY 22-25

Industry Average

Key Insight

Claim Settlement Ratio (CSR)

99.62%

98.66%

A CSR (above the recommended mark of 97%) reflects very strong claim settlement consistency, indicating a high likelihood of claims being honored smoothly.

Amount Settlement Ratio (ASR)

96.37%

94.83%

An ASR of 96.37% suggests balanced claim payouts, ensuring both small and large claims are settled fairly. The metric is well above the recommended 90% mark.

Annual Business Volume (in crore)

₹10,719

₹3,411

A significantly higher business volume highlights the insurer’s strong market presence and widespread customer base. Business is thrice the industry average and above the recommended mark of ₹5000 crore.

Amount Paid in Death Claims (in crore)

₹1,316.2

₹195.05

Higher total death claims paid indicate a strong financial capacity to reliably meet large claim obligations.

Volume of Complaints Per 10,000 Claims

5.67

17.67

A lower complaint ratio indicates a better customer experience and fewer issues, despite handling a high volume of policies.

Solvency Ratio

1.88x

2.04x

A solvency ratio of 1.88x remains comfortably above regulatory requirements, indicating strong financial health and ability to meet future claims.

Note: The above metrics reflect the overall performance of Axis Max Life Insurance and are not limited to any particular insurance product.

To understand how insurers perform using official disclosures, visit Ditto Data Lab. It contains term insurance data collected from reliable sources and curated by our team.

Offers 6 variants and covers 64 critical illnesses (with add-on). The plan includes a terminal illness payout and a premium waiver, plus a ₹2 lakh instant payout and health services.

Individuals looking for a term plan that can be tailored to key life milestones, rather than just offering a fixed lump sum payout on death.

The plan offers a simpler structure with level coverage and flexible payouts. It includes terminal illness benefit up to ₹1 crore, a cover continuance option, and instant payout at claim intimation.

Individuals seeking a strong pure-protection term plan with claim payout flexibility, long coverage duration, and a built-in exit option.

The policy offers terminal illness payout up to ₹1 crore and a special exit value. It also includes an accident cover, return of premium (ROP), and a premium break option.

Suitable for those looking for a feature-rich protection plan with options like joint life cover, premium break flexibility, and the ability to top up in the future.

Take Note

Besides the above-listed term plans offered by Axis Max, the insurer also offers plans that include:

ULIPs like Fast Track Super and Flexi Wealth Plus.

Savings Plans like Axis Max Life Smart Wealth Advantage Guarantee Elite Plan.

Children's Plans like Axis Max Life Shiksha Plus Super Plan.

Retirement Plans like Axis Max Life Forever Young Pension Plan.

However, at Ditto, we are against plans that combine insurance and investment. Such plans not only offer less life cover but also tend to be less efficient than buying a term plan and investing separately.

Riders Available in Axis Max Life Insurance Plans

Waiver of Premium Plus Rider: This rider ensures your policy stays active even if you’re unable to pay premiums due to a disability or critical illness, as future premiums are waived.

Critical Illness and Disability Rider: It provides a lump sum payout if you are diagnosed with a listed critical illness or suffer a disability, helping you manage treatment costs and income loss.

Accidental Death and Disability Rider: This rider offers additional financial support in case of accidental death or dismemberment, giving your family extra protection beyond the base life cover.

Premium Comparison for Axis Max Smart Term Plan Plus

Age

Male

Female

25

₹10,773

₹9,158

30

₹13,581

₹11,544

35

₹17,740

₹15,079

40

₹23,608

₹20,067

45

₹31,016

₹26,364

Note: The listed premiums are for a non-smoker profile with a sum assured of ₹1 crore (coverage till age 70, without first-year discounts). The illustrative figures show how premiums increase with age, and that premium pricing for women is up to 15% cheaper than for men.

CTA

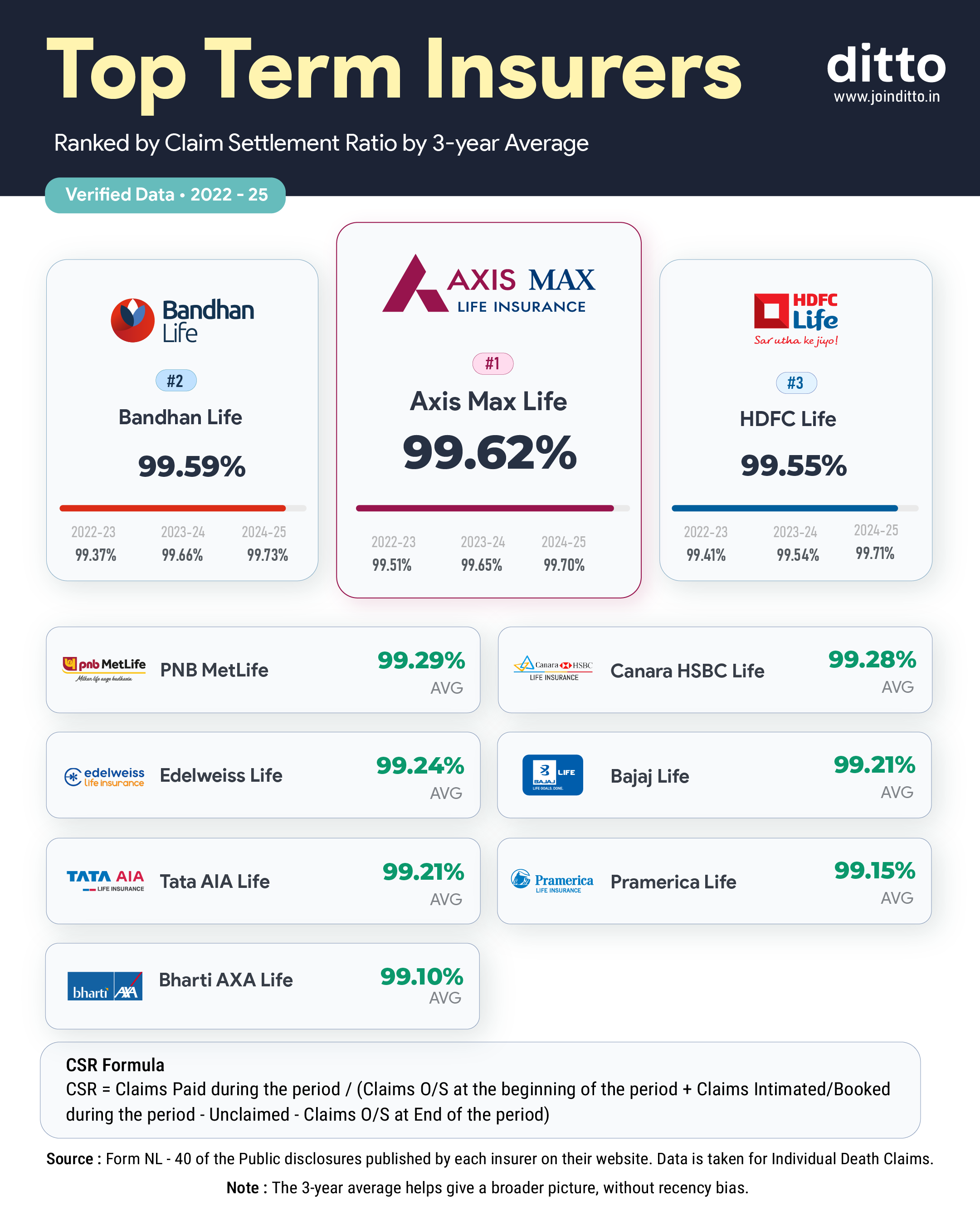

Top 10 Life Insurance Companies in India by Claim Settlement Ratio

Take a quick look at the infographic to see which insurers make the top 10 list.

Take Note: Axis Max Life tops the list in CSR, highlighting its strong track record in consistently honoring claims.

Why Choose Ditto for Life Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

Backed by Zerodha

100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

Axis Max Life Insurance offers a wide range of insurance products, including ULIPs that combine insurance with market-linked investments. However, buying a standalone term life insurance policy for protection and investing separately through options such as mutual funds can provide greater coverage and better returns.

If you are looking for a term plan from Axis Max, we recommend:

Smart Term Plan Plus, which is the insurer’s current flagship plan and ranks first on our list of best term insurance plans, offering comprehensive features and strong overall value.

Axis Max Life Smart Total Elite Protection (STEP) Term Plan and Smart Secure Plus are secondary options, best suited for specific needs and available through select channels.

However, if you wish to explore beyond Axis Max Life, we recommend the best term insurance companies that offer comprehensive term plans that align with your future goals.

Disclaimer: Axis Max Life Insurance is one of Ditto’s partner insurers. The information in this guide is based on publicly available sources and insurer disclosures and is shared for educational purposes only.

Frequently Asked Questions

How can I find Axis Max Life Insurance branches near me?

You can locate Axis Max Life branches using the official branch locator on their website. Furthermore, many Axis Bank branches also offer Axis Max Life services for added convenience.

Is a policy loan available under Axis Max Life Term Insurance?

Pure term plans do not offer a loan facility. However, the Smart Secure plan offers this only under the Return of Premium variant, once a surrender value is built, allowing loans up to 75% of that value.

How can I contact Axis Max Life Insurance?

You can reach Axis Max Life through their customer care helpline at 1860-120-5577. You can also mail them at service.helpdesk@axismaxlife.com, or chat via their WhatsApp number at 7428396005.

What types of life insurance plans does Axis Max Life offer?

Axis Max Life offers a range of plans, including term insurance, savings plans, ULIPs, and retirement solutions, catering to different financial goals and risk preferences.

Can I buy Axis Max Life Insurance policies online?

Yes, many Axis Max Life plans, including flagship term policies, can be purchased online through the insurer’s website and via licensed advisors and digital platforms like Ditto.

Axis Max Life Customer Reviews

4.7

96 reviews

Axis Max Life has the highest claim settlement ratio in the industry at 99.6% and that is exactly why I chose them. The issuance was fully digital and the policy document was detailed and clear. Very happy with this decision.

KS

Karthik Suresh

The Smart term plan plus has excellent flexibility — I could choose my premium payment term and the cover continuance feature gives real peace of mind. A great product at a very competitive price point.

RS

Riya Sharma

The cover continuance benefit on my Axis Max Life plan means my family stays protected even if I miss a premium due to job loss. That thoughtful feature is what sets them apart from most other term insurers.

AV

Asha Venkataraman

I was confused about which riders to add to my Axis Max Life plan and my Ditto advisor patiently explained each one and helped me pick only what I genuinely needed. That personalised guidance was invaluable!

AP

Arun Pillai

Axis Max Life's branch presence is more limited compared to older insurers like HDFC Life, which can be inconvenient for those who prefer in-person servicing. The app works well for most things but more offline support would be appreciated.

MR

Manish Rao

Last updated on:

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your

convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We

promise no spam and a hassle-free experience.

Buy from Ditto

Talk to us and we will help you shortlist a policy, fill the application and make the best purchase you can

Get on a call with us

We have around 50 slots open each day. Pick a time and we will call you at your convenience.

WhatsApp us

If you'd much rather prefer texting at your own pace, just hit us up on WhatsApp. We promise no spam and a hassle-free experience.

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.