Quick Overview

Choosing a ULIP requires understanding how the policy structure, charges, and benefits work in practice. In this blog, we’ll explore the policy details of the HDFC Life Click 2 Invest plan, its key features, charges, lock-in rules, expected returns, and the HDFC Life claim settlement ratio.

What is the HDFC Life Click 2 Invest ULIP Plan?

In the HDFC Life Click 2 Invest plan, a portion of your premium is invested in market-linked funds selected by you. At the same time, the policy provides a life insurance benefit based on the death benefit option chosen at the start. Since the investments are linked to market performance, returns are not guaranteed and may vary depending on how the selected funds perform.

At the time of purchase, you must choose several policy features, including the plan option, death benefit option, premium payment term, policy term, sum assured, and investment funds. The plan offers two plan options, Growth and Loyalty, and four death benefit options: Classic, Classic Plus, Classic Waiver, and Classic Waiver Plus. These choices are fixed at inception and cannot be changed during the policy term.

Policy Type, Eligibility & Investment Options

Who Should Consider This Plan?

The HDFC Life Click 2 Invest ULIP may suit:

- Investors looking for market-linked long-term investments

- Individuals comfortable with market-linked products

- Those who prefer a digital policy purchase and management experience

HDFC Life Click 2 Invest Features and Benefits

1) Premium Allocation and Fund Management Charges

The HDFC Life Click 2 Invest plan has a relatively simple charge structure compared to many older ULIPs.

Key charges include:

- Premium Allocation Charge: Nil

- Fund Management Charge: Up to 1.35% per year for regular funds

- Discontinued Policy Fund Charge: 0.50% per year

- Mortality Charges: Deducted monthly based on the policyholder’s age and level of cover

- Policy Administration Charge: Nil in the Growth option, but applicable in the Loyalty option

For the Loyalty option:

- Single Pay: 0.03% per month of the single premium

- Regular Pay: 0.25% per month of the annualized premium

Additional transaction charges may apply if policyholders exceed the free limits on fund switches, withdrawals, or premium redirections.

2) Insurance and Investment Benefit

The HDFC Life Click 2 Invest plan combines market-linked investment with life insurance protection. However, the exact death benefit depends on the option selected at the policy's inception. The plan offers four death benefit options:

- Classic: The nominee receives the highest of the sum assured (after adjusting applicable partial withdrawals), the fund value, or 105% of the total premiums paid.

- Classic Plus: The nominee receives the higher of the sum assured plus fund value or 105% of the total premiums paid.

- Classic Waiver: The nominee receives the higher of the sum assured or 105% of total premiums paid, and future premiums are waived while the policy continues until maturity.

- Classic Waiver Plus: In addition to the higher of the sum assured or 105% of total premiums paid, future premiums are waived, and a monthly income benefit is provided.

This distinction is important because the plan does not follow a single “higher of sum assured or fund value” structure across all variants. The final insurance payout can vary significantly depending on the death benefit option chosen at inception.

Cost Comparison Insight

3) Partial Withdrawal and Switching Options

The plan also offers flexibility in managing investments during the policy term.

Policyholders can:

- Make partial withdrawals after the lock-in period

- Switch between available funds to adjust their investment strategy

- Use premium redirection to change how future premiums are allocated across funds

Charges, Returns & Policy Details Explained

1) Premium Allocation and Fund Management Charges

The HDFC Life Click 2 Invest plan has a relatively simple charge structure compared to many older ULIPs. It has no premium allocation charge, while the fund management charge is up to 1.35% per year for regular funds and 0.50% for the Discontinued Policy Fund. Mortality charges are deducted monthly based on the policyholder’s age and level of cover.

The Growth option has no policy administration charge, but the Loyalty option includes one. In the Loyalty option, the charge is 0.03% per month of the single premium for Single Pay and 0.25% per month of the annualized premium for Regular Pay. Transaction charges may also apply if withdrawals, fund switches, or premium redirections exceed the free limits.

2) Lock-in Period and Surrender Rules

Like all ULIPs, HDFC Life Click 2 Invest has a mandatory 5-year lock-in period. During this time, the invested amount cannot be withdrawn freely like in a mutual fund. If the policy is discontinued within this period, the fund value, after applicable charges, is transferred to the Discontinued Policy Fund, and the payout is released only after the lock-in period ends.

The Click 2 Invest HDFC Life brochure also includes a discontinuance charge table where charges vary based on the premium type, premium amount, and policy year. After the lock-in period is completed, if the policy is surrendered, the available fund value is paid out, and the policy ends.

Growth vs Loyalty: Which Option Looks Better on Paper?

Performance Metrics Of HDFC Life Insurance

Note: The HDFC Life claim settlement ratio and other metrics shown above refer to the insurer as a whole, not specifically to the ULIP product line. These figures reflect HDFC Life Insurance’s broader performance, including all product categories.

HDFC Life Click 2 Invest Review: Pros, Cons & Verdict

Ideal Investor Profile: The HDFC Life Click 2 Invest ULIP may suit investors seeking a long-term market-linked plan with integrated life cover. However, those prioritizing stronger protection or more efficient wealth creation should compare it with a standalone term plan plus mutual funds.

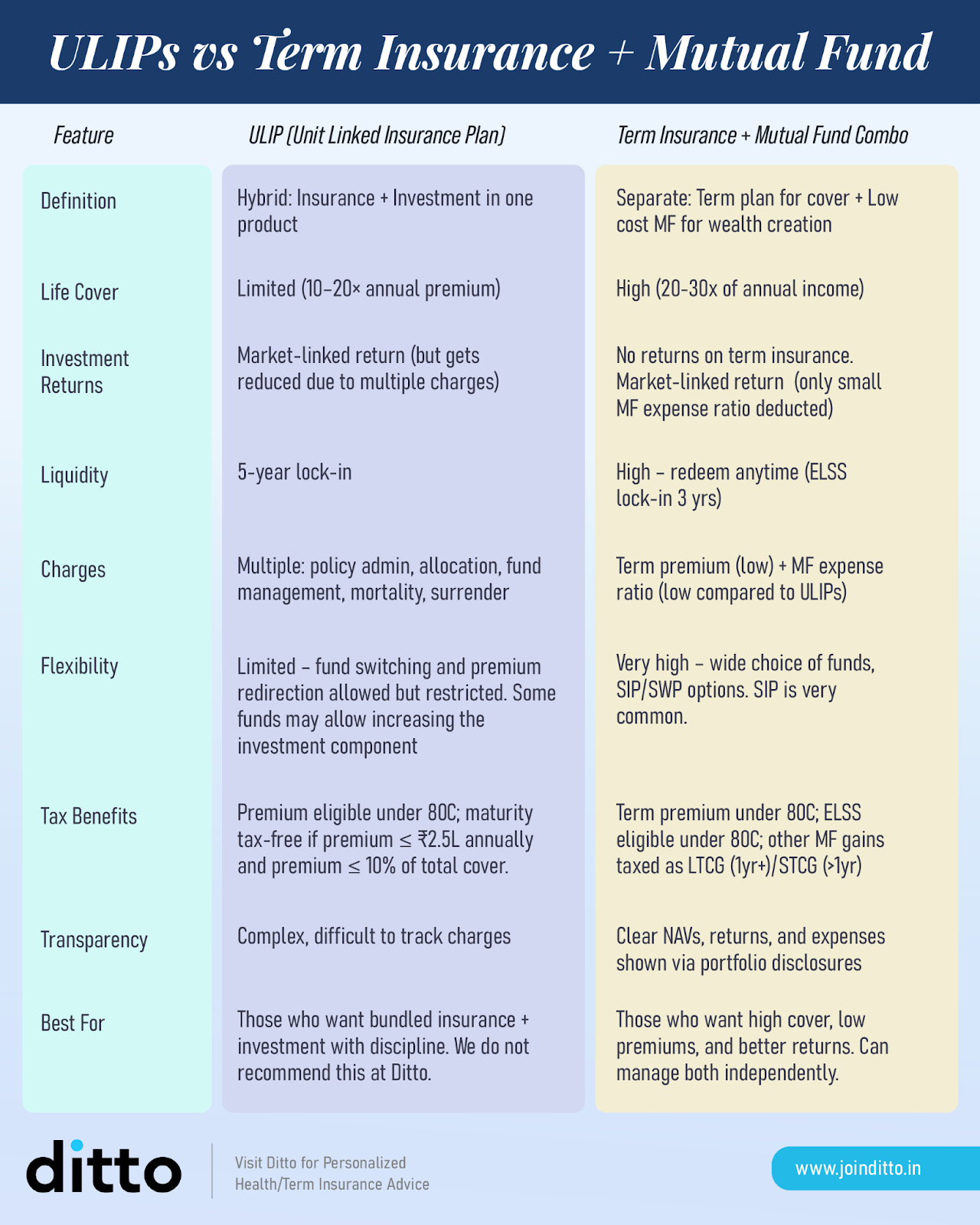

ULIPs vs Term Insurance + Mutual Funds

Many investors compare ULIPs with the alternative approach of buying term insurance for protection and investing separately in mutual funds. The key difference lies in how these products structure insurance and investment.

The comparison above highlights an important distinction. ULIPs combine insurance and investment within a single product, while the alternative strategy separates the two. With a term insurance + mutual fund approach, the term plan focuses purely on providing high life cover, while mutual funds are used for long-term wealth creation.

Why Choose Ditto for Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat on WhatsApp with our expert IRDAI-certified advisors.

Ditto’s Take

HDFC Life Click 2 Invest has a relatively clean charge structure among ULIPs, with zero premium allocation charge and no policy administration charge in the Growth option. However, at Ditto, we generally do not recommend ULIPs because they tend to be structurally less efficient than buying a pure term insurance plan and investing separately. Since ULIPs combine insurance and investment in a single product, they often result in lower life cover relative to the premium, multiple ongoing charges, and reduced flexibility due to lock-in periods.

Instead, separating these goals usually works better. A term insurance plan can provide significantly higher life cover at a lower cost, while mutual funds allow investors to build wealth with greater flexibility and transparency.

When Might This Plan Be Considered?

The HDFC Life Click 2 Invest ULIP may be considered by investors with a long investment horizon, who specifically want a combined insurance–investment product, and who are comfortable maintaining regular premiums throughout the policy term. It may also be relevant for individuals who already have sufficient term insurance or are unable to obtain term coverage due to underwriting constraints.

When It May Not Be Suitable

This plan may be less suitable for those seeking maximum wealth creation, higher life insurance protection, or greater investment flexibility. In such cases, a standalone term insurance plan combined with low-cost mutual funds can often provide better protection and more efficient long-term investment outcomes.

Disclaimer: HDFC Life Insurance is a partner insurer. However, Ditto primarily recommends evaluating their term insurance plans, such as Click 2 Protect Supreme Plus, when looking for pure life insurance protection. This article is intended for educational purposes only. Ditto does not advise on or assist with the purchase of ULIPs.

Frequently Asked Questions

Last updated on: