Student health insurance covers medical costs during your studies. Depending on the location where you study, plans cover hospitalization, mental health, dental, and emergency evacuations. You can utilize sponsored university plans, extend a family floater plan, or purchase specialized domestic and overseas student policies.

Students studying abroad often need specialized overseas student health insurance to meet visa and university requirements. When choosing a plan, students should check hospital networks near campus, room rent limits, disease-wise limits, and access to cashless treatment. At Ditto, we recommend Optima Secure+, backed by HDFC ERGO with a 96.71% average claim settlement ratio. A 20-year-old in Delhi would pay about ₹12,669 a year for a ₹15 lakh cover under this plan.

This guide is ideal for students looking for a comprehensive health plan.

As more students move to new cities and countries for education, medical emergencies can quickly become financial emergencies. Student health insurance helps protect against unexpected hospital bills, so students can focus on their studies without added financial stress on their families.

This guide breaks down the best student health insurance plans, costs, and key factors students and parents should compare before buying a health plan.

Student health insurance helps cover medical expenses during academic years, including hospitalization, accidents, surgeries, and illnesses. In India, students are often covered under a family floater policy or through an individual health insurance plan. Students studying abroad may receive coverage through university group insurance or specialized overseas student plans offered by Indian insurers.

Take Note: In health insurance, the term “students” is not limited to college-goers. It usually includes school, college, and university students, as well as individuals studying in India or abroad, generally up to age 25. The age limit is commonly set around 25 because insurers allow financially dependent children to remain covered under their parents’ family floater policy until that age.

Ditto’s Pick for Best Student Health Insurance Plans (2026)

01

HDFC ERGO

Optima Secure+

Optima Secure+ focuses on dependable coverage, smooth claims support, and meaningful benefits that are especially valuable during major medical emergencies.

HDFC ERGO

Optima Secure+

4.6

Overall Rating

Premium Rating

3.0/5

Insurer Rating

5.0/5

Feature Rating

4.6/5

Customer Service Rating

5.0/5

Core Benefits

Secure Benefit doubles your base cover from day one

Unlimited Restore refills your cover after every claim, regardless of the number of claims in the same year

The sum insured increases by 100% each year, with no upper cap

Consumables like gloves, masks, and syringes are covered

Add-on options like Limitless, where you get unlimited coverage (without any upper cap) for a specified number of claims during the policy tenure

Why Optima Secure+

HDFC ERGO Optima Secure+ works well for students because it combines strong hospitalization coverage with long-term flexibility at a relatively young entry age.

02

Care

Supreme

Care Supreme balances strong features with relatively affordable pricing. It suits students seeking higher restoration benefits and long-term bonus growth without stretching the budget too far.

Care

Supreme

4.5

Overall Rating

Premium Rating

5.0/5

Insurer Rating

4.2/5

Feature Rating

4.5/5

Customer Service Rating

3.0/5

Core Benefits

Unlimited restoration for related and unrelated claims

Cumulative bonus up to 100%

Bonus extension up to 500% or unlimited accumulation through add-ons

Wellness rewards with renewal discounts up to 30%

Additional add-ons for consumables, annual health check-up, and gym sessions

Why Care Supreme

Care Supreme is a practical option for students who want strong recharge benefits and long-term coverage while keeping premiums manageable.

3

Aditya Birla

Activ One MAX

Activ One MAX is designed for younger and health-conscious individuals and families. It combines strong hospitalization coverage with wellness-focused rewards and long-term savings opportunities.

Aditya Birla

Activ One MAX

4.4

Overall Rating

Premium Rating

5.0/5

Insurer Rating

4.5/5

Feature Rating

4.3/5

Customer Service Rating

5.0/5

Core Benefits

Unlimited restoration from the second claim onward of the policy lifetime

100% cumulative bonus every year up to 500%, and is unaffected by claims

HealthReturns rewards healthy lifestyle habits with a renewal premium discount

Why Activ One MAX

Aditya Birla Activ One MAX works well for students because it combines comprehensive hospitalization coverage with wellness-focused benefits that suit younger individuals.

4

Niva Bupa

ReAssure 2.0 Platinum+

ReAssure 2.0 Platinum+ is a feature-rich plan created for long-term use. It is especially useful for individuals expecting multiple claims over the years and wanting stronger refill benefits.

Niva Bupa

ReAssure 2.0 Platinum+

4.3

Overall Rating

Premium Rating

5.0/5

Insurer Rating

4.2/5

Feature Rating

4.2/5

Customer Service Rating

3.0/5

Core Benefits

Unlimited restoration after every claim through ReAssure+

Premium age-lock until the first claim (medical inflation or insurer-wide re-pricing can still increase premiums)

Booster+ benefit that carries forward unused cover up to five times

Safeguard rider for non-payable items and bonus protection

Wellness rewards of up to 30% premium discounts on renewal

Why ReAssure 2.0 Platinum+

Niva Bupa ReAssure 2.0 Platinum+ is well-suited for students because it offers long-term flexibility and strong restoration benefits, which can be useful during repeated medical emergencies.

5

SBI

Super Health Platinum Infinite

Super Health Platinum Infinite is designed for those seeking high coverage along with advanced healthcare and wellness features.

SBI

Super Health Platinum Infinite

4.1

Overall Rating

Premium Rating

5.0/5

Insurer Rating

3.8/5

Feature Rating

4.2/5

Customer Service Rating

3.0/5

Core Benefits

Unlimited reinstatement with up to 200% cover per claim

Built-in OPD and consumables cover

1 year waiting periods for specific illnesses and 2 years for pre-existing diseases

Health Multiplier benefit up to 3x of the base cover once a year for any listed critical illnesses

Talk to an expert today and find the right insurance for you.

How Much Does Student Health Insurance Cost?

If you are about to exit your family floater plan and switch to independent health coverage, here’s an indicative premium example with recommended add-ons for a ₹15 lakh sum insured for people residing in Delhi (110010).

Sample Premiums Across Ages and Plans

Plan

18 Years

25 Years

HDFC ERGO Optima Secure+

₹12,353

₹13,459

Care Supreme

₹16,294

₹16,294

Aditya Birla Activ One Max

₹10,149

₹10,149

Niva Bupa ReAssure 2.0 Platinum+

₹11,535

₹11,535

Note: If you'd like to explore the detailed figures reported by insurers and the IRDAI in their annual disclosures and public reports, visit Ditto Data Labs, our proprietary repository of health insurance data, meticulously compiled, verified, and maintained by the Ditto team over the years.

Who Should Buy Student Health Insurance Plans?

Students Living Independently: Working students, freelancers, PhD scholars, married students, or those above the dependent-child age should consider buying an individual health insurance plan.

Online and Distance Learning Students: Students studying remotely from home usually do not require specialized overseas student insurance. Online student health insurance helps students easily compare, purchase, and manage medical coverage from anywhere, with protection for health emergencies.

Students With Higher Medical or Lifestyle Risks: Students with existing medical conditions, active sports participation, frequent travel, or limited parental coverage may need stronger personal health coverage.

Students Studying Abroad: Students moving overseas for higher education should buy a student travel or international health insurance plan accepted by the university and visa authorities. Plans like HDFC ERGO Student Suraksha and Tata AIG Student Travel are specially designed for students studying abroad and offer protection for medical emergencies, travel risks, and university-related requirements.

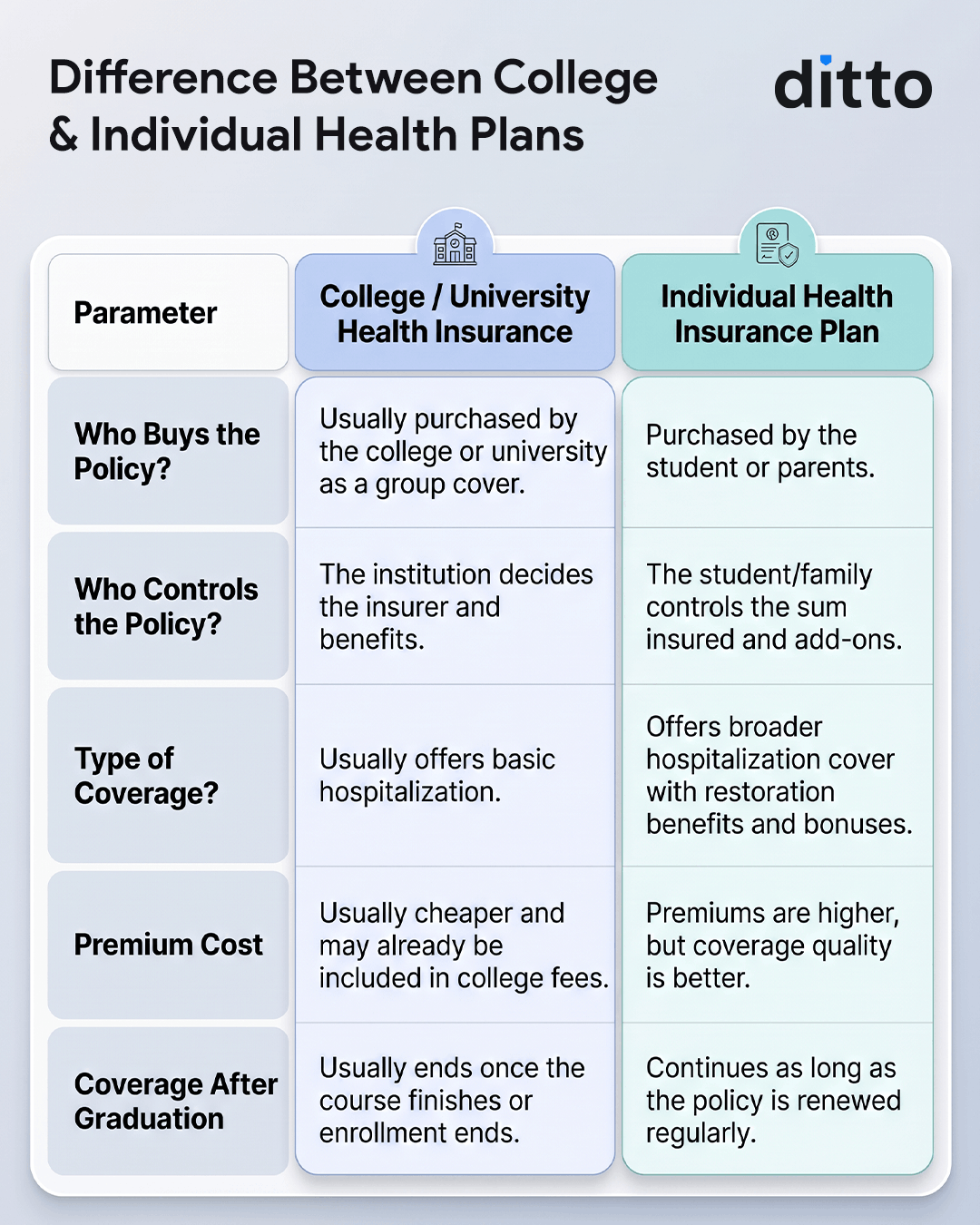

Are College Health Insurance Plans Enough?

Many college health insurance policies appear adequate based on the headline sum insured, but the fine print can significantly affect claim payouts in a medical emergency.

Take the example of the Indian Institute of Management Calcutta. As per the 2025–26 MBA student insurance structure, students receive a medical cover of ₹3 lakh. However, normal room charges are capped at ₹6,000 per day, while ICU single-bed charges are limited to ₹12,000 per day.

At first glance, these limits may appear reasonable. But in metro cities, many private hospitals charge much higher room rents. Once you select a room above the allowed limit, insurers may apply proportionate deductions. So even if the total hospital bill stays within the ₹3 lakh sum insured, families may still face substantial out-of-pocket expenses. This is why students should treat university-provided insurance as a support layer, not a complete health protection solution.

Take a look at the infographic for a clear picture of the differences between college and individual health plans.

Why Should Students Buy Health Insurance?

01

Medical Emergencies Can Become Expensive

Student health insurance helps cover emergency treatments. This protects students and families from unexpected medical bills during academic years.

02

Important for Active Student Lifestyles

Students often travel daily, use two-wheelers, or participate in sports and outdoor activities. Health insurance helps manage accident-related medical costs and emergency care expenses.

03

Builds Long-Term Continuity Benefits

Early coverage helps preserve waiting period credits, accumulate bonuses, and policy continuity when moving from a family floater to an individual policy later.

04

Mental Health Support Has Become Essential

Academic pressure and social stress can affect mental well-being. Modern student health insurance plans include mental health hospitalization support. However, coverage for therapy sessions and psychologist consultations varies across health insurance plans.

05

Valuable for Students Studying Abroad

International student health insurance can cover hospitalization, emergency treatment, study interruption, and sponsor protection during overseas education.

06

Early Purchase Keeps Premiums Lower

Students are generally younger and healthier, which makes health insurance more affordable by avoiding loading charges.

07

Helps Protect Academic Continuity

A serious illness can disrupt studies and increase expenses for tuition, travel, or recovery.

Did You Know?

According to The IndianExpress, over 18.8 lakh Indian students were studying abroad across 153 countries, including more than 12.5 lakh enrolled in universities and higher education institutions. This highlights the growing need for strong student health and travel insurance protection.

Things to Keep in Mind Before Buying Student Health Insurance

Avoid Room Rent Limits: Plans with room rent caps can reduce your final claim payout through proportionate deductions. Choose plans with no room rent restrictions to avoid unexpected out-of-pocket expenses.

Disclose Your Medical History Honestly: Always include your medical history. Non-disclosure remains one of the biggest reasons for claim rejection in India.

Stay Away From Co-payments and Disease-wise Limits: A co-payment means you pay part of every claim yourself. Disease-wise sub-limits restrict payouts for illnesses such as cataracts or hernias, even if your overall cover is high. Plans without these restrictions offer better financial protection.

Understand Restoration Benefits: Restoration benefits refill your sum insured if it gets exhausted during the policy year. This becomes useful during repeated treatments or multiple hospitalizations.

Check the No-Claim Bonus (NCB): Many insurers reward claim-free years by increasing your sum insured without a matching rise in premium. Over time, this can significantly increase your available cover and improve long-term value.

Look for Consumables Cover: Standard policies may exclude non-medical hospital items such as gloves, masks, or syringes. These expenses can still add up. Plans or add-ons covering consumables help reduce final out-of-pocket costs.

Verify the Hospital Network: Check whether the insurer has cashless hospitals near the college, hostel, or student accommodation. A strong nearby hospital network makes emergency treatment faster and less stressful.

Note: If you are covered under a family floater plan, find out the maximum age at which you can stay on the policy. Most insurers ask students to move to an individual plan around age 25. Under IRDAI rules, insurers must allow migration to an individual policy with waiting period credits intact if you apply at least 30 days before the exit age.

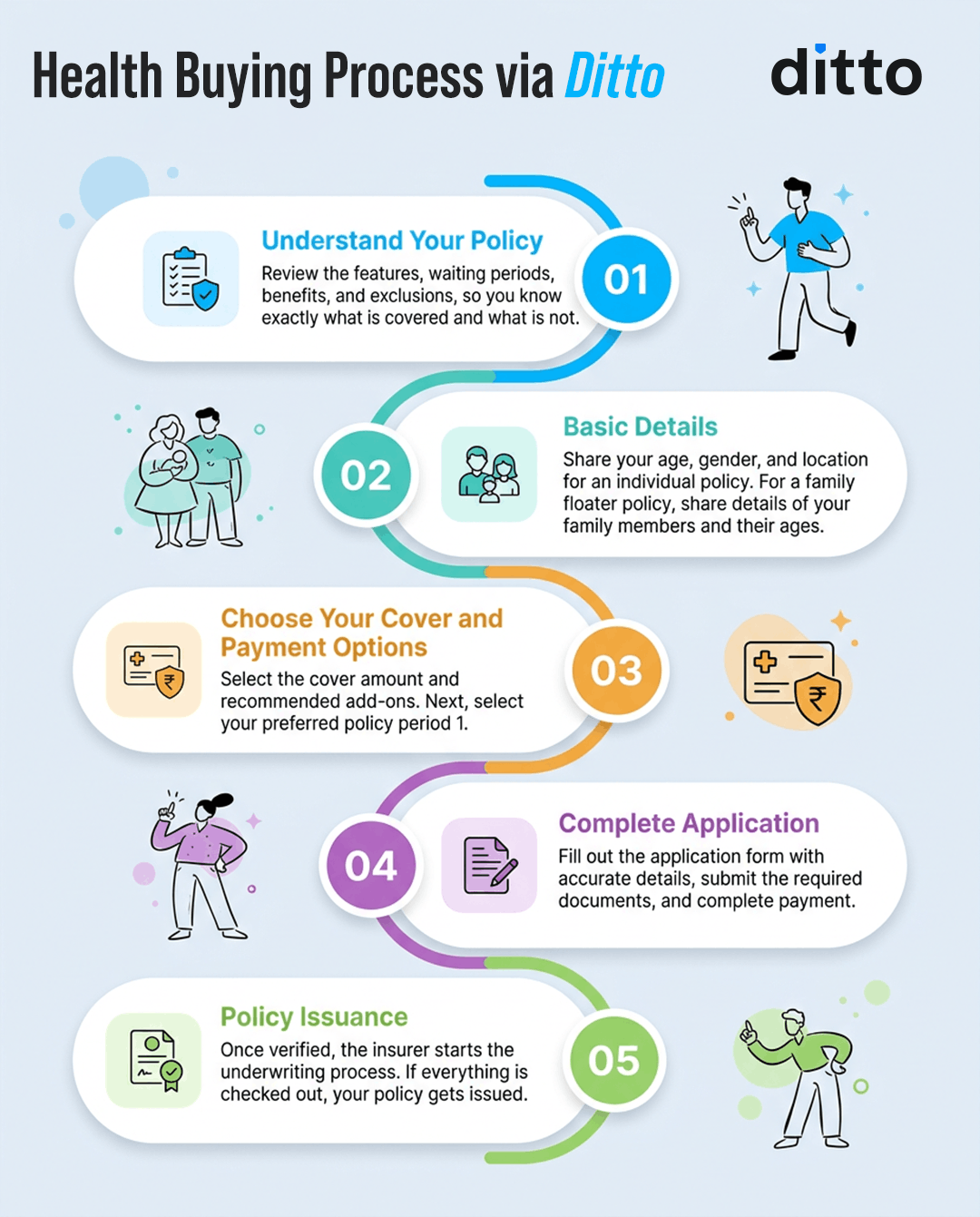

How to Buy Student Health Insurance Online Through Ditto?

At Ditto, we help students and parents choose the right health insurance plan based on budget, medical needs, and study location. Our team supports you through documentation, underwriting, policy purchase, and claims assistance, making the entire process simpler, faster, and less stressful during medical emergencies.

Take a look at the infographic to understand how the process works:

For students studying overseas, we often recommend a combination approach. An Indian health insurance plan helps maintain coverage for treatment and medical needs back home, while a separate health plan from the country of study provides local coverage for emergency care there.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

Backed by Zerodha

Dedicated Claim Support Team

100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or chat on WhatsApp with us now!

Ditto’s Take On Student Health Insurance

Student health insurance is not just about managing medical emergencies; it is also an important financial safety net that protects students from unexpected healthcare costs.

Start Early: If you do not have any health coverage, it is recommended to buy an individual health plan at a young age. It keeps costs lower and helps build continuity benefits that become valuable over the years.

University Plans Have Limitations: University group health plans are useful during the course period, but they often come with room rent restrictions, lower flexibility, and limited benefits. They work best as temporary support rather than complete long-term protection.

Overseas Students Must Compare Carefully: Students studying abroad should compare university student health insurance plans (SHIP) with Indian overseas student insurance plans in detail. The policy should still comply with visa rules and ensure reliable local acceptance.

Personal Health Insurance Offers Long-Term Security: Employer or university health cover should not be your only protection. A personal health insurance plan provides portability, continuity of coverage, and long-term coverage even after graduation, relocation, or job changes.

At Ditto, we believe student health insurance should be treated as an early financial planning decision, not just a college requirement. A well-chosen plan protects savings, builds long-term continuity, and gives both students and parents greater confidence during important academic years.

Full Disclosure

This article is purely for informational purposes and offers an unbiased review of health insurance plans from both our partner and non-partner insurers. The information has been sourced from IRDAI reports, insurer websites, policy documents, and other publicly available data. To understand how our experts evaluate and shortlist health insurance plans, explore Ditto’s Cut.

Frequently Asked Questions

What is student health insurance in India?

Student health insurance is a health policy that covers medical expenses during academic years. It usually includes hospitalization, surgeries, accidents, day-care procedures, and illnesses. In India, students are commonly covered under a parent’s family floater plan, a university group plan, or an individual health insurance policy. Students studying abroad may also require specialized overseas student insurance to comply with visa and university requirements. In insurance terms, “students” includes school, college, and university students, as well as young adults up to around age 25. The right option depends on age, location, study duration, and future healthcare needs.

How long can a student stay on their parents' health insurance in India?

Most family floater plans in India allow dependent children to remain covered until age 25. Some insurers offer extended limits. For example, plans like Niva Bupa ReAssure 2.0 Platinum+ and SBI Super Health Platinum Infinite have no fixed exit age. This can help students in postgraduate or doctoral programs. Under IRDAI’s migration rules, students who apply at least 30 days before the exit age can switch to an individual plan while retaining continuity benefits, such as waiting-period credits. At Ditto, we recommend planning this transition early to avoid coverage gaps later.

Should students buy their own health insurance or stay on their parents' plan?

For most financially dependent students, staying on a parent’s family floater plan is usually the most practical and cost-effective choice. It keeps premiums lower and helps build continuity benefits for future coverage. However, working students, freelancers, married students, PhD scholars, or those above the dependent exit age should consider buying an individual health insurance policy. A personal plan offers better long-term flexibility and portability. At Ditto, we also advise students not to rely solely on university group insurance, as it often comes with room-rent caps, lower coverage limits, and restrictions once the course ends or graduation is complete.

How much does student health insurance cost in India?

The cost of student health insurance depends on factors like age, city, insurer, medical history, and type of coverage. For an 18-year-old student, premiums for a ₹15 lakh cover in Delhi generally range between ₹10,000 and ₹17,000 per year across popular plans like HDFC Optima Secure +, Aditya Birla Activ One Max and Care Supreme. Since students are usually younger and healthier, premiums remain relatively affordable. Buying early also helps lock in continuity benefits, avoid loading charges, and makes underwriting easier.

What is the best health insurance plan for students in India in 2025 or 2026?

At Ditto, one of our top recommendations for students is HDFC ERGO Optima Secure+. It reported a strong average claim settlement ratio of 96.71% across FY 2022 to 2025 and offers access to a large hospital network. The plan doubles the base cover from day one, includes unlimited restoration and bonus accumulation, and covers consumables. Other strong options include Care Supreme and Aditya Birla Activ One MAX. The ideal plan depends on budget, expected duration of coverage, dependent exit age, and whether the student plans to study in India or abroad.

Do students need health insurance if they have college group insurance?

College or university group insurance is useful, but it should not be treated as complete protection. These plans usually last only for the course period and often include caps on room rent, lower sum-insured limits, and restricted benefits. They may also not offer portability or long-term continuity once the student graduates. A personal health insurance policy provides students with stable, long-term coverage that continues through job changes, relocations, and different life stages. At Ditto, we believe students should view personal health insurance as an early financial planning decision rather than only a university enrollment requirement or temporary backup cover.

Does health insurance cover mental health for students in India?

Yes, health insurance plans in India are required to include mental health coverage. IRDAI mandates insurers to treat mental illness on par with physical illness for hospitalization purposes. This means psychiatric conditions that require inpatient treatment are covered under many standard health insurance plans. For students dealing with academic stress, relocation challenges, anxiety, or social pressure, this benefit has become increasingly important. Some plans may also offer outpatient mental health consultations through OPD add-ons or wellness services. At Ditto, we recommend checking mental health coverage carefully before purchase, especially for students living away from home or studying abroad.

What is the restoration benefit in health insurance, and why does it matter for students?

A restoration benefit replenishes your sum insured after it is exhausted by claims during the same policy year. Some plans restore the coverage only for unrelated illnesses, while stronger plans restore it for both related and unrelated conditions. This feature is valuable for students because medical emergencies or repeated treatments can happen unexpectedly within a short period. Students with active lifestyles, chronic conditions, or sports exposure may benefit significantly from this feature. Plans like HDFC ERGO Optima Secure+ offer unlimited restoration, meaning the sum insured can be replenished multiple times in a year.

Can parents claim tax benefits for paying their child's health insurance premium?

Yes, parents can claim tax deductions for health insurance premiums paid for dependent children under Section 80D (old regime) of the Income Tax Act. The deduction limit is up to ₹25,000 annually for eligible family members, including children covered under a family floater or individual policy. If senior-citizen parents are also covered, the overall deduction eligibility may increase further. Health insurance premiums, therefore, offer both financial protection and tax efficiency for families. At Ditto, we encourage families to view student health insurance as a long-term financial planning tool rather than just a short-term medical expense during educational years.

What is a no-claim bonus in health insurance, and how does it benefit students?

A no-claim bonus increases your sum insured for each claim-free year, with no extra premium. Since students are generally younger and healthier, they may go several years without making a claim. Some plans offer very high bonus limits through optional add-ons. For example, certain policies can increase coverage multiple times the base sum insured, such as Optima Secure+, which offers 100% p.a. bonus accumulation with no upper cap. The no-claim bonus is one of the biggest long-term advantages of buying health insurance early rather than waiting until later adulthood.

Customer Reviews

4.9

20915 reviews

Ditto is doing really great. Absolutely spam free- that's the best part. They don't talk to you like they are forced to sell the product. It's more like, helping us buy better. Advisor Nuha was very patient and answered all my questions with clarity. Thanks for the service

I

INDHUMATHI M

Loved the service! Maheta Nidhi Hitesh was incredibly helpful and knowledgeable. She guided me through the whole process and made everything super easy to understand. I really appreciated how patient she was with all my questions—there was no pressure at all, just clear and honest advice. Honestly, I'm very happy with my experience at Ditto so far. Highly recommend!

RK

Ragul Kumar

I had a great experience with Ditto while exploring health insurance options. The process was smooth and everything was explained clearly.

A special thanks to Swaroop SK for patiently answering all my questions and guiding me through the policy details without any pressure. The transparency and support made it much easier to understand and choose the right plan.

Really appreciate the assistance!

PS

Pulkit Singh

Had a great experience with Ditto Insurance. Ishita Sudrania was extremely helpful in guiding me through choosing the right term plan. There was no spamming or sales pressure, and all my questions were patiently answered. She also assisted me thoroughly with the entire application process. Highly recommend!

SS

Samil Shah

I had a great experience with Ditto while filing my health insurance claim. Their team guided me clearly through the entire process, helped with the required documents, and promptly answered all my queries. Their support made the claim process much smoother and less stressful. Highly appreciate their assistance.