Quick Overview

Managing a household today requires careful budgeting. With children’s school fees, EMIs, daily expenses, and other financial commitments, most families stick to a strict financial plan. But a single medical emergency can quickly disrupt years of savings. This is where a family floater health insurance plan becomes essential. It’s a simple, cost-effective way to safeguard both health and financial stability.

In this guide, we explore how family floater health insurance works, the best plans available in India, and factors to consider when buying a plan for your family.

How Does a Family Floater Health Insurance Plan Work?

A family floater health insurance plan allows multiple family members to be covered under a single policy with a shared sum insured. All insured members can use this common coverage for medical expenses during the policy year, and claims made by one member reduce the remaining balance available to others. Frequent or large claims can exhaust the coverage if the sum insured is low.

Key Factors to Know About Family Floater Plans

- Premium Based on the Eldest Member: The premium for a family floater policy is usually calculated based on the age of the eldest insured member. When this person moves to a higher age band at renewal, the premium for the entire policy increases.

- Family Floater Suitability: Family floater plans work best for young families with fewer members and lower health risks. Senior citizens or individuals with chronic or pre-existing conditions may benefit more from separate individual policies, as frequent claims could quickly deplete the shared sum insured.

Family Floater vs Individual Health Insurance

When choosing health coverage, many people often compare family floater and individual health insurance plans. If you want a detailed breakdown of how they differ, you can explore our guide on family floater vs individual health insurance.

Best Family Floater Health Insurance Plans in India

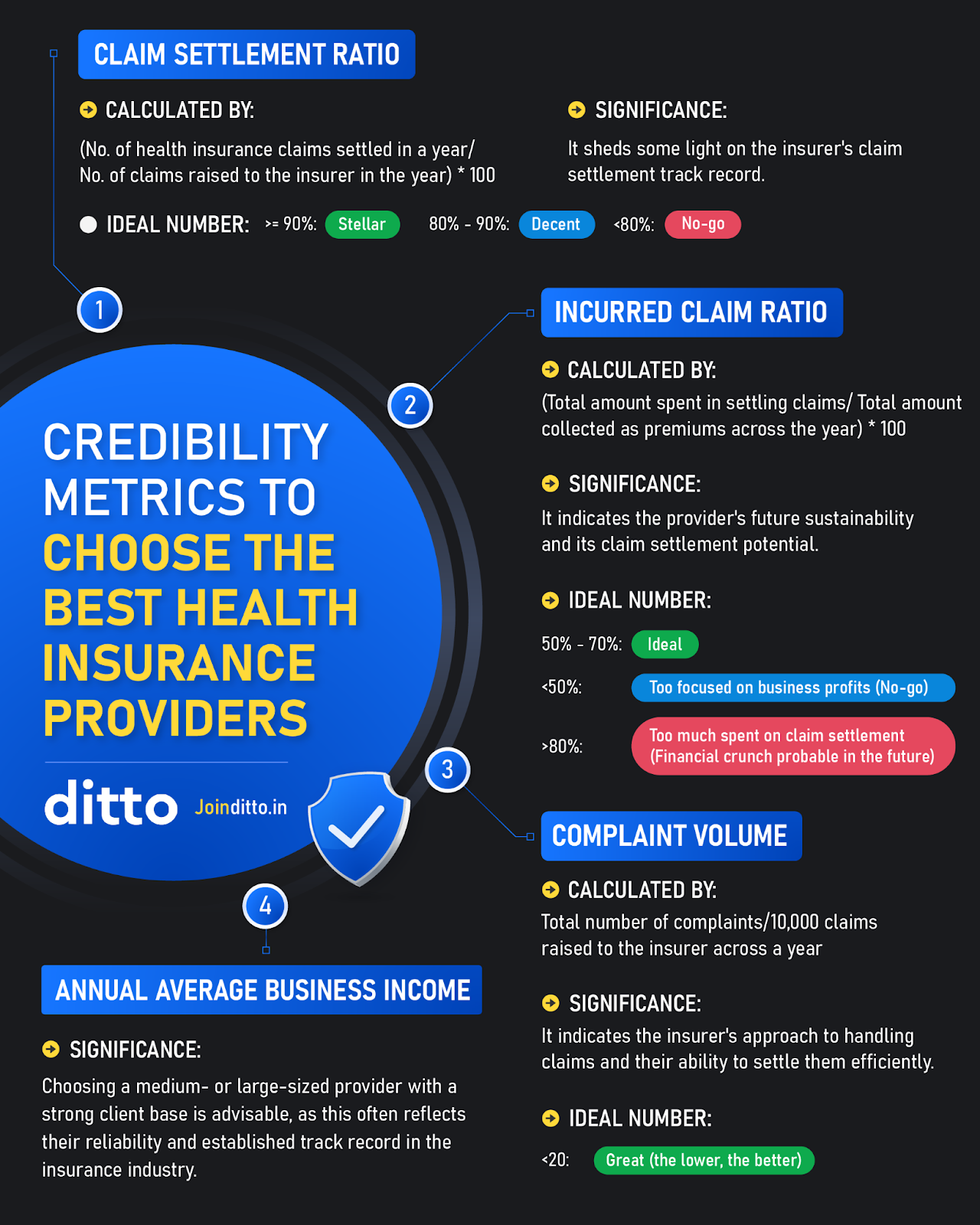

Here, CSR stands for claim settlement ratio and ICR denotes incurred claims ratio.

The plans above are selected based on Ditto’s evaluation framework, which takes into account plan features, performance metrics, hospital network size, and overall policy value.

Ideally, the key metrics of family floater health insurance plans should fall within the recommended ranges shown below.

Family Floater Health Insurance Plans Premium Comparison

Note: These are indicative premiums for a Delhi resident (Pin code: 110001) with a ₹15 lakh sum insured, including recommended add-ons. Actual premiums may vary depending on age, location, medical history, plan variant, and selected add-ons.

Things to Keep in Mind Before Buying a Family Floater Health Insurance Plan

- Check Restoration Benefit Conditions: Many family floater health insurance plans in India offer restoration benefits that reinstate the base sum insured after it is exhausted. Check whether restoration works after partial exhaustion and whether it applies to the same illness or only to different treatments. For instance, if restoration triggers only after full exhaustion and medical expenses exceed the base limit before it activates, you may have to pay the excess out of pocket.

- Watch for Claim Deductions: Some family floater health insurance policies include room rent limits or co-pay clauses. Choosing a room above the allowed limit can lead to proportionate deductions on several hospital expenses. A co-pay means you pay a fixed percentage of each approved claim.

- Check Dependent Age Limits: In most family floater health insurance plans in India, children can be covered from around 90 days until their mid 20s. After crossing the specified age limit, they must transition to a separate individual health insurance plan.

- Understand Newborn Coverage Rules: Newborn coverage rules vary across insurers. In many policies, a newborn is covered only after 90 days from birth and must be formally added to the policy thereafter. However, if the plan includes maternity benefits, the baby may be covered from day 1 , usually up to a specific limit under the maternity health insurance.

- Disclose Medical History Fully: When applying for family floater health insurance, disclose all past illnesses and treatments. Incomplete disclosure may lead to claim disputes later.

- Review Policy Terms Carefully: Before choosing a family floater plan, compare policies based on key metrics such as claim settlement ratio, incurred claim ratio, hospital network, overall performance and customer experience. Also, check the waiting periods in health insurance, policy exclusions, and coverage limits before buying a family floater plan to ensure it fits your family’s needs.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or chat on WhatsApp with us now!

Conclusion

A family floater health insurance plan is ideal for families seeking a single, shared health cover that is cost-effective and easy to manage. It works particularly well for couples or parents with young children.

Senior parents can be covered under a separate floater plan. Whereas members with chronic health conditions can opt for individual health insurance policies to ensure adequate coverage without exhausting the shared sum insured.

Ultimately, choosing between family floater vs individual health insurance depends on your family’s age profile, health risks, and coverage needs. Review plan features carefully, compare options, and select a policy that provides adequate protection and long-term financial security.

Disclaimer: This content is meant for informational purposes and is based on publicly available information. Insurance policy terms may change over time, so it is important to review the official policy wording and speak with a licensed advisor before making a purchase decision. Ditto currently partners with HDFC ERGO, Care, Aditya Birla, and Niva Bupa.

Frequently Asked Questions

Last updated on: