Quick Overview

Reliance Nippon Life Insurance Company Limited was originally launched as AMP Sanmar Life Insurance in 2001. It later became Reliance Life Insurance and subsequently Reliance Nippon Life Insurance Company Limited after Nippon Life of Japan increased its stake.

It has officially been renamed IndusInd Nippon Life Insurance Company Limited, effective 10 December 2025. This is only a name change. All existing policy benefits, terms, conditions, and servicing remain unchanged.

The insurer has also updated its official email domain from @relianceada.com to @indusindnipponlife.com. Policyholders can reach customer service at customerservice@indusindnipponlife.com for assistance.

Reliance Nippon Life Insurance Performance Metrics

Note: Reliance Nippon Life Insurance handles claims reliably and maintains stable finances. Customers report relatively fewer service issues, and overall, the company appears steady and dependable, even though it is not among the largest insurers in the market.

However, its annual business volume is substantially lower than the industry median. While that does not imply weakness, it indicates a smaller market share than that of leading insurers. For long-term contracts like term insurance, scale and sustained growth can influence operational resilience over decades.

Top Plans Offered by Reliance Nippon Life Insurance

1) Reliance Nippon Life Super Suraksha Plus

Super Suraksha Plus is the insurer’s flagship term plan, available in two variants: Life and Life Plus.

- Offers pure protection under the Life variant and return-of-premium option under Life Plus.

- Entry age starts at 18 years, with coverage extending up to 85 years (variant-dependent).

- Minimum sum assured starts at ₹50 lakh, with no upper cap (subject to underwriting).

- Flexible premium payment options, including regular and limited pay.

- Enhanced Coverage Benefit allows policyholders to increase coverage at key life milestones like marriage or childbirth without fresh medical underwriting.

- Customizable payout options (lump sum, income, or combination).

- Optional riders for accidental death, disability, and critical illness.

- Discounts are available for salaried individuals, women, and online buyers.

This plan suits individuals looking for flexible structure, milestone-based coverage upgrades, and optional maturity benefits.

2) Reliance Nippon Life Super Suraksha Elite

Super Suraksha Elite is a high-cover term plan tailored for affluent individuals seeking substantial protection.

- Minimum sum assured starts at ₹2 crore.

- Entry age ranges from 18 to 60 years.

- No maturity benefit (pure protection plan).

- Policy terms can extend up to 50 years, subject to age limits.

- Offers the same rider options and discount structure as Super Suraksha Plus.

- Enhanced Coverage Benefit is available.

- Provides a conditional instant claim payout feature.

- Requires a minimum income threshold and is targeted at salaried and self-employed professionals.

This plan competes directly with high-sum assured plans from large private insurers. Pricing is competitive but not consistently the lowest in the market.

3) Reliance Nippon Life Saral Jeevan Bima

Saral Jeevan Bima is a standard term insurance product mandated by the regulator and offered by all insurers under uniform guidelines.

- Coverage ranges from ₹5 lakh to ₹25 lakh.

- Entry age ranges from 18 to 65 years.

- Offers regular, limited, or single premium payment options.

- Designed for individuals who may face difficulty meeting strict income or documentation requirements.

It is a basic, no-frills term plan suitable for individuals seeking simple and affordable life cover.

Types of Plans Offered by Reliance Nippon Life Insurance

- Term Plans: Super Suraksha Plus, Protection Plus, Digi-Term Insurance Plan, Saral Jeevan Bima.

- Savings & Endowment Plans: Guaranteed Advantage Income Plan, Nishchit Samrudhi Plus, Super Endowment Plan, Increasing Income Insurance Plan, Bluechip Savings Plan.

- ULIPs (Unit Linked Insurance Plans): Prosperity Plus, Classic Plan II, Smart Savings Insurance Plan, and Premier Wealth Insurance Plan.

- Retirement & Pension Plans: Saral Pension Plan, Immediate Annuity Plan, Smart Pension Plan, Nishchit Pension.

- Child Plans: Education Plan, Child Plan.

- Group Plans: Group Term Assurance Plus, Group Credit Protection Plus.

Premiums for Reliance Nippon Life Super Suraksha Elite Plan vs. Other Insurers

Note: For this example, we’ve taken healthy profiles of non-smoking, salaried individuals, covered for a sum assured of ₹2 Crores till the age of 70. The premiums are indicative in nature and can vary based on your age, health condition, lifestyle choices, and underwriting decisions. Moreover, the figures exclude first-year discounts (2nd year onwards premiums).

A 10% online discount and 5% salaried discount have been applied to the first-year premium for Reliance Nippon Life.

Riders Available in Reliance Nippon Life Insurance Plans

Note: The Accidental Death and Disability Plus rider may not be available if the Enhanced Coverage Benefit option is chosen.

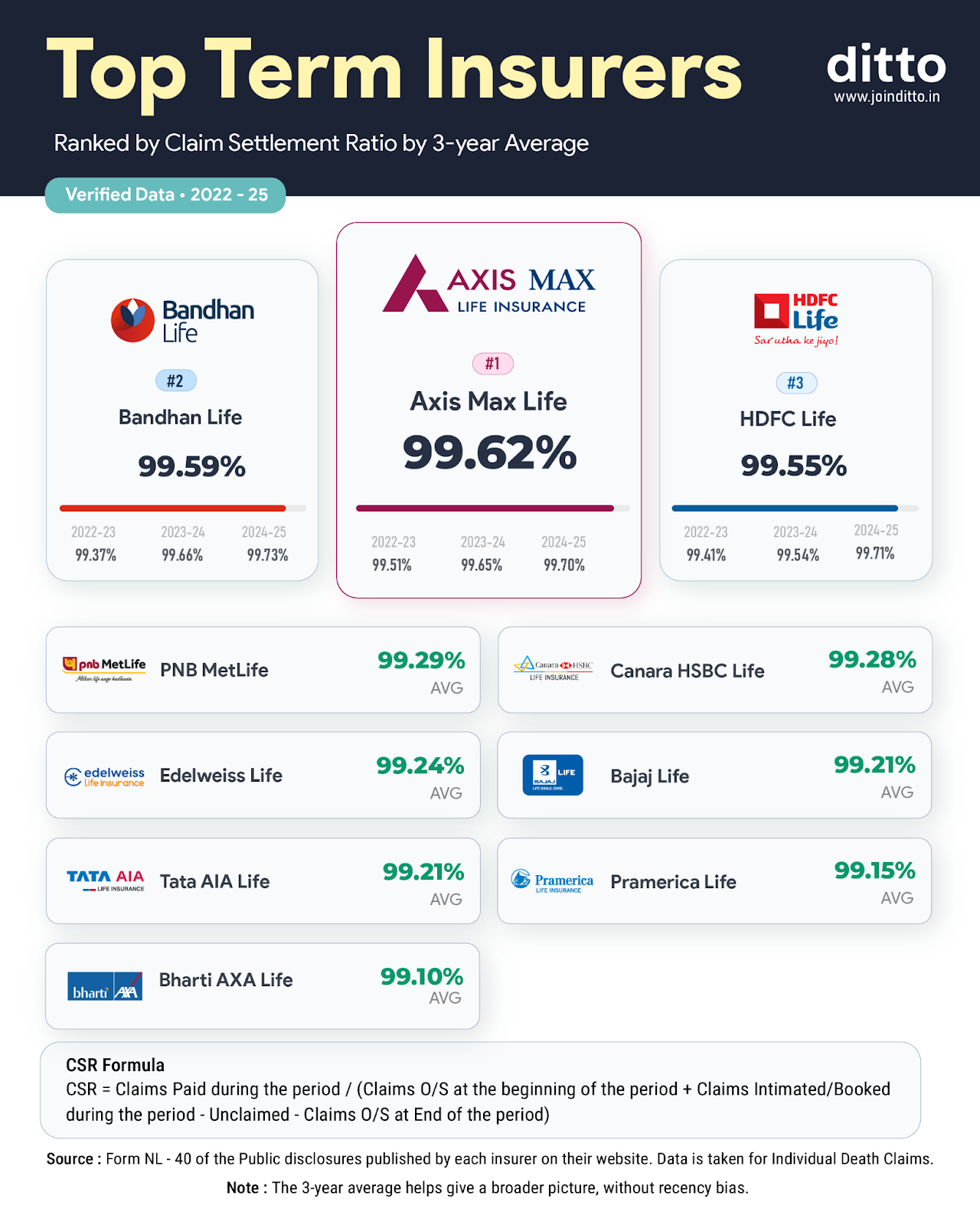

Top 10 Life Insurance Companies in India by Claim Settlement Ratio

Note: The CSR reflects the overall claim settlement performance of the life insurance company across all products, not just the term insurance segment. However, it should not be the sole deciding factor. You should also evaluate ASR, solvency ratio, product structure, and long-term financial stability before making a decision.

Why Choose Ditto for Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat on WhatsApp with our expert IRDAI-certified advisors.

Ditto's Take

Reliance Nippon Life Insurance has undergone ownership transitions in recent years and is now operating under new management. While such transitions can create uncertainty, the insurer’s claims performance and servicing track record have remained broadly stable so far.

Its term plans, Super Suraksha Plus, Super Suraksha Elite, and Saral Jeevan Bima, offer decent flexibility, milestone-based cover enhancements, and optional riders. For buyers in Tier 2 and Tier 3 cities, its strong distribution network can also be a practical advantage.

That said, life insurance is a long-term commitment. When an insurer undergoes structural or ownership changes, it’s reasonable to monitor consistency in service standards, underwriting approach, and product continuity over time.

Disclaimer: Reliance Nippon Life Insurance is not a partner insurer of Ditto. Our assessment here is completely independent and based solely on publicly available data and the evaluation framework we use for all insurers.

If you want to understand how Ditto reviews insurers across claims, complaints, business strength, and product suitability, read our methodology here. Please check the insurer’s official website for the latest available information.

Frequently Asked Questions

Last updated on: