What is a Survival Period in Health Insurance?

When buying health or critical illness insurance, most people focus on premiums, coverage, and claim processes. But there’s one lesser-known detail that could make a big difference when it matters most: the survival period.

Understanding benefit-based vs. indemnity-based policies makes the concept of a survival period much clearer. Let’s take a quick look:

In this guide, we’ll explain precisely what the survival period is, how it works, and how it differs from standard waiting periods. By the end, you’ll be better prepared to choose a health plan that truly meets your needs, without any last-minute surprises.

Why Does Critical Illness Insurance Have a Survival Period?

You might wonder, “Why must I survive 30 days to get a payout?”

Here’s why: critical illness (CI) insurance is meant to support your recovery, not serve as a death benefit. If the illness is fatal early on, your term life insurance covers your family financially. But if you survive, the CI plan helps you manage non-medical costs like lost income, daily expenses, or home adjustments.

Remember, each insurance product plays a unique role:

- Term life protects your family

- Health insurance covers hospital bills

- Critical illness protects you during recovery

That’s why the survival period exists.

How Long is the Typical Survival Period in Health Insurance Plans?

There's no survival period in standard health insurance plans, since these policies focus on covering medical treatment costs rather than offering lump-sum payouts after a diagnosis.

However, if you’ve added critical illness coverage to your health or term insurance, or have a standalone critical illness policy, a survival period of 14 to 30 days usually applies. This means you must survive for that duration after being diagnosed with a covered illness or undergoing a covered surgery for the insurer to approve the claim. It helps ensure the benefit is paid only for severe, life-impacting conditions.

That’s why it’s wise to choose one with the shortest survival period available when selecting a critical illness rider.

A shorter survival period, say, 14 days instead of 30, reduces the risk of your claim being rejected if the illness proves rapidly fatal. It ensures your family is more likely to benefit, even in severe cases where recovery is uncertain.

Simply put:

The shorter the survival period, the greater the chances of your payout being honored, providing timely financial support when needed most.

Examples of Survival period

Did You Know?

Difference Between Waiting Period and Survival Period in Health Insurance

Understanding the difference between waiting and survival periods in health insurance is essential for making informed coverage choices. Let's take a quick look at the comparison table:

Do You Get Return on Premium if You Do Not Survive the Survival Period?

In most cases, you won’t get a return on premium if the insured person doesn’t survive the required survival period under a critical illness rider.

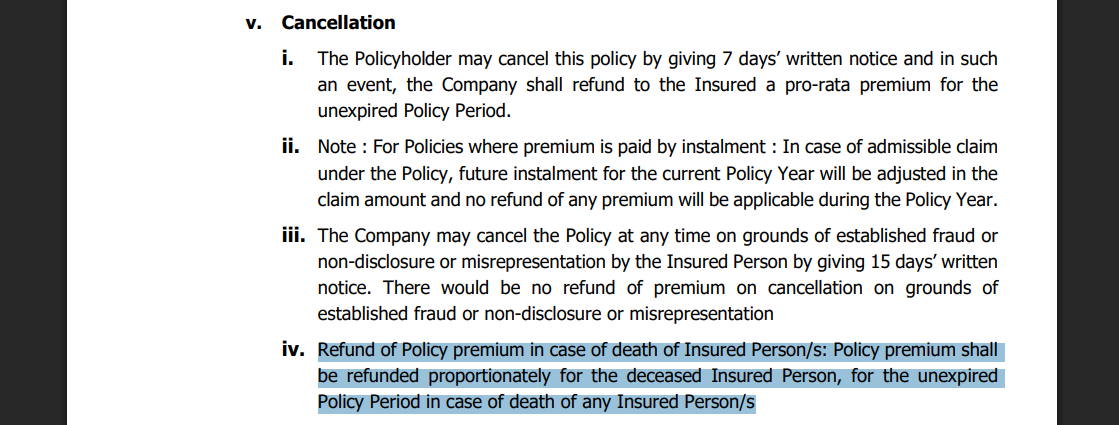

However, in case of a standalone policy ( such as HDFC ERGO Standalone CI policy), proportionate premiums may be refunded if no prior claim is made, only for that particular year.)

Here’s a snippet from the policy wording stating such premium returns:

Critical illness and other riders are structured to pay a lump sum benefit only if the insured survives a set number of days (usually 14 to 30) after being diagnosed with a covered illness or suffering a serious injury.

If the person passes away before completing that period, the claim becomes invalid and no payout is made, regardless of how much premium was paid. That’s why it’s essential to clearly understand these terms before adding such riders to your policy.

Did You Know?

How to Choose the Right Survival Period in Health Insurance? (Ditto’s Take)

First, ensure the plan or rider fits your needs, check the number of illnesses covered, their severity, and the insurer’s track record (claim settlement ratio, complaints, financial stability). Once that aligns, secondary factors like the survival period and other policy conditions should be evaluated.

The survival period may seem like a small detail, but it can make a big difference when you make a claim, especially with a critical illness rider. Here's how to make the right choice:

- Go for the shortest survival period available (usually 14 days). It lowers the risk of your claim being denied if the illness is rapidly fatal.

- The cost difference is often negligible, so there's little downside to choosing a shorter period.

- It increases the chances your family receives the payout, even in severe health emergencies.

- Read policy terms carefully: some riders may come with more extended periods by default, or differ across insurers.

Ditto's take: When in doubt, always opt for the shortest survival period offered. It's a smart way to protect your claim eligibility.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or chat on WhatsApp with us now!

Conclusion

Understanding the survival period is essential when adding a critical illness rider to your insurance. It can significantly impact your claim and financial protection. Here's some final thoughts:

- The survival period applies to riders, and regular health insurance does not cover treatment costs.

- Typically, you must survive 14 to 30 days after diagnosis or injury for a claim to be valid.

- Choosing a shorter survival period reduces the risk of claim denial and improves payout chances.

- If you don’t survive the period, no lump sum is paid, and premiums are usually non-refundable.

- Always check the survival period terms carefully before finalizing your policy.

Frequently Asked Questions

Last updated on: