The rising doctor fees, high cost of medical services and medications, accompanied by the increased chances of health complications (despite all our kale diet) and the peek-a-boo at the fragility of human lives (courtesy: COVID-19) have all motivated the Indian masses to reach out for the best health insurance plans available. If you’re trying to narrow down your options, our curated list of the best health insurance plans in India can serve as a useful starting point to understand how leading policies compare on coverage, features, and pricing.

Fortunately and unfortunately, health insurance providers caught a whiff of the spiked demand much before it actualised, and hence, we have multiple new players and plans. While this offers potential policyholders more options to choose from, it also leaves them confused about which insurer and policy they should rely on. Now, in a true marketing venture, most of the new players in the market have come up with innovative features that are appealing and intriguing. On the other hand, the steady providers play to their strength and keep working on their claim settlement experience and affordability factors. One such player is HDFC Ergo. As of recently, the insurer has launched an economical alternative to its flagship Optima Secure plan - the HDFC ERGO Optima Lite.

While HDFC Ergo is often considered one of the stronger health insurance providers in the market, that does not automatically make every policy from its portfolio a perfect fit. The launch of Optima Lite is particularly interesting because it attempts to address the perception that HDFC Ergo plans tend to be slightly premium-priced compared to peers. But does “affordable” here mean smart value, or are there feature trade-offs involved?

To answer that, we take a closer look at the plan’s structure, benefits, limitations, and pricing in our detailed HDFC ERGO Optima Lite customised review, where we evaluate whether it genuinely delivers value or trims down essential protections in the name of affordability.

| Quick Verdict On HDFC ERGO Optima Lite |

|---|

| HDFC Ergo Optima Lite is a new plan from the stable that has been marketed as an affordable alternative to the insurer’s flagship plan - HDFC Ergo Optima Secure. |

| Unfortunately, the Optima Lite plan seems to have brought in an affordability quotient at the cost of HDFC Ergo’s most prized USP - comprehensiveness. The policy has a few too many restrictions in the form of low coverage, room rent restrictions, low pre and post-hospitalisation coverage, and more. Additionally, the plan is only available for Tier 2 and Tier 3 cities. |

| Overall, we would say, unless you are absolutely sure that HDFC Ergo Optima Lite is the way to go, stick with Optima Secure! |

Pro tip: The health insurance market can be a labyrinth. Instead of spending hours navigating through the hundreds of policies out there, why not book a 30-minute call with our expert IRDAI-certified advisors? We don’t spam or pressure you to buy. Just honest insurance advice.

Comprehensive Review of HDFC ERGO Optima Lite

- HDFC ERGO Optima Lite: Brief

Founded in 2002 as a joint venture between India’s HDFC and Germany’s ERGO International AG, HDFC Ergo has been at the forefront of the health insurance industry. The insurer has a vast client base courtesy of its excellent claim settlement experience and track record, as reported by its policyholders. Apart from that, here is a quick look at the metrics of HDFC Ergo that throw some light on its credibility -

| Insurer | Claim Settlement Ratio (CSR) | Incurred Claim Ratio (ICR) | Complaint Volume | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Ideal Numbers | >= 90% | 50% - 70% | <20 | |||||||||

| Years | 2021 - 2022 | 2022 - 2023 | 2023 - 2024 | Avg | 2021 - 2022 | 2022 - 2023 | 2023 - 2024 | Avg | 2021 - 2022 | 2022 - 2023 | 2023 - 2024 | Avg |

| HDFC Ergo | 100 | 95.49 | 97.19 | 97.56 | 97.47 | 79.04 | 80.98 | 85.83 | 7.95 | 6.23 | 6.89 | 7.02 |

| Industry Average | 85.85 | 91.18 | 92.25 | 89.76 | 90.51 | 79.94 | 81.322 | 83.93 | 18.7 | 19.51 | 29.76 | 22.66 |

(The data above is an average of three years. The average of the data across 3 years is meant to provide you with a better insight into the insurer’s consistency across its overall operational proficiency and its progress graph.)

You might also be interested to know that HDFC Ergo has ties with over 12500+ network hospitals.

Overall, HDFC Ergo strikes all the right chords with its potential and existing policyholders, proving why it’s considered one of the best health insurance providers in the country. However, much like any other insurer, this provider, too, has a drawback that you would need to consider - most of the health insurance products from this stable are comparitively pricier than that from its competitors.

Now, this is what makes the HDFC Ergo Optima Lite policy a plan to be discussed - an affordable product from HDFC Ergo would generally mean the best of both worlds: affordability and assurance of the best provider in the business. However, the concern is that Optima Lite might have compromised with HDFC Ergo’s USP of comprehensive policies in the hope of dropping prices to match its peers.

Unfortunately, our concern seems to have been actualised -

HDFC Ergo Optima Lite is one of the most basic offerings from the HDFC Ergo stable that provides coverage of either ₹5 or ₹7.5 lakhs. Now, the policy retains some of the standard features

- A pre-existing waiting period of 3 years,

- Daycare coverage,

- Domiciliary coverage,

- AYUSH treatment coverage and

- Unlimited restoration perks for the same and different ailments,

-there are multiple restrictions across the policy that raise the question: is HDFC Ergo Optima Lite genuinely worth the purchase?

Well, decide for yourself: as per the insurer’s claims, Optima Lite is supposed to be the affordable alternative for its flagship plan, Optima Secure. However, HDFC Ergo Optima Lite has quite a few restrictions, some of which can’t exactly be brushed off. Here’s a quick look at some of the most concerning cons of this policy -

- The plan is unavailable for Tier 1 cities (living in Tier 1 doesn’t mean the residents don’t need affordable policies!)

- The offered coverage is only ₹5 lakhs or ₹7.5 lakhs, which might fall substantially short, considering the increased cost of medical treatments and procedures.

- The plan has a room rent restriction of up to 1% and an ICU room rent restriction of up to 2% of the sum insured.

- Pre-hospitalisation and post-hospitalisation coverage are only offered for 30 days and 60 days, respectively.

Keeping these cons in mind, if you are still planning on availing the HDFC Ergo Optima Lite plan for the offered edge of affordability and the assurance of the insurer’s credibility, here‘s a detailed look into the features. Make sure to go through these details carefully before you purchase the policy -

Table of the Features of HDFC ERGO Optima Lite

| Features | Details |

|---|---|

| Coverage | ₹5 lakhs | ₹7.5 lakhs |

| Copayment | No |

| Room Rent Restrictions | Up to 1% | Up to 2% (for ICU rooms) |

| Disease-Wise Sub-Limits | No |

| Affordability of Premiums | Affordable |

| Waiting Period | 3 years (pre-existing medical ailments) 2 years (Specific Illness) 30 days (Initial) |

| Domiciliary Coverage | Yes (Up to the sum insured) |

| Daycare Coverage | Yes (Up to the sum insured) |

| AYUSH coverage | Yes (Up to the sum insured) |

| Pre and Post Hospitalisation | 30 and 60 days, respectively |

| Preventive Health Check-up | Yes |

Should You Buy HDFC ERGO Optima Lite?

- HDFC ERGO as a health insurance provider: HDFC Ergo is undoubtedly one of the country's most popular health insurance providers. While the insurer deals in multiple insurance genres (car, bike, cyber, home, and health), its health insurance product portfolio is the most well-known, considering the comprehensiveness and diversity across the product portfolio. Because of these pros, policyholders agree to pay slightly higher premiums when compared to the other plans launched by its competitors.

Additionally, if you consider the credibility metrics of HDFC Ergo, purchasing a health insurance plan from this provider means you have access to a top-notch insurer. All of this combined makes HDFC Ergo the perfect choice for you.

However, you should also know that, much like the case with any insurance provider, not all policies from this stable are a good choice. So, make sure to pick out a comprehensive plan that offers ample room for customisation and is yet comparatively priced.

- In-Built Features: As a base policy, the HDFC Ergo Optima Lite plan offers a few features. Unfortunately, some of these features are pretty restrictive, which might lead a potential policyholder to seek out a more comprehensive plan. Here is a quick look at its in-built features -

- Coverage: when calculating the health insurance coverage for a plan, we always recommend that you look into the following -

- The number of policyholders covered under the plan

- The medical requirement and hospitalisation history of the individuals to be insured

- The age of the policyholders (the older they are, the higher the chances of sizeable hospital bills, considering the higher risk of acquiring ailments)

- Your financial bandwidth (the higher the sum insured, the higher the premium)

Usually, the minimum offered coverage, even for individuals, is ₹10 lakhs, considering the spiked cost of medical treatments and services and the projected medical inflation. Again, with standard policies, you can always start lower, if you are young or have a limited financial bandwidth and increase the cover later as per your requirement.

However, in the case of HDFC Ergo Optima Lite, there are only 2 options in terms of the sum insured - ₹5 lakhs and ₹7.5 lakhs. This sum will definitely fall short when catering to medical treatments requiring long-term care/treatments. And you will end up paying out of your pocket despite having trusted one of the leading health insurance providers.

- Copayment: Copayment in health insurance might seem appealing at the start, considering that you will be required to pay less in terms of premiums; however, in the long run, it might not be the best financial decision. With a copayment feature in your health insurance policy, you must pay off a share of your bill, while the insurer only covers the other part. So, despite paying a premium and having an active health insurance plan, you will still be digging into your pocket. So, we generally recommend avoiding copayment in your plans (except for 2 cases - senior citizens' plans and plans for patients with critical conditions/ailments).

In the case of HDFC Ergo Optima Lite, no copayments are involved, which is a significant pro for individuals planning to purchase this plan.

- Disease-Wise Sub-Limits: Say you have a ₹5 lakh health insurance policy that comes with a disease-wise sub-limit in the case of cardiac surgeries of up to ₹1 lakh. Under such circumstances, despite having a health insurance plan, in case your heart surgery expenses exceed ₹1 lakh, you will have to pay the balance amount out of your pocket. This is one of the features that we recommend our clients avoid, and it isn’t so much of a feature as a red flag to look out for.

HDFC Ergo’s Optima Lite takes the win in this category, too, since the policy has no disease-wise sub-limits.

- Room Rent Restrictions: Here is something that you might not know about room rent restrictions - in case you exceed the room rent limit as mentioned in your policy documents, you end up paying a pro-rata-based share of the total medical bill. This unexpected spending might take a severe and surprising toll on your savings. Thus, the best health insurance plans in the industry have no room rent restrictions.

However, in the case of HDFC Ergo Optima Lite, there are two types of room rent restrictions -

- 1% of the sum insured in the case of normal rooms

- 2% of the sum insured in the case of ICU beds

This should be a major concern for any potential policyholder that might lead them to avail of any other comprehensive health insurance plan.

- AYUSH coverage: While the streamlined medications and treatment procedures offer almost instant relief and comfort, at times, the long-time reliability of such methods and medicines may have a dire impact on one’s health. This has led to multiple individuals turning to unconventional and nature-based treatments and medicines. Now, while these treatments may require comparitively lower charges, there is still a consistent expense that would require you to pay out of your pocket. Hence, with the best health insurance plans, there is an option for AYUSH coverage without any caps.

HDFC Ergo Optima Lite offers coverage for AYUSH-based treatments without sub-limits (up to the sum insured).

- Daycare and Domiciliary Coverage: When it comes to health insurance plans, even the most basic ones now offer coverage for daycare procedures and domiciliary treatments. This indicates offering funds for

- Treatments and procedures that require less than 24 hours of hospitalisation (think cataract surgery, dialysis, etc.)

- Medical care/procedures carried out at home due to the shortage of hospital beds/ mobility issues of the patient.

HDFC Ergo Optima Lite offers daycare coverage and domiciliary coverage up to the sum insured of the base plan.

- Waiting Period: In the case of health insurance plans, there are 4 types of waiting periods -

- Initial waiting period (usually 30 days)

- Pre-existing waiting period (ranges from 1 year to 3 years)

- Specific Illness waiting period (usually of 2 years)

- Maternity waiting period (ranges from 9 months to 4 years)

As common knowledge goes, the lower the waiting period, the better the plan is for the policyholder. This span indicates the number of months the insured has to wait out before they can avail of the coverage for the specific condition.

In the case of HDFC Ergo Optima Lite, the waiting period is pretty close to being “great.”

- The initial waiting period is 30 days,

- The pre-existing ailment waiting period is 36 months (24 months could have been better, of course)

- The specific illness waiting period is 24 months.

- Restoration Perks: Refilling the sum insured as it gets utilised over claims across a single year is a perk that no health insurance policyholder should miss out on. The ideal restoration feature should include - unlimited restoration upon partial exhaustion for both the same and different ailments.

In the case of HDFC Ergo Optima Lite, the restoration feature ticks all the boxes by offering unlimited options for the same and different illnesses.

- Daily Cash for shared room: Under the HDFC Ergo Optima Lite policy, if the insured stays in a shared room in a network hospital and the hospitalisation surpasses 48 hours, the insurer offers a daily cash of ₹800 (capped at ₹4800). However, this cash is offered on a reimbursement basis.

- e-Opinion: In case the insured is diagnosed with any of the listed critical ailments (in the policy document), the insurer offers you the perk of getting an e-Opinion once in a policy year. This e-Opinion is supposed to aid you in making an informed decision about your medical treatments.

- Preventive Health CheckUp: In the case of top-notch health insurance policies, insurers offer a free preventive health insurance checkup (up to a specified limit) once/year. This feature ensures that the insured stays aware and conscious about any medical conditions that have crept up over the year and remain one step ahead with an early diagnosis and treatment.

HDFC Ergo Optima Lite offers free preventive health check-ups once a year. The limit is specified as follows -

| Type of Policy | Base Coverage | Preventive Health CheckUp Coverage |

|---|---|---|

| Individual Plan | ₹5 lakhs and ₹7.5 lakhs | ₹1500 |

| Family Plan | ₹5 lakhs and ₹7.5 lakhs | ₹2500 |

- Cumulative Bonus: Irrespective of whether you make claims, you can acquire a cumulative bonus of 10% up to a maximum of 100%. Unfortunately, HDFC Ergo Optima Lite’s nominal cumulative bonus isn’t encouraging, especially when its competitors offer bonuses of up to 500%.

- Pre and Post-Hospitalisation Coverage: Much like any of the health insurance policies in the industry, HDFC Ergo Optima Lite too offers coverage for pre and post-hospitalisation expenses. Now, this is a basic feature that ensures that the insured’s post-follow-up procedure and pre-procedure diagnostics, etc. are well-funded. And even then, Optima Lite fails to offer the industry standards - the policy only provides coverage of 30 days (pre-hospitalisation) and 60 days (post-hospitalisation), much less than what top-notch or even average health insurance plans offer.

- Add-Ons: Apart from the basic features that HDFC Ergo Optima Lite offers, a handful of add-ons lend some degree of customisation. However, please remember that these add-ons require an additional amount that is included over and above your premium. Also, not every health insurance add-on is worth purchasing. So, before you purchase an add-on, make sure that the affordability perk of Optima Lite doesn’t go out of the window and that the rider caters to your medical and financial requirements.

- Protect Benefit: Under this rider, you get coverage for non-medical expenses and consumables (medical supplies and items used during a hospital stay or medical procedure). This is a great rider to have with your base policy in case you opt to purchase the HDFC Ergo Optima Lite plan, considering that such expenses contribute to about 5-15% of the medical bill.

- Plus Benefit: This coverage doubles your sum insured after 2 years. The bonus ranges from 50% to 100% and is unaffected by claims. This might be a value-adding health insurance add-on to have if you consider the low coverage (₹5 lakhs and ₹7.5 lakhs only) that the plan offers. The bonus might just be the affordable way out to boost your sum insured to the amount that you ideally need.

- Aggregate Deductible: Under this add-on, the insurer offers aggregate deductible options of ₹10k/₹25k/₹50k, offering premium discounts of up to 40%. The rider can help reduce your premiums further. However, you might want to rethink the decision about purchasing this rider, considering the deductible that you will be paying and the additional premium that you would need to pay on account of the add-on.

| To Note - Zonal Restrictions for accessibility |

|---|

| One of the striking issues with the HDFC Ergo Optima Lite plan is its restrictions in terms of availability - the policy is only available in Tier 2 and Tier 3 cities and not in Tier 1 cities. While this justifies HDFC Ergo being able to launch their rare affordability USP in their plans (Tier 2 and Tier 3 cities incur lower medical costs as compared to Tier 1 places), it also severely restricts the target audience. |

| Also, this restriction sheds light on why and how the sum insured offered by Optima Lite might fall substantially short if you seek specialists for advanced treatments from a Tier 1 city. |

Now, coming to the question of whether you should buy an HDFC Ergo Optima Lite policy, we have a quick comparison between HDFC Ergo’s flagship plan, Optima Secure vs Optima Lite. Take a look and decide for yourself!

HDFC Ergo Optima Secure vs HDFC Ergo Optima Lite

| Features | Optima Secure | Optima Lite |

|---|---|---|

| Base Sum Insured | ₹5 lakhs - ₹2 crores | ₹5 lakhs and ₹7.5 Lakhs only |

| Hospitalisation Expenses | 100% up to the sum insured | 100% up to the sum insured |

| Waiting Periods | Initial - 30 days Specified Illnesses - 24 months PEDs - 36 months |

Initial - 30 days Specified Illnesses - 24 months PEDs - 36 months |

| Room Rent | At Actuals | Room: 1% ICU: 2% |

| Pre-Hospitalization | 60 Days | 30 Days |

| Post-Hospitalization | 180 Days | 60 Days |

| Day Care & AYUSH Treatments |

Covered up to the sum insured | Covered up to the sum insured |

| Domiciliary Treatment and Hospitalization at Home | Covered up to the sum insured | Covered up to the sum insured |

| Organ Donor Expenses | Covered up to the sum insured | Covered up to the sum insured |

| Preventive Health Check-up | Covered (up to specified limits) | Covered (up to specified limits) |

| Daily Cash for Choosing Shared Room | ₹800 per day, max up to ₹4800 | ₹800 per day, max up to ₹4800 |

| Automatic Restore Benefit | Once a year for the same & different illnesses (add-on available to make it unlimited) |

Unlimited times for both the same & different illnesses |

| Plus Benefit (Cumulative Bonus) | +50% per year up to max 100% (Irrespective of claims) | +10% per year; max up to 100% (Irrespective of claims) & (+50% per year; max 100% - Optional) |

| E Opinion for Critical Illness | Once per year | Once per year |

| Emergency Air Ambulance | Up to ₹5 lakhs | Up to ₹5 lakhs |

| Secure Benefit (2 X cover from Day 1) | Included | NA |

| Protect Benefit | Included | Can be covered via an Optional add-on |

| Aggregate Deductible options(Optional) | ₹25k - ₹5 lakhs | ₹10k - ₹50k |

| PED wait period modification (Optional add-on) | PED WP can be reduced to 1 or 2 years from 3 years. (Not Live Yet) | PED WP can be reduced to 1 or 2 years from 3 years. (Not Live Yet) |

Here is a quick look at the approximate base premiums for both policies -

| ₹5 Lakhs sum insured TIER 2 city (Age of the policyholder) |

HDFC Ergo Optima Secure | HDFC Ergo Optima LITE |

|---|---|---|

| 30 years old | ₹11,378 | ₹9,511 |

| 40 years old | ₹12,779 | ₹10,683 |

| 50 years old | ₹20,066 | ₹16,773 |

One look at the two tables above and you can arrive at this conclusion -

While the difference in premium is nominal (a couple of thousand), HDFC Ergo Optima Lite ends up with many compromised features and restrictions compared to Optima Secure. Moreover, the covergae and customisation option too is not great with Optima Lite.

So, if you are wondering about getting Optima Lite, take a look at Optima Secure instead. You will end up with a plan with a higher range of coverage that you can boost later on to meet your evolving requirements, no room rent restrictions, multiple add-ons, and more - in a nutshell, a comprehensive health insurance plan.

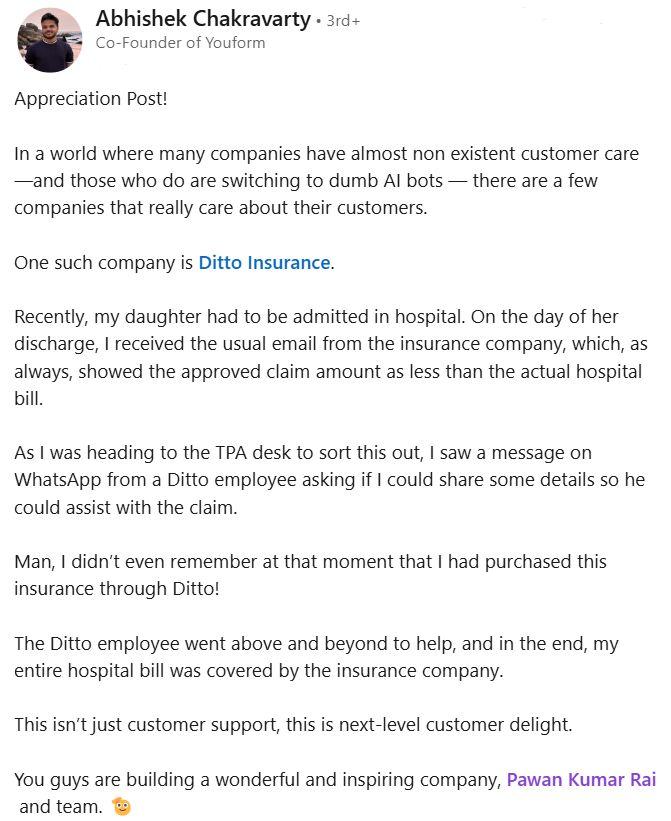

Why Talk to Ditto for Your Health Insurance?

At Ditto, we’ve assisted over 3,00,000 customers with choosing the right insurance policy. Why customers like Abhishek below love us:

✅No-Spam & No Salesmen

✅Rated 4.9/5 on Google Reviews by 5,000+ happy customers

✅Backed by Zerodha

✅100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now!

What’s Unique About HDFC ERGO Optima Lite?

HDFC Ergo Optima Lite offers no special/unique features. The policy instead compromises the basic offerings. The only thing exceptional about the policy is its limited availability across Tier 2 and Tier 3 cities only.

Last updated on: