Imagine paying rent, EMIs, and school fees, and then a parent or child needs an unplanned surgery. The bill does not check if you are financially ready.

This fear is very real because most healthcare expenses in India are still paid directly by families. In 2021–22, out-of-pocket spending was 39.4% of India’s total health expenditure (down from 62.6% in 2014–15, but still a major share).

That is why buying health insurance for family is important. It involves choosing a plan that actually protects your household from sudden, high medical bills, especially in years when more than one person needs care.

In this guide, we will break down the top 5 health insurance plans for family in India, their benefits and drawbacks, and learn how to shortlist the right policy.

Key Features of a Health Insurance Plan for Family

Shared Family Cover

A family floater typically covers self, spouse, and dependent children under one policy, with a single sum insured shared by everyone. In simple terms, this means that if one member uses a part of the cover, the remaining cover is what the rest of the family is left with for that policy year.

Cashless Claims

Cashless reduces the need to arrange the full hospital bill amount upfront. The insurer pays the hospital directly (after approvals) for admissible expenses. A practical way to judge cashless usefulness is the insurer’s network in your city and how smoothly pre-authorization gets handled. IRDAI also sets expectations on timelines, including quick decisions on cashless authorization and timely discharge approvals, which is exactly what families care about during emergencies.

Pre- and Post-Hospitalization Cover

A good family plan covers not just the hospital stay but also related expenses before admission and after discharge, within defined day limits. This is what protects you from paying separately for tests, medicines, and follow-up care that are part of the same treatment episode. The exact number of days varies by plan, so it is worth checking this feature while shortlisting.

Room Eligibility

Room eligibility influences how much the insurer pays during a hospitalization. If your plan has room rent limits, choosing a higher room category can reduce the payout through proportionate deductions, not just the room cost difference. Plans with no room rent limits are preferred as they tend to create fewer unpleasant surprises for families during claims.

Restoration Benefit

Restoration is a feature that can refill the sum insured within the same policy year, based on the plan’s rules. This matters more in a family floater because multiple claims in one year can happen, and everyone is using the same shared pool. A good restoration benefit allows each member to effectively have their own cover. Always check the trigger conditions, like whether the refill happens only after full exhaustion and whether it has restrictions around related illnesses.

Maternity and Newborn Cover

Some family plans offer maternity and newborn-related benefits. They often come with waiting periods and payout caps. Look for this feature if you are planning a baby and want coverage for delivery-related hospitalization costs and early newborn care that the normal plans exclude for the first 90 days. If you have a corporate cover, prefer that over buying a maternity plan. Check the cost-to-benefit ratio because usually you end up paying more than the benefits.

Individual vs. Family Floater Health Insurance Plans: Which is Better?

Default Choice

For most families, buying a shared cover for your immediate family, including your spouse and your kid is recommended. It is built for households with similar age profiles and lets everyone share one pool of cover. This works out more efficiently and costs up to 50% less than buying separate individual policies for each member.

Parents in Floaters?

Adding parents to the same floater is usually not a good idea for two reasons.

- If your parents are in the same family floater policy, their age drives the pricing, and the premiums increase, even if you and your spouse are still young.

- Parents are more likely to claim. Since a floater has a shared sum insured, frequent or large claims can drain the pool and make the policy less useful for your spouse and kids in the same year.

What we recommend instead is a cleaner split: one floater for you, your spouse, and kids, and a separate floater policy for parents. This keeps the covers separate, prevents parents’ age from inflating your family's premium unnecessarily, and makes the policies easier to manage and optimize for each group’s needs.

When an Individual Plan Wins

Individual plans make more sense when one member has a significant or complicated medical history. It can also help when a combined family floater option is not feasible due to underwriting or eligibility constraints.

How to Choose the Best Health Insurance Plan for Families in India?

When you compare family plans online, most pages look the same: big “cashless” banners, “comprehensive” badges, and a premium that looks tempting. The problem is, none of that tells you what really matters for a family: will this plan pay cleanly, without surprise deductions, when multiple things go wrong in the same year?

At Ditto, we rate plans using a structured framework that lets you compare policies on the things that actually affect claims, not marketing. We look at three buckets:

Policy Strength (Features)

This is where most families get burned. We check room rent rules, co-pays, waiting periods (and whether you can reduce them), restoration rules, no-claim bonus behavior, consumables, and exclusions that can cause out-of-pocket costs during a claim.

Company Dependability (Insurer)

Even a well-designed plan feels painful if service is poor. We look at the insurer's track record using IRDAI-backed data points and signals like complaint volume, business scale, and hospital network strength, so you can judge how reliable the company is when you actually need a cashless approval or a reimbursement payout.

Value for Money (Premium)

Finally, we sanity-check the premium for a benchmark family setup and ask a simple question: Are you paying extra for real claim protection, or just for fancy-looking add-ons?

These scores combine into a single policy rating that we standardize into a Ditto Policy Score, so it is easier to shortlist without getting lost in spreadsheets. If you want the full breakdown of how the scoring works and how we evaluate plans or insurers, you can read Ditto’s cut.

Using this approach, here are the Top 5 Health Insurance Plans for Family in India.

Top 5 Health Insurance Plans for Family

Talk to an expert

today and

find

the right

insurance for you.

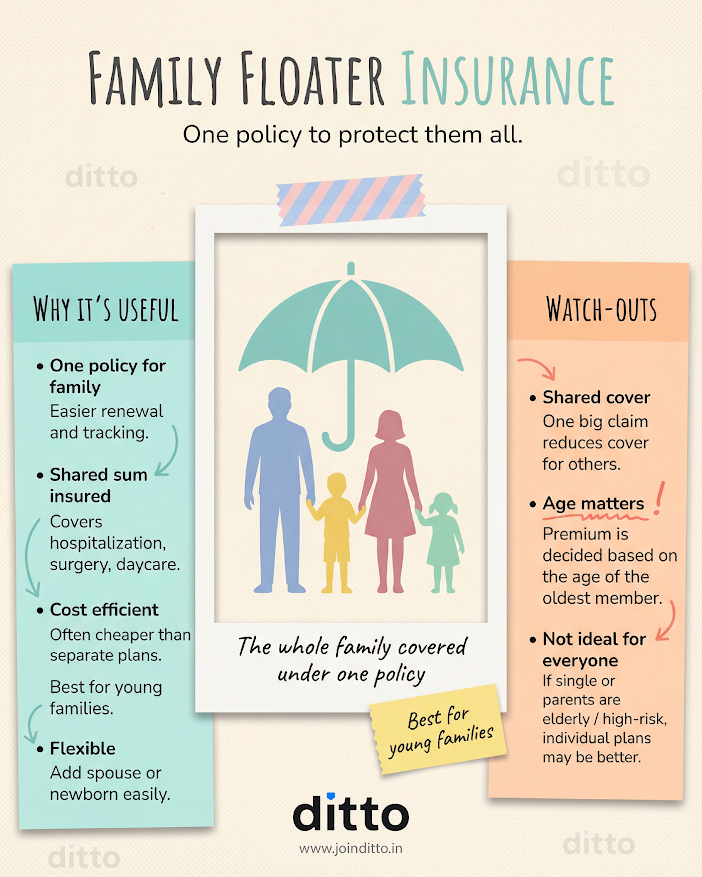

Benefits of Buying Family Health Insurance

Check out the infographic below to learn how family floater insurance works well for many families, and the key considerations you should know upfront.

Premiums for Health Insurance Plans for Family

Note: These are indicative premiums for a Delhi resident (Pincode - 110001), with a ₹15 lakh sum insured, including mandatory and recommended add-ons. Your premiums can change based on age, city, medical history, plan variant, and chosen add-ons.

Drawbacks of Family Health Insurance

Shared Cover Drain

Restoration Confusion

Claim Deduction Traps

Eldest Age Pricing

Inclusions and Exclusions of Health Insurance Plans For Family

It’s worth noting that coverage and exclusions may vary slightly across insurers and plans.

Things to Keep in Mind Before Buying a Family Plan

Full Health Disclosure

Disclose every past medical condition, surgery, and any ongoing treatment upfront, even if it feels minor. We have seen many claim disputes start from “small omissions” that later get treated as misrepresentation, especially before the 5 year moratorium protection fully kicks in.

Dependent Age Rules

Check who counts as a dependent and till what age, because plans differ on child entry age and when a child stops being eligible under a floater. Many retail plans allow kids to be added from 91 days and keep them covered as dependents until their early to mid 20s, but you should confirm it for your plan. Once kids reach the exit age, insurers offer an option to migrate into an individual plan offering similar benefits and coverage.

Newborn Coverage Timing

If your plan does not include newborn coverage, the baby usually gets added to the family floater after 91 days, subject to insurer rules. This matters if you are planning a baby and want the first few months covered, because you may need a plan that explicitly offers newborn benefits.

Policy Document Audit

Before you commit long-term, do a quick audit of the policy document basics: insured member details, sum insured, exclusions, and key clauses that affect claims. Compare your policy against our checklist that helps you review this without getting overwhelmed.

How to Buy a Health Insurance Plan for Family Online?

Step 1: List Members

Start by listing who needs to be covered: you, spouse, kids, and whether parents will be separate. Note ages, city, and any existing medical conditions, since these affect eligibility, waiting periods, and pricing.

Step 2: Decide Plan Structure

Choose the structure first: a family floater usually fits self, spouse, and kids, while parents are typically better on a separate policy. Getting this right upfront makes shortlisting faster and avoids paying for the wrong setup later.

Step 3: Set Your Sum Insured

Pick a base sum insured that can handle at least one serious hospitalization without exhausting the policy. We recommend opting for a ₹15-25 lakh base cover, considering medical inflation and hospital costs.

Step 4: Shortlist Insurers

Now, shortlist insurers based on practical reliability signals and hospital network strength in your city. Check out the best health insurance companies based on Ditto’s framework.

Step 5: Shortlist Plans

Within your insurer shortlist, compare plans on claim-impact features, not brochure language. Check out our understand your policy tool to read about any policy in detail.

Step 6: Fill Details Carefully

When you apply online, enter your member details exactly as per government ID proofs and disclose your medical history completely. Most claim issues start from incorrect information or missed disclosures, so treat this step like a formality that protects your future claim.

Step 7: Upload Documents

Keep standard documents ready: identity proof, address proof, age proof, and any medical records if asked. This reduces delays in underwriting and issuance.

Step 8: Medical Tests (If Required)

Some members may be asked for tests based on age or health disclosures. This is normal underwriting, and it is better to complete it quickly so your policy gets issued without delays.

Step 9: Issuance and Follow-Ups

After you submit the application, the insurer may come back with follow-up questions or ask for additional documents, especially if any member has a medical history or if medical tests are required. This back-and-forth is normal underwriting, and your policy gets issued only after the insurer is satisfied with the information and reports.

Why Talk To Ditto For Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Abhinav below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation here. Slots are filling up quickly, so be sure to book a call or chat on WhatsApp with us.

Ditto’s Take on Family Health Insurance

If you are buying health insurance for your family, our stand is clear: get one strong floater for you, your spouse, and your kids, and keep parents on a separate policy in most cases. This structure stays the most predictable on premiums and also keeps your family’s cover from being consumed by higher-frequency claims.

What We Recommend:

- Prefer “clean” plans that do not create surprise costs at claim time (avoid heavy room rent limits and routine co-pays where possible).

- Use restoration as backup, not as your main dependency feature. It helps in multi-claim years, but base cover still matters most.

- If one member has a complicated medical history, consider a separate individual policy so everyone else’s cover stays stable.

Bottom Line: A good family policy is one you can renew for years without regret. Ensure the structure is simple, keep parents separate, and buy for claim reliability, not just a low premium.

Quick Note

Frequently Asked Questions

Customer Reviews

Last updated on: