In the past, the standard financial practice was to offer a term insurance plan to the earning member of the family. The concept was still a bit biased, wherein life insurance providers considered that only earning members of a household required an income replacement in the case of their unfortunate death to safeguard the family’s future financial life goals!

However, over the years, insurers soon became open to the idea that homemakers, too, make a significant contribution to a family’s financial growth, even if it is indirect. Housewives may even host a small business on the side or guide the dependent children of the family to become financially independent. Such financial contributions couldn’t be ignored when calculating a family’s annual/monthly financial earnings.

Moreover, while it was great to have the option to choose one’s children as dependents, there was a consistent concern for a spouse - what happens to the other spouse when they pass away? Under such circumstances, a lot would ride on the child’s sense of responsibility towards the living parent, and their spouse won’t have a penny to strengthen their financial standpoint.

This brings us to the introduction and concept of term insurance plans for couples. Across this blog, we will explain in detail term insurance policies for couples—what they are, what their significance is, what conditions and clauses are involved, what the best term insurance plans offer this perk, and whether you should opt for such plans at all.

Best Term Insurance Providers For Couples

| Best Term Insurance Providers | Best Term Insurance Plans Offered |

|---|---|

| HDFC Life | Click2Protect Super | Click2Protect Life |

| Max Life | Smart Secure Plus |

What are Term Insurance Plans For Couples?

Term insurance plans, on a standard basis, cover only individuals. However, term insurance plans for couples are what the phrase suggests - term insurance policies with two policyholders: 2 spouses - a primary and a secondary policyholder.

Now, if you have read our term insurance policy eligibility details (if you haven’t, we suggest you read it now), you know that income is a significant eligibility criterion that is factored in while deciding whether you can purchase a term insurance plan and the sum assured that would be assigned to you. Based on this, for term insurance for couples, we have two scenarios -

CASE 1: What if 1 spouse has an active occupation and the other spouse is a housewife?

Now, the top 3 term insurance providers in the market - HDFC Life, ICICI Prudential, and Max Life all offer plans to home-makers with no direct earnings of their own.

While the eligibility factors, payouts, rider availability, and sum assured may vary from insurer to insurer, one particular consideration is common for all—in the case of housewives, the husband's income is taken into account as an eligibility factor.

Heads Up: It takes an average person up to 5 hours to read & analyze a policy, and 10 hours or more to compare different plans and make a decision.

This is why we propose a better alternative - taking a 30-minute FREE consultation with Ditto’s certified advisors. We have a spam-free guarantee, and we’ll never push you to buy a plan. Don’t delay this - we have limited slots every day, so book a quick call here before they run out.

CASE 2: What if both spouses have active occupations?

In this case, since both policyholders are financially independent, the insurer will consider both the income amount and offer you a suitable sum assured. However, in this case, since both the potential policyholders are earning (thereby meeting the eligibility criteria individually), the usual recommendation is that you choose two individual plans instead of opting for a joint term insurance plan. If you want to know why, read on!

Should You Opt for Term Insurance Plans For Couples?

- PROS: The only pro of joint-term insurance plans is the affordability of the premiums. Here’s an idea - imagine taking a term insurance plan for 30 years for a ₹1 crore cover as an individual vs opting for a term insurance policy for 30 years for ₹1.5 crore as a couple. The premium difference would be the required edge that convinces you to take a term insurance plan for couples.

However, before you go ahead with this choice, we would recommend that you do either or both of these -

- Approach an expert and discuss the details to gain their opinion

- Use free calculators to calculate the ideal term cover for you both, and then use a free comparison tool to determine the term insurance policy that would suit your current financial bandwidth and future financial goals.

2. CONS: Term insurance plans for couples are only called into question in the case of spouses. This is a similar condition to that of a joint savings account in any reputed bank. Usually, you opt for joint accounts to secure the financial future of your partner in the event of your unfortunate absence. However, in the case of term insurance, what you must factor in are the tax perks and the premiums.

- Term insurance plans usually offer you tax savings under Section 80C and 10(10D). So, naturally, two-term insurance plans amount to two sets of tax savings on your premiums.

- Moreover, in the case of term insurance plans, some insurers offer reduced premiums to female policyholders. Under such cases, this might be a beneficial perk to have. However, you would need to verify if you are getting this financial edge and if its worth the pain of managing two different policies, renewing them, choosing the perfect riders, etc.

- Joint-term insurance plans often limit your cover amount and bring in multiple restrictions to the already stringent eligibility criteria. You might want to check out your eligibility for a term insurance plan for couples in advance.

What are the Things to Remember When Purchasing Term Insurance Plans For Couples?

As mentioned before, each term insurance provider has a different set of bells and whistles when it comes to eligibility criteria and features offered for such plans for couples. Take a look at these clauses -

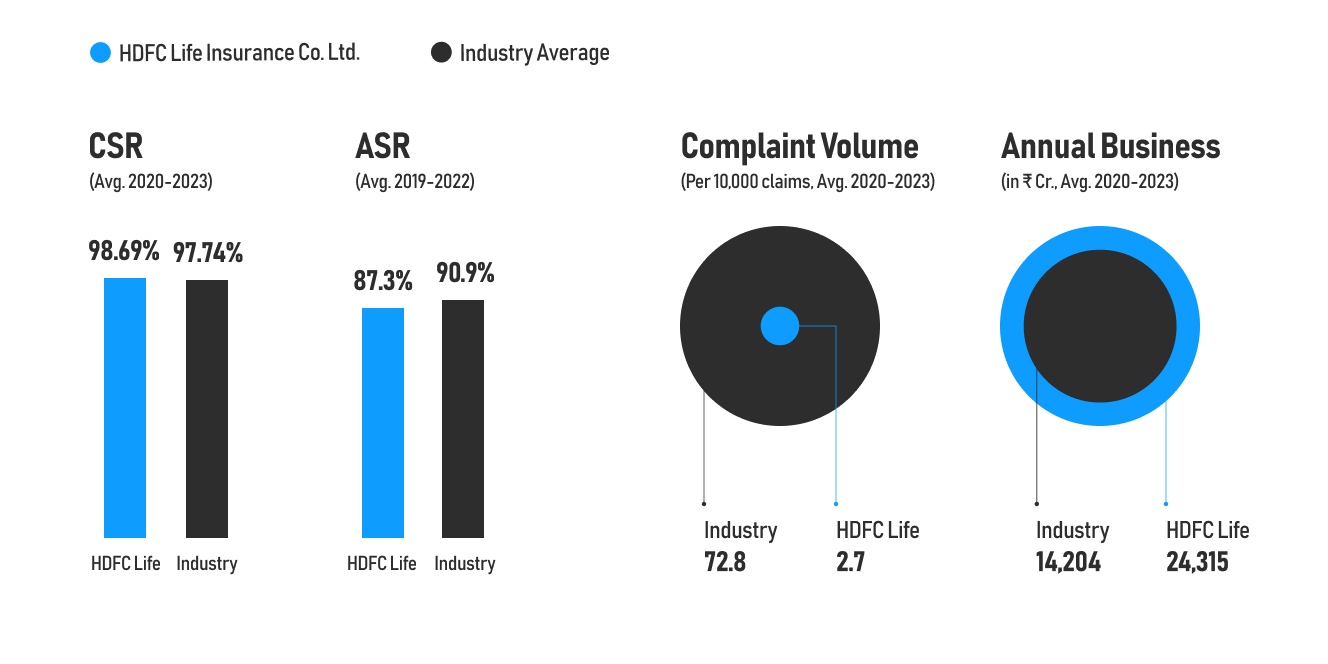

- HDFC Life: HDFC Life is one of the best term insurance providers in the market. The insurer has excellent data across the metrics used to determine a provider’s credibility -

Thus, HDFC Life is undoubtedly a great pick as your term insurance provider. Now, if you plan to purchase a term insurance plan for couples from HDFC Life, here’s what you need to remember:

- The age difference between the primary insured and the spouse should be a maximum of 10 years.

- The spouse must be a graduate and can't have more than ₹1 crore as a life cover option.

- No riders are available with a joint-term insurance plan from this insurer.

- If the primary insured dies first, the sum insured of his plan will be paid out to his/her beneficiary, and the spouse’s cover will actively start, with the sum assured equal to 50% of the primary policyholder’s cover.

- If the spouse dies first then no sum assured will be paid. The primary insured will just continue with their cover amount.

- Tax benefits will go to the primary insured individual.

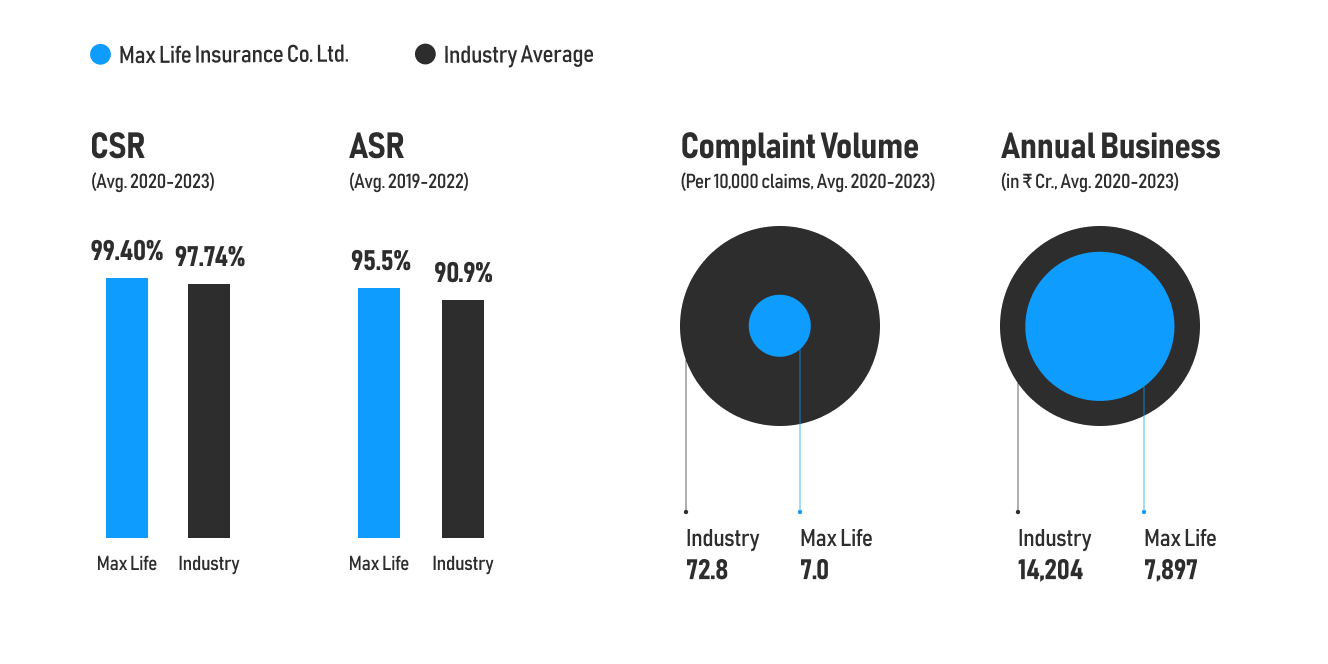

2. Max Life: Max Life is one of the best picks for term insurance plans. Much of this popularity can be attributed to the affordability of the plans and the wide range of plan options and variants across its policies. Additionally, the insurer establishes its credibility with excellent numbers across its metrics -

So, if you are planning to opt for a term insurance plan for couples from this insurer, here’s what you need to remember -

- The maximum cover is capped at ₹50 lakhs.

- You will need to provide your standard physical medical examination reports.

- If the secondary policyholder dies before the primary insured, a payout of ₹10 lakhs will be given. On the other hand, if the primary policyholder passes away first, the beneficiary receives ₹50 lakhs.

- A minimum income eligibility of ₹5 lakhs is a mandate.

Why Talk to Ditto for Your Health Insurance?

At Ditto, we’ve assisted over 3,00,000 customers with choosing the right insurance policy. Why customers like Srinivas below love us:

✅No-Spam & No Salesmen

✅Rated 4.9/5 on Google Reviews by 5,000+ happy customers

✅Backed by Zerodha

✅100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now!

Why Talk to Ditto for Your Health Insurance?

At Ditto, we’ve assisted over 3,00,000 customers with choosing the right insurance policy. Why customers like Srinivas below love us:

✅No-Spam & No Salesmen

✅Rated 4.9/5 on Google Reviews by 5,000+ happy customers

✅Backed by Zerodha

✅100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now!

Conclusion

Term insurance plans for couples are a unique offering that is only offered by a few insurers as of now. While these policies surely can be an option if you wish to cover your spouse and are finding it difficult to find a plan for them, there are quite a few cons that you need to weigh out before the purchase. Also, please remember that insurers offer separate term insurance plans for housewives.

While multiple policies can be a bit cumbersome to maintain, you may want to rethink from the perspective of tax deductions, rider availabilities, restrictions on coverage and other features, etc. Also, if you opt for two separate plans, one for you and the other for a homemaker, you can add one more top-notch term insurer to the mix of your options: ICICI Prudential (it doesn’t offer joint term insurance plans yet).