| How Does Term Insurance Claim Work? A term insurance claim is filed by the policy beneficiary to the insurance company to avail of the death benefit in case of the policyholder's unfortunate demise. A majority of insurance companies offer efficient claim processing facilities, allowing beneficiaries to file claims and receive benefit payouts on time. For claims, the nominee must submit the original policy document or a soft copy, death certificate, claimant's ID proof, medical or hospital records (if applicable), and a bank account proof. In case of accidental death, FIR and postmortem reports may also be required. |

Losing a loved one is devastating, and the last thing a family needs is a delayed or rejected insurance claim. Every year, thousands of claims are denied due to missing documents or incorrect disclosures, leaving families financially vulnerable.

To avoid this, you can approach your agent or an intermediary like Ditto to claim term insurance efficiently. Most importantly, you must know how the claim settlement process happens over time.

Drawing from IRDAI regulations, policy wordings, and our claim support experience, this guide simplifies the process for nominees. By the end, you’ll know how does term insurance claim work and what steps to take to ensure a smooth, stress-free claim.

Purchased your term insurance policy via Ditto? Just reach out to us, and our expert claims team will guide you every step of the way. Get claims assistance now!

You can book a FREE consultation. Slots are running out, so make sure you book a call now!

| Key Takeaways: 1) Keep all required documents up to date and ready. 2) Maintain transparency in policy details and disclosures. 3) Regularly update nominee and contact information. 4) A well-prepared nominee ensures faster claim settlement. 5) Many insurers provide grief counsellors and trained claims teams for support. |

Step-by-Step Process of Term Insurance Claim Settlement

Here's the breakdown of the steps to guide nominees and beneficiaries, ensuring a smooth and timely claim settlement process.

- Notify the Insurer Immediately: Inform the insurance company about the policyholder’s death as early as possible. Notification can be done via customer care helpline, email, the insurer’s website, or by visiting the nearest branch office.

- Gather Documents: Prepare and organize all necessary paperwork before submission. Refer to the list of mandatory and additional documents required in the next section.

- Submit the Claim: Once all documents are ready, submit the claim to the insurer or the intermediary. You can submit the claim at a physical branch, via email, or through the insurer’s online claims portal.

Ditto’s Advice: Always keep photocopies of all submitted documents and obtain a written or digital acknowledgment for future reference, or if multiple policies are to be claimed.

- Claim Verification: The insurer will now review the claim and documents to validate the request. Natural deaths generally require basic verification, whereas unnatural deaths like accidental deaths, suicides, or deaths occurring within the contestability period ( first 3 years of the policy) may trigger a detailed investigation.

Ditto’s Note: Be transparent and cooperative. Respond to all insurer queries promptly, and provide complete, honest information. This not only builds trust but also helps minimize delays in claim settlement.

- Claim Settlement: After successful verification, the insurer proceeds with the settlement. If no investigation is required, the death claim must be settled within 15 days from the date of intimation. In cases where an investigation is necessary, the claim must be settled within 45 days from the date of intimation. Ultimately, the approved claim amount is directly credited to the nominee's bank account via NEFT.

| Did You Know? As per IRDAI’s master circular on protection of policyholder’s interests, you can contact the insurer’s grievance redressal cell or escalate to the Insurance Ombudsman in case of delays. If the claim is not settled within the specified timelines, the claimant is entitled to interest at the bank rate plus 2% from the date the insurer receives the claim intimation until the date of payment. This interest must be paid by the insurer automatically along with the claim amount. |

How Does Section 45 Impact the Claim Settlement Process?

According to Section 45 of the Insurance Act, 1938, a life insurance policy cannot be questioned on any ground except outright fraud once 3 years have passed from the latest of:

- Policy issuance

- Commencement of risk

- Revival of policy

- Addition of rider

To learn more about the reasons behind term insurance rejections and the ways to handle them, read this article.

Documents Required for Term Insurance Claim Submission

If you want to avoid term insurance claim rejections, here is a list of documentation you should possess:

1. Basic/Mandatory Documents (For all Claims)

- Duly filled and signed Claimant Statement Form (Claim form)Original Policy document (Not required if policy is in E-insurance account/ Demat form)

- Death Certificate of the Life Assured (issued by Municipal Authority / Gram Panchayat / Tehsildar, attested if a copy)

- Claimant’s identity proof (PAN, Aadhaar, Passport, Voter ID, etc.)

- Claimant’s address proof (Utility bill, Aadhaar, Passport, etc.)

- Recent photograph of the claimant

- Bank account proof (Cancelled cheque/bank statement/bank passbook with printed name and account number)

- Duly filled and signed the payout mandate form with bank details

- Copy of PAN card or Form 60 of the claimant

2. Additional Documents (Based on the Cause of Death)

A. Natural Death (e.g., in hospital, at home, medical causes)

- Medical cause of death certificate (attested by hospital/doctor)

- Past medical records & treatment papers

- Hospitalization records, such as admission forms, indoor case papers (ICPs), discharge summaries, and diagnostic/lab test reports (USG, Pathology, etc.)

- Doctor’s Certificate (duly filled)

- Medical/Hospital Attendant Certificate

B. Unnatural Death (e.g., Accident, Murder, Suicide, Road/Rail incidents)

- First Information Report (FIR) from the police

- Inquest / Panchnama Report from the police/authority

- Final police investigation report (Chargesheet/Closure report)

- Postmortem Report (PMR) issued by the hospital

- Viscera / Chemical Examination Report (if applicable)

- Driving License (if death due to a road accident and the Life Assured was driving)

- Hospitalization/treatment records (if any before death)

- Newspaper cutting (if available/relevant, e.g., major accident reported)

- Employer’s Certificate (only if the life assured was salaried and the accident occurred in the course of employment)

Things to Consider:

- Attestation is not required if you submit the original documents.

- If copies are submitted, they must be attested by issuing authorities, such as police, hospital, or municipal authorities.

- The claim must ideally be intimated within 90 days of death (genuine unavoidable delays will be condoned).

| Quick Note: In India, life insurers operate under strict IRDAI regulations, and death claims are treated with high priority. After a policy has been in force for three years, Section 45 of the Insurance Act significantly restricts an insurer's right to repudiate a claim. Insurers also know that IRDAI closely monitors their claim settlement numbers quarterly, which directly impacts public trust and their market reputation. A higher settlement ratio builds confidence among customers and also serves as a powerful marketing tool. Due to this regulatory oversight and reputational importance, insurers strive to settle genuine claims promptly rather than risk regulatory action or loss of credibility. |

Ditto’s Take on Term Insurance Claims

At Ditto, we often see that people can easily avoid claim rejections with proper guidance at the time of purchase. That’s why we help you understand what needs to be disclosed, ensure your nominee details are up to date, and remind you about premium deadlines.

Moreover, misunderstandings are common between insurers and customers, which often need an intermediary to resolve the issues. In these cases, Ditto can be the best companion to get things sorted.

Our advisors don’t just sell policies; they stick around to help even during insurance applications and claims, if needed.

Why Choose Ditto for Term Insurance?

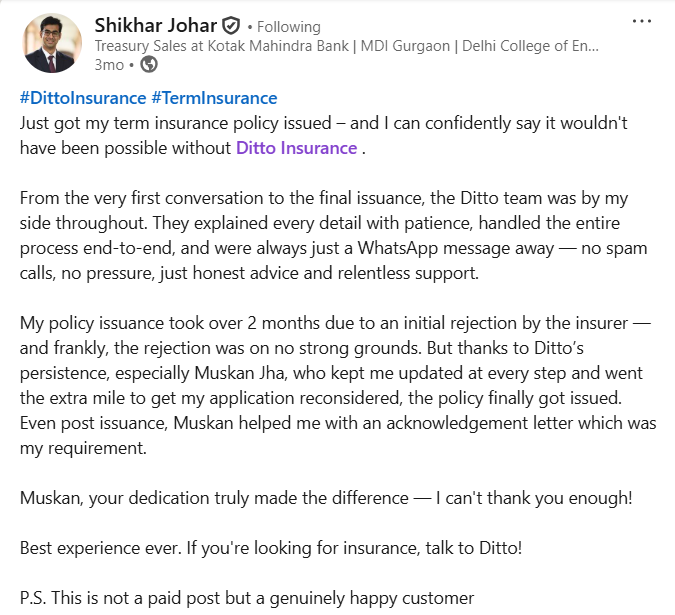

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right term insurance policy. Here’s why customers like Shikhar love us:

✅No-Spam & No Salesmen

✅Rated 4.9/5 on Google Reviews by 15,000+ happy customers

✅Backed by Zerodha

✅Dedicated Claim Support Team

✅100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now!

How Does Term Insurance Claim Work: Final Thoughts

When claiming term insurance, being prepared is the best way to protect your family financially. Always remember that by keeping documents organized, updating policy details, and maintaining transparency, you can ensure a smooth, hassle-free process for your loved ones.

Since not everyone is familiar with how claim settlements work, it is advisable to consult a trusted agent or an intermediary like Ditto. We assist you not only with the insurance application but also guide you through the entire claim process. In short, our advisors make sure your family receives the benefits efficiently and without unnecessary delays.

FAQs

What is the process for filing a death benefit claim in term insurance?

To file a death benefit claim under term insurance, the nominee must inform the insurer, submit the death certificate, policy document, ID/address proof, and a filled claim form. Once all documents are received, the insurer verifies them and generally settles the claim within 15 to 45 days if the information is complete.

What are the reasons for term insurance claim rejection?

It generally occurs due to non-compliance with the insurance policy terms, non-disclosure, or misrepresentation during the application and claim process. Additional reasons include incorrect personal information, undisclosed existing policies, policy lapse, death due to criminal activities, suicide in the first year, and illegal substance abuse, among others.

Can multiple nominees claim a single term policy?

Yes, multiple nominees can be appointed under a single term insurance policy in India, and the policyholder must specify the percentage share each nominee will receive. Upon the policyholder's death, the claim amount is divided among the nominees in proportion to their specified shares. A maximum of three to four nominees can be appointed, and if any nominee is a minor, an appointee (guardian) must be designated to receive the share on their behalf.

Can a loan provider/bank claim the proceeds of a term insurance policy instead of the nominee?

That’s not possible because if the policy is assigned under the MWP Act, it can be legally designated for the exclusive benefit of your spouse and children. This provision ensures that the life insurance payout is directed solely to your beneficiaries and cannot be claimed by anyone else, including creditors or loan companies. You also have the provision to assign your term plan (entirely or a specific share) to the loan provider, upon death they can deduct the amount they are owed and rest is paid to the nominees.

Are deaths abroad covered?

Yes, especially if you are on a vacation or business trip. The same documents and proofs are required, although language gaps and international processes must be taken into account. If you are planning to relocate abroad for work or education permanently, you are required to notify the insurer. Continuation of coverage would depend on the country; if it's a war zone or a high-risk zone, it may be denied.

How does death claim work in case of a missing person in India?

In India, death claims for missing persons need a police FIR and insurer notification. Settlement is usually delayed until a court declares death under Section 108 of the Evidence Act (after seven years). In exceptional cases, such as accidents with strong proof, insurers may settle earlier but with a court declaration or conclusive evidence. If a claim is paid and the missing person later returns alive, the insurer can recover the amount.

What happens if a person’s body is not found in case of a natural calamity?

For calamity-related deaths, insurers don’t usually wait seven years. They accept official proof like a police FIR, certificates from authorities, or government lists of deceased. Nominees submit these with claim papers, and insurers verify before settling. If documents are insufficient, affidavits or a court declaration may still be required.

Last updated on: