What is the National Insurance Premium Rate Chart?

Ever noticed how your health insurance premiums differ from someone else’s, even for the same policy? That’s because several key factors, like age group, city of residence, and riders play a significant role in determining your final policy premium. These elements help insurers assess risk more accurately and price policies fairly. At Ditto, we help customers understand these differences and help them make informed choices for the best coverage.

This guide helps you understand:

- how the National Insurance Company calculates premiums.

- Covers age bands, sum insured slabs, and zonal classifications.

- Simplifies complex terms for easy understanding.

Let’s take a look at some key Public Sector Undertaking (PSU) insurance companies in India:

Check out this video to know more about public health plans in India 2025:

National Insurance Premium Rate Chart: Age Bands & Sum Insured Slabs

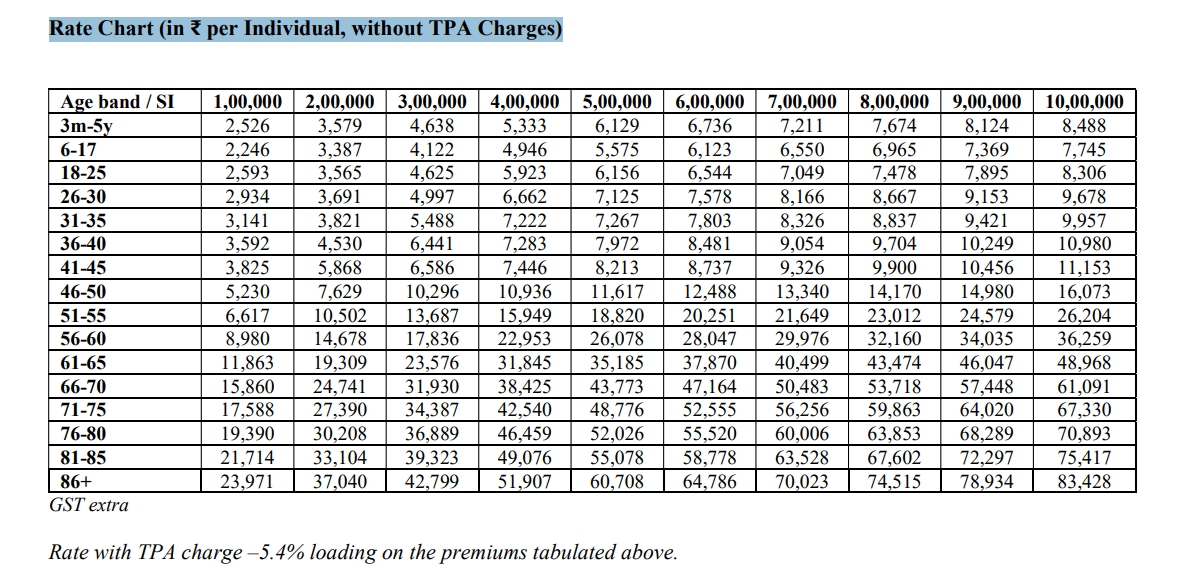

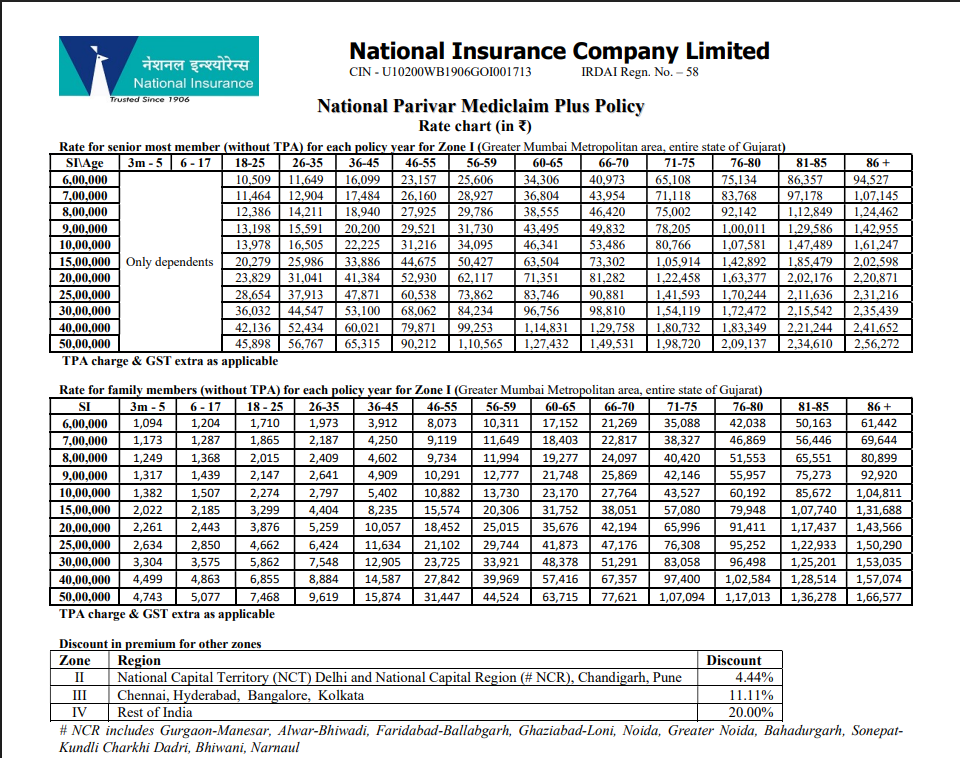

Here’s a snippet from National Mediclaim policy where you can find the Rate chart:

Age Bands and Sum Insured Slabs provide standardized categories for risk assessment and premium calculation. Age bands group policyholders by age ranges, while sum insured slabs define coverage levels.

Such classifications are required because age affects health risk, life expectancy, and the likelihood of claims, while the sum insured indicates potential payout exposure.

Here’s a snippet from National Insurance’s National mediclaim policy:

Are premium charts mandatory?

How do Premium Prices differ by City or Zone?

In India, health insurers use zonal classifications to price premiums more accurately based on medical costs, lifestyle risks, and healthcare infrastructure in different regions. It's a common practice to ensure that residents or those from non-metro/tier 2/3 cities are not penalized for higher treatment costs in tier 1.

For instance, if a 25-year-old male purchases an HDFC Optima Secure plan with a sum insured of Rs 10 lakh, he needs to pay an annual premium of Rs 13,300 if he resides in Delhi, while he needs to pay Rs 11,210 if he resides in Patna.

Here's an overview of how zonal classification works:

- Zone I (Metro Cities): This zone includes cities such as Mumbai, Delhi, Chennai, Bengaluru, Hyderabad, and Kolkata. Medical and hospitalization costs are highest in these areas, resulting in higher premiums.

- Zone II (Tier 2 Cities): Covers state capitals and large cities such as Pune, Ahmedabad, Jaipur, Lucknow, and Kochi. Healthcare costs are moderate in these areas, which means the premiums are slightly lower.

- Zone III (Rest of India / Tier 3 & Rural Areas): This zone includes smaller towns and rural regions, where treatment costs are comparatively lower, resulting in more affordable premiums.

National Insurance offers zonal classification for some of its health products depending on the following zones:

Insurers often apply a zonal copayment when you receive treatment in a higher zone than the one for which your premium is priced.

For instance, the National Parivar Mediclaim Plus Policy has the following conditions:

- Zone I Premium: No copay in other Zones

- Zone II Premium: No copay in Zones II–IV; 5% copay in Zone I.

- Zone III Premium: No copay in Zones III–IV; 7.5% in Zone II, 12.5% in Zone I.

- Zone IV Premium: No copay in Zone IV; 10% in Zone III, 17.5% in Zone II, 22.5% in Zone I.

How to Calculate Your Premium ?

Calculating your health insurance premium with National Insurance Company Limited (NICL) is simple once you know the key factors involved. Here’s how it works:

1) Step 1: Know Your Age Band

Premiums under the National Mediclaim Policy are grouped by age bands — such as 18–25, 26–35, 36–45, and so on.

The older you are, the higher the premium, since health risks rise with age. We recommend our customers to buy a healthy plan when they are young and healthy. Starting early helps you complete waiting periods sooner, benefiting your long-term coverage.

2) Step 2: Choose the Sum Insured

Decide the total coverage amount you need (for example, ₹2 lakh, ₹5 lakh, or ₹10 lakh).

A higher sum insured offers better protection but comes with a slightly higher premium (increase is not linear)

3) Step 3: Check Your Zone

Premiums also vary based on where you live. NICL classifies India into zones to reflect medical costs:

- Zone 1: Metro cities – higher premiums

- Zone 2 & 3: Tier-II and Tier-III cities – moderate or lower premiums

Note: At Ditto, we recommend checking for zonal restrictions, such as copays. If your budget allows, consider choosing Zone 1/Tier-1 premiums, even if you live in lower zones, to ensure coverage for treatments in major cities or specialized hospitals without incurring extra costs.

4) Step 4: Add Optional Covers

You can enhance your base policy with add-ons like critical illness, maternity benefit, or daily cash allowance.

Each add-on increases your total premium slightly but expands coverage.

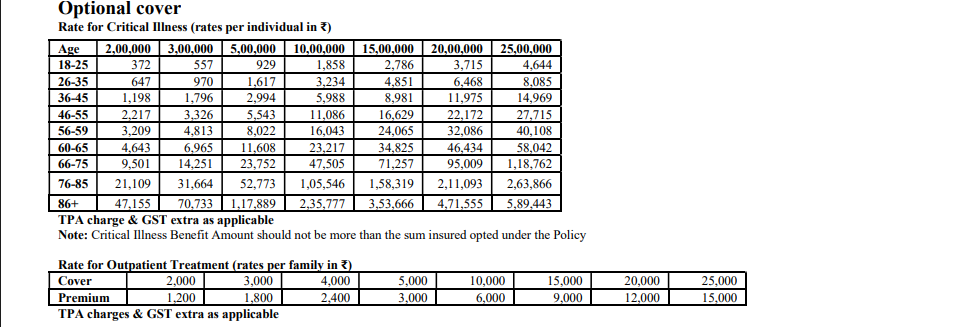

Here’s a snippet from National Parivar Mediclaim Plus Policy about optional covers:

5) Step 5: Apply available discounts

NICL offers discounts for:

- Family floater policies

- co-payment facilities

- No-Claim Bonus (NCB) for claim-free years

For instance, most NICL health products, such as the National Mediclaim Policy and the National Senior Citizen Mediclaim Policy, offer a 10% Online discount (without intermediary) during purchase.

Quick Note:

How are premiums for family floater plans calculated?

Let's take the example of National Parivar Mediclaim Plus Policy (Floater Policy):

Under this policy, the total family floater premium is calculated by adding the premium of the oldest insured member to the combined premiums of all other covered family members.

Each figure is drawn from the corresponding Sum Insured (SI) and age band in the two tables from the above extract.

Example (illustrative for Zone I, ₹10 lakh SI):

- Base premium = 31,216 + 5,402 + 1,507 + 1,507 = ₹ 39,632

- Add 5.4 % TPA loading = ₹ 39,632 +₹ 2,140 = ₹ 41,772

Note: TPA loading is the additional charge on the total premium when the policy is serviced through a Third-Party Administrator, covering the administrative cost of cashless and claims support.

Why Talk to Ditto for Your Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Abhinav below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now!

Conclusion

Knowing how age, coverage, and location affect your health insurance premium helps you make smarter decisions while purchasing a health plan. Here's what to keep in mind:

- Premiums increase with age as health risks rise. They may also increase when insurers revise rates or adjust for inflation, resulting in updated premium charts.

- Sum insured slabs define coverage levels and potential payouts, enabling insurers to assess risk and determine appropriate premiums accurately.

- Premiums differ by city or zone based on healthcare costs, lifestyle, and infrastructure.

- Loading charges are applied on top of the premiums; most policies also specify the maximum possible loading for any one condition and the policy overall.

- Consider your age band, chosen sum insured, residential zone, optional add-ons, and discounts such as multi-year plans, family floater policies, or No-Claim Bonus.

Frequently Asked Questions

Last updated on: