Quick Overview

If you’ve explored life insurance in India, you’ve almost certainly come across LIC. Founded in 1956, LIC has built a dominant presence over the decades and continues to command a large share of the life insurance market. The insurer handles an annual business of over ₹2,17,726 crore, maintains a claim settlement ratio of 98.55%, and settles about 95.90% of claims within 30 days, figures that reinforce its scale and longstanding trust among policyholders.

Given this strong market position, many buyers naturally consider LIC first when evaluating term insurance. However, term insurance pricing with LIC can vary significantly depending on your profile and the plan selected.

This is where the LIC Term Plan Calculator becomes useful. It allows you to preview premiums before committing to a policy. By using the lic term plan premium calculator approach available through LIC’s website, you can understand whether the pricing aligns with your financial goals or if alternatives offer better value.

In this article, we explain how the calculator for LIC Term Insurance Plans works, what affects premiums, and how LIC compares with private insurers.

LIC Term Plan Calculator: Online Steps

- Visit the LIC homepage and click on “Buy Online” in the top-right corner.

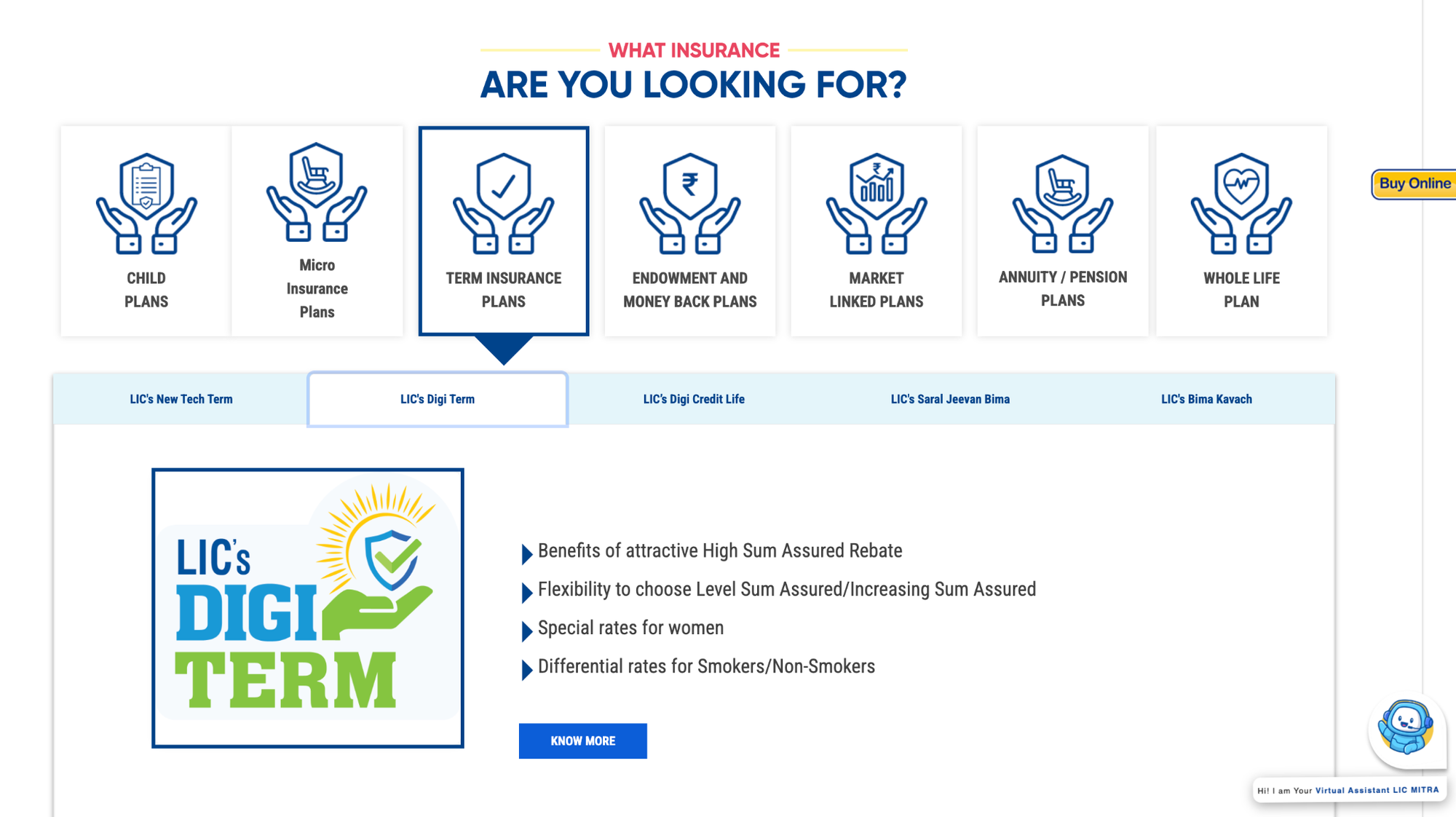

- Scroll down and select “Term Insurance Plans.”

- Choose the specific term plan for which you want to estimate the premium.

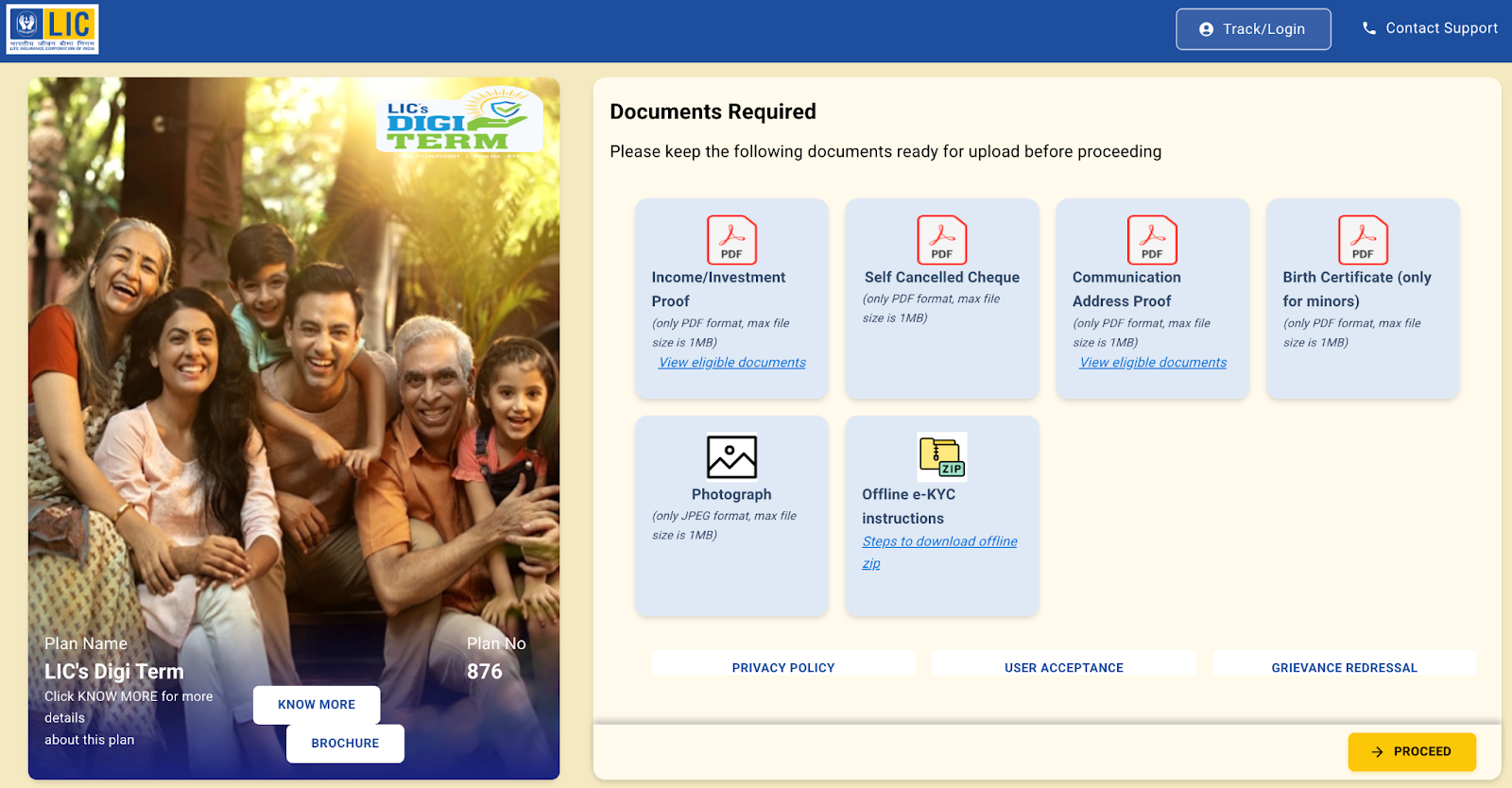

- Click “Know More.” You’ll be redirected to an external page. This is part of LIC’s official flow and is required to proceed.

- On the next screen, click “Proceed.”

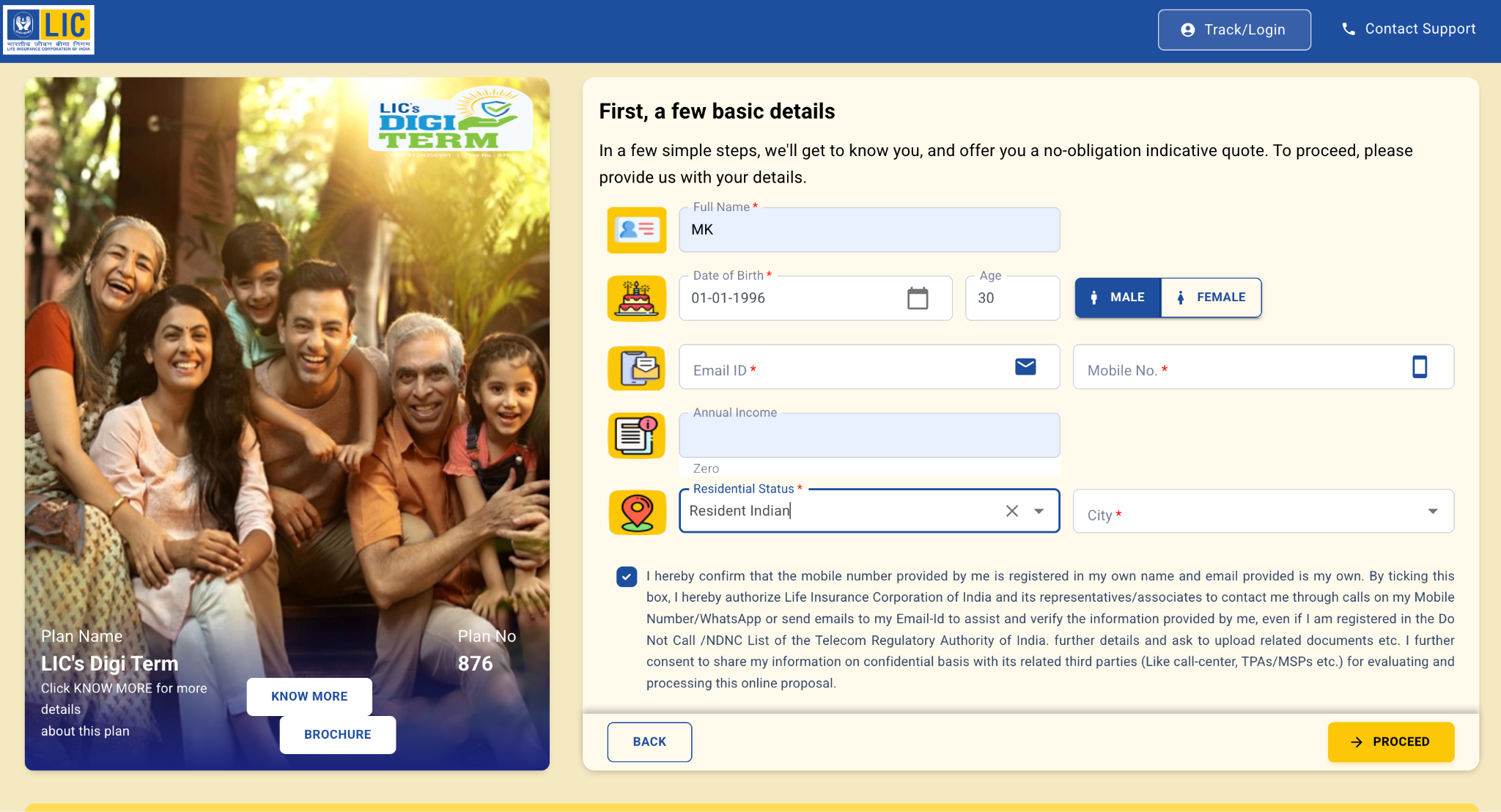

- Enter the required personal details asked such as age, income, residential status, and contact details, then click “Proceed.”

Note: Using your actual contact details may lead to follow-up calls or emails from LIC representatives.

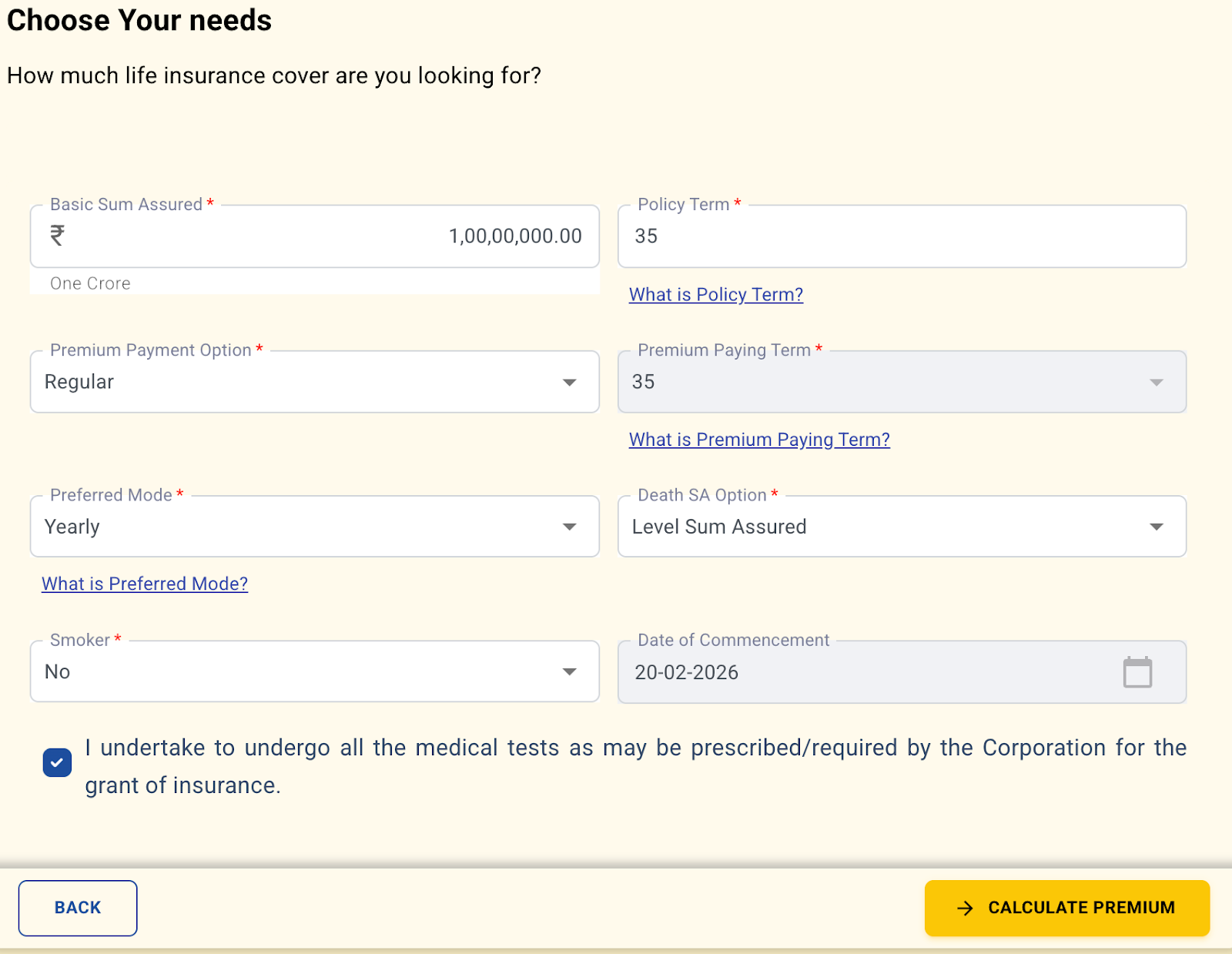

- Fill in the required information like sum assured, policy term, and payment option, etc., then click “Calculate Premium.” The amount displayed is an indicative premium generated through this LIC Term Plan Calculator-style process.

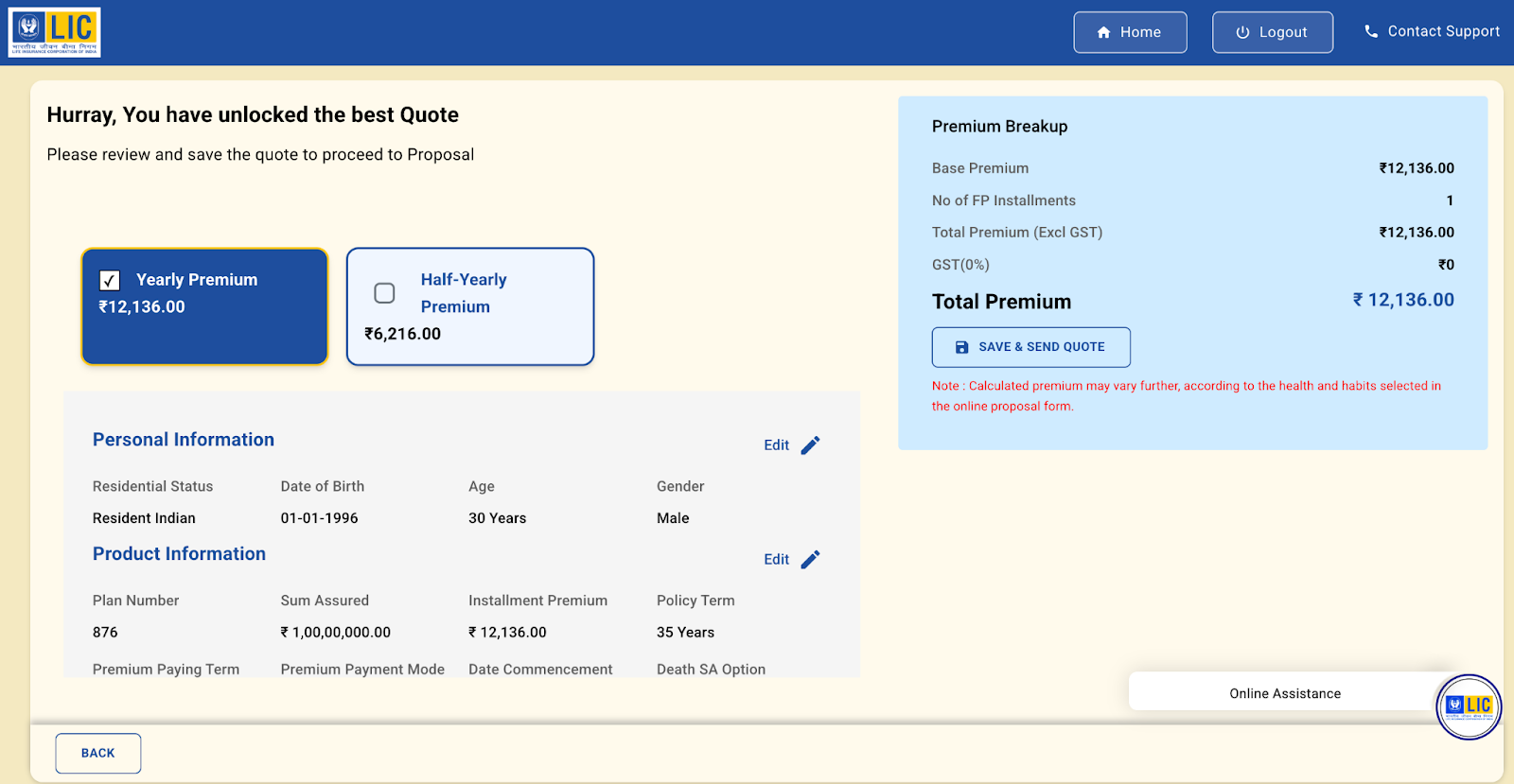

- You have successfully understood and unlocked the LIC Term Plan Calculator.

Note: The displayed premium is for LIC’s Digi Term Plan for a 30-year-old male non-smoker with a 1 crore cover until the age of 65.

The LIC Term Plan Calculator is usually the Buy Online quote journey, not a single standalone tool. If you prefer not to navigate the website to find the premiums, you can call the official LIC number at +91-22-68276827 for assistance from agents.

Top LIC Term Insurance Plans

1) LIC Digi Term (Plan No. 876)

LIC Digi Term is a pure term insurance plan and one of the more affordable protection-focused options from LIC. While it provides essential life cover, the plan does not include modern features such as early exit benefits, life stage upgrades, or multiple rider options.

2) LIC Bima Kavach (Plan No. 887)

LIC Bima Kavach is another pure protection plan offering high coverage. The plan allows an accident benefit rider and a cover enhancement option. However, it lacks commonly available riders like waiver of premium or critical illness cover.

3) LIC New Tech Term (Plan No. 954)

LIC New Tech Term Plan is a non-linked, individual pure-risk plan available exclusively through LIC’s online platform. It offers basic protection with an optional accident benefit rider but does not include newer features such as early exit benefits or life stage flexibility.

Other LIC Term-Oriented Offerings

In addition to the plans above, LIC also offers products such as Yuva Term, New Jeevan Amar, and Yuva Credit Life. These plans are available through the offline purchase route via LIC branches or agents and may not be part of the standard LIC Term Plan Calculator evaluation journey.

Factors Affecting LIC Term Plan Premiums

1. Entry Age: Buying earlier means lower premiums since the risk of a claim is lower.

2. Sum Assured: Higher cover increases premiums, though larger policies may receive High Sum Assured Rebates that reduce the cost per unit of cover.

3. Policy Term: Longer tenures cost more because the insurer carries the risk for a longer period.

4. Smoking & Lifestyle: Tobacco use significantly raises premiums due to higher health risks. Pre-existing illnesses and certain high-risk professions can also lead to higher premiums, as they increase the insurer’s risk exposure.

5. Plan Variant: Level cover is cheaper, while increasing cover may cost more as the sum assured rises over time.

6. Premium Payment Option: Single, limited, or regular pay structures influence overall pricing and affordability.

7. Gender: Women typically pay slightly lower premiums based on life expectancy trends.

Sample Premium Comparison (Illustrative)

Note: The listed premiums are for a non-smoker profile, male with a sum assured of ₹2 crore (Coverage till age 70, without first-year discounts). Premiums are indicative and may vary based on underwriting outcomes, health status, and chosen riders.

LIC vs Private Term Insurance: Which Is the Better Option?

LIC term plans offer unmatched brand legacy and trust, but they often come with higher premiums, limited riders, in-built features, and less flexibility. Private insurers, on the other hand, provide more competitive pricing, comprehensive features/riders, and smoother digital experiences. Comparing quotes using the LIC Term Plan Calculator alongside private plans can help you see which option delivers better value.

LIC plans may be suitable for individuals who prefer simple, no-frills protection, value LIC’s longstanding reputation, and are comfortable choosing a straightforward policy without extensive customization.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat on WhatsApp with our expert IRDAI-certified advisors.

Frequently Asked Questions

Last updated on: