Overview

Introduction

When you’re reeling from the loss of a loved one, paperwork is the last thing you want to deal with. Yet, during such emotionally overwhelming moments, term insurance becomes a crucial financial lifeline for the family.

Having handled thousands of claims at Ditto, we understand that life insurance is a sensitive space, and navigating claims can feel confusing, intimidating, and even frustrating when you don’t know where to begin. That’s why we’ve put together this simple, no-nonsense guide that walks you through the step-by-step process of term insurance claim settlement, the documents required for term insurance claim submission, key factors to consider, and practical tips to ensure a smooth experience.

Step-by-Step Process of Term Insurance Claim Settlement

The following nifty little infographic details the step-by-step process of term insurance claim settlement:

If your term insurance claim was rejected and you want to know why, refer to the linked blog for the possible reasons.

Documents Required for Term Insurance Claim

For term insurance claim submission, the required documents depend on the cause of death.

Natural Death (Illness, Old Age, Medical Conditions)

- Claim form

- Death certificate

- Nominee’s KYC (ID + address proof)

- PAN or Form 60

- Bank details (cancelled cheque/passbook)

- Medical cause of death certificate (if available)

Accidental or Suspicious Death (Accident, Suicide, Homicide)

- Death certificate

- FIR

- Post-mortem report (PMR)

- Inquest/panchnama

- Police final report/charge sheet

- Nominee’s KYC

- Additional documents, if needed: viscera report, driving licence, eyewitness statements, newspaper clippings

Death Due to Natural Disasters

- Death certificate from the government/disaster authorities

- Claim form with bank details

- Nominee’s KYC

- PAN or Form 60

- Local authority certificate/eyewitness statements (if the body is not recovered)

Death Outside India

- Embassy/consulate–attested death certificate

- Local police report (or equivalent FIR)

- Certified English translations of documents

- A passport copy of the deceased

- Proof of cremation or repatriation (if available)

Disputed Cases / Special Scenarios

- Standard claim documents (depending on the type of death)

- Attested Will, Legal Heir Certificate, or Succession Certificate

- Additional investigation reports, if required

For a complete case-by-case list, read this blog on documents required for term insurance claim submission.

A denied term insurance claim can feel overwhelming, especially when you’re already dealing with loss. But a rejection isn’t always final; there are clear steps you can take to get the claim reviewed again.

What To Do When Your Term Insurance Claim is Rejected

Ask for a Written Explanation

Start by requesting an official written note from the insurer explaining why the claim was rejected. This helps you understand the exact issue and is essential if you plan to contest the decision.

Review, Correct, and Resubmit Documents

Many claims are denied due to missing or mismatched documents. If that’s the case, you can provide the required paperwork or clarifications and ask the insurer to reassess the claim.

Reach Out to the Insurer’s Grievance Redressal Officer

If the initial rejection letter doesn’t resolve your concerns, escalate the matter within the insurer by contacting their Grievance Redressal Officer (GRO). The insurer must respond within a defined timeframe, usually 15 days.

Escalate via Bima Bharosa (IRDAI’s Grievance Portal)

If the insurer’s response is unsatisfactory, you can escalate the issue through IRDAI’s grievance redressal platform, Bima Bharosa. It allows you to register complaints, upload evidence, and track your case until it is resolved.

Approach the Insurance Ombudsman

If the matter still isn’t resolved, you can file a complaint with the Insurance Ombudsman, who independently reviews disputes between insurers and policyholders. Lastly, you can approach Consumer Courts if nothing else has helped.

Things to Keep in Mind Before Making a Term Insurance Claim

- Premiums must have been paid on time, and the policy should be “in force” on the date of death.

- Only the registered nominee (or legal heir) can file the claim. If the nominee's details are outdated, the insurer may request additional legal documents.

- Natural death, accidental death, homicide, or death due to illness, each may require different sets of documents and levels of verification.

- The smoother your documentation, the faster your claim gets processed. Missing paperwork is the primary reason for delays.

Note: While insurers don’t explicitly penalise delays, late intimation often leads to deeper investigations and longer timelines. Therefore, it’s best to file a claim within 90 days of the policyholder’s demise.

Real-Life Claim Scenario

A few months after buying a ₹5 crore term plan, one of our customers tragically passed away in Thailand during a snorkelling accident. His wife, alone in a foreign country, was overwhelmed by the paperwork like hospital documents, local authorities, and consulate procedures.

She contacted us immediately. We guided her on exactly which documents to collect and how to authenticate them. Once she arranged everything, we took over.

Our team coordinated with the insurer, submitted all paperwork, and kept her updated throughout.

After verification, the insurer settled the claim, giving the family the financial security he had planned for them.

Even in the most difficult moments, having the right support can make all the difference. At Ditto, we make sure no family has to navigate this alone.

Why Choose Ditto for Your Term Insurance?

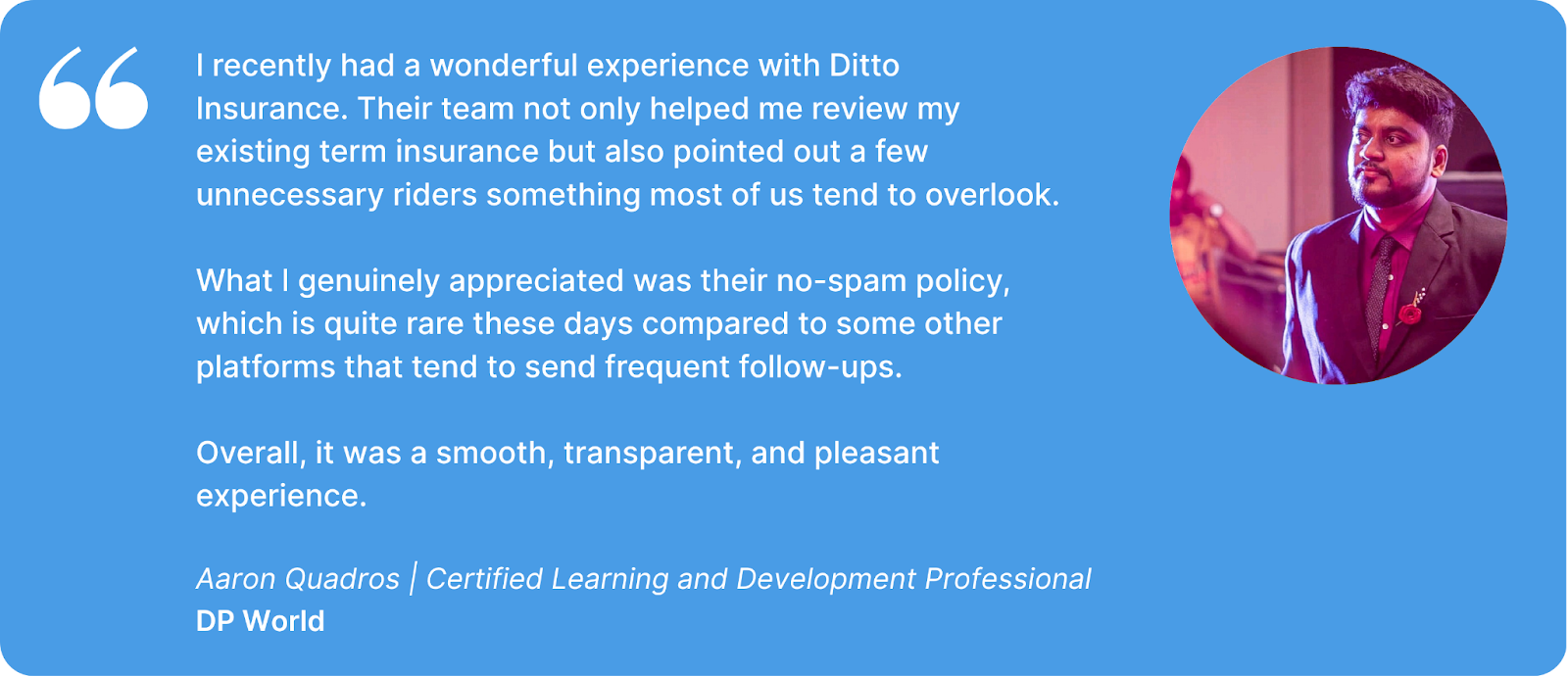

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron love us:

- No Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now!

Conclusion

In moments of loss, even simple tasks can feel overwhelming. But knowing how to claim term insurance can ease a small part of that burden and ensure your family receives the support they’re entitled to. And if you ever feel stuck, remember, you don’t have to navigate this alone. Ditto is always here to help.

Frequently Asked Questions

Last updated on: