Overview

India’s insurance market today is packed with options, from digital-first insurers to more transparent products. According to IRDAI Annual Report (FY 2024-25), India’s overall insurance penetration stands at 3.7%, with life insurance at 2.7% and non-life insurance at 1%.

At the same time, more households are becoming aware of how insurance can protect their family’s future against unexpected risks. This is where one common question comes in: term insurance vs life insurance. Should you choose a simple, affordable term plan that offers a large safety net? Or should you pick a broader life insurance product that combines protection with savings or investment?

This guide breaks down term insurance vs life insurance so you know what you are comparing. Let’s dive in.

What Is Term Insurance?

Term insurance is a pure protection plan. You pay a fixed premium for a defined period, usually 20, 30, or 40 years. If you pass away during that period, your nominee receives the sum assured as a lump sum. If you outlive the policy, the coverage simply ends, and nothing is paid out.

A ₹1 crore term cover for a healthy 30-year-old typically costs ₹10,000 to ₹12,000 per year.

Key features of term insurance include:

- High Cover at Low Premiums: Often the cheapest way to get ₹50 lakh–₹5 crore of protection, depending on underwriting.

- Fixed Tenure: Typically 20 to 40 years or cover till age 85 (sometimes 99).

- No Investment Element: Premiums only pay for risk coverage.

- Clear Claim Triggers: Death and, in some plans, terminal illness.

- Tax Benefits: Premiums paid may qualify under Section 80C (old regime), and death benefits are tax-free under Section 10(10D) for the nominees.

For a more comprehensive understanding, refer to our guide on how term insurance works.

Talk to an expert

today and

find

the right

insurance for you.

Types of Term Insurance

Key Insights:

- We recommend level term insurance as the default option because it provides a fixed, high cover at an affordable premium throughout the policy term.

- Increasing cover, zero cost exit, and housewife term plans can be considered only when they fit a specific need or profile.

- We don’t generally recommend return of premium, decreasing term insurance, or whole life term insurance because they either cost much more, reduce coverage over time, or extend coverage beyond the years when your family actually depends on your income.

- Group term and joint term insurance should not be your primary protection plan because employer or bank-linked covers can end anytime, and joint covers may have payout limitations. Separate individual term plans usually offer cleaner and more reliable protection.

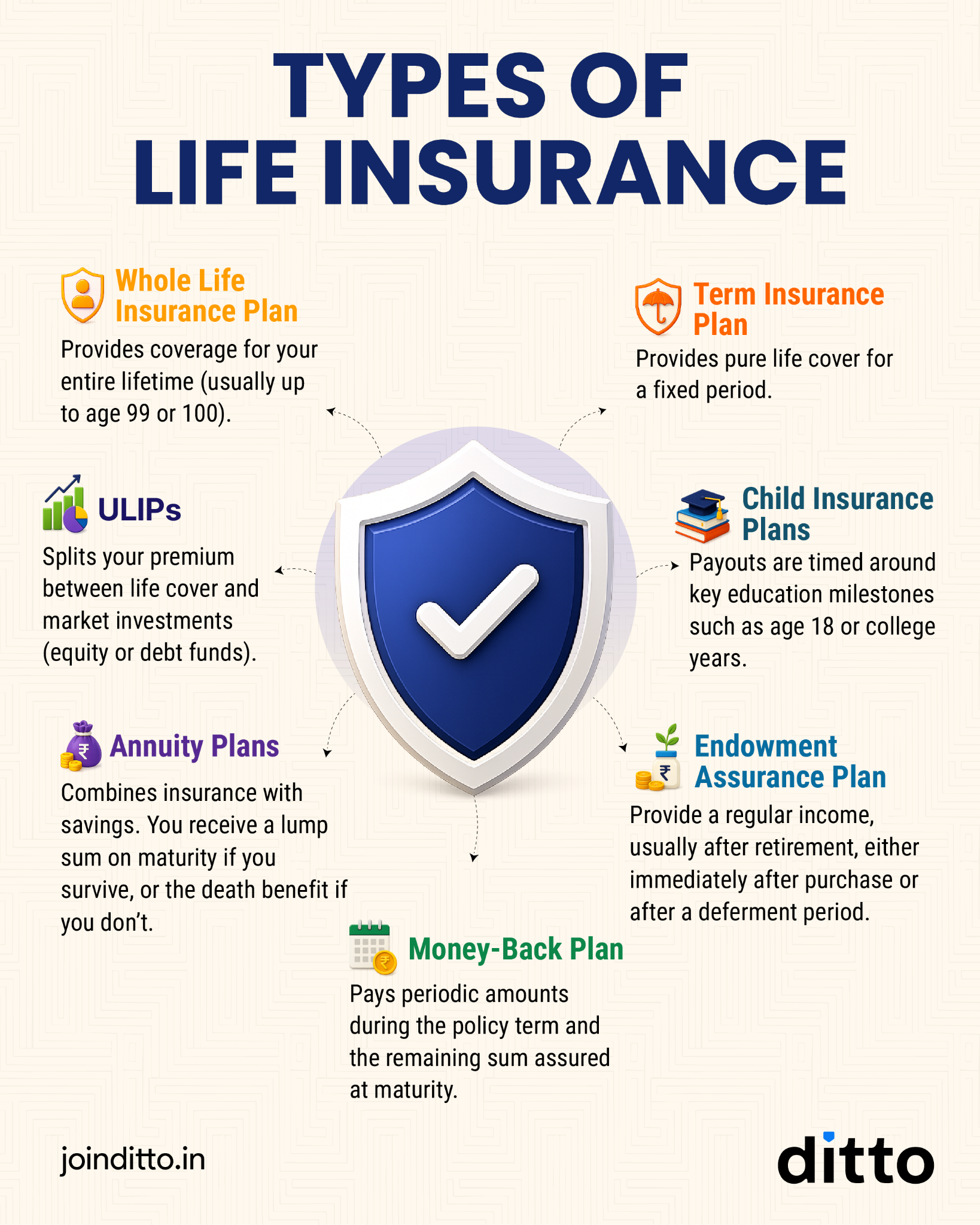

What Is Life Insurance?

Life insurance refers to a broad category of policies that provide a payout upon death and, in many cases, also offer savings or investment benefits upon survival or maturity.

In simple terms, life insurance is a contract where the insurer promises to pay a fixed amount if the insured person dies during the policy term. In some plans, the insured also receives a maturity benefit if they survive the term.

In the official IRDAI’s master circular, life insurance products are usually classified using categories such as linked or non-linked, participating or non-participating, individual or group, and savings or pure-risk products.

For easier understanding, however, life insurance products can be grouped into two broad buckets:

- Pure Protection Plans: They cover only the risk of death (e.g., term insurance).

- Protection‑Plus‑Savings: These plans combine life cover with returns or investments (e.g., endowment, money‑back, ULIPs, and whole‑life policies).

This structural difference is at the heart of the life insurance vs term insurance debate. Life insurance policies are built around a few core elements:

- Life Assured/Policyholder: The person who buys the policy and pays the premiums

- Nominee: The person who receives the benefit on death (usually spouse, children, or parents)

- Sum Assured: The guaranteed payout amount on death/maturity

- Policy Term: Duration of coverage

- Premium: Amount paid to keep the policy active

- Death Benefit: Payout if death occurs during the term

- Maturity Benefit: Payout on survival (if applicable)

- Surrender/Paid‑up value: Amount received or reduced cover if premiums are discontinued in savings‑based plans

For more information, read our guide on the features of life insurance.

Types of Life Insurance

Term Insurance vs Life Insurance: Side-by-Side Comparison

Note: Here, ROP refers to return of premium, and TROP denotes term plan with return of premium.

Premium Comparison

Term vs TROP Premiums

The premiums considered are for HDFC Life Click 2 Protect Supreme Plus (term plan) and its return of premium version (second year onwards). The illustration is for a 30-year-old male seeking a ₹1 crore cover up to 65 years.

Here, you can clearly see that the premiums for the TROP are almost 125% higher than those of the pure term plan.

Endowment Plan Premiums

The following illustrative premiums are calculated for a healthy male aged 30 years (50 years for the life-long income option), who pays ₹1 lakh per annum and survives the policy term under the HDFC Life Sanchay Plus plan.

Here, PA stands for per annum.

ULIP Premiums

These illustrative premiums are for a 30-year-old individual seeking a cover of ₹20 lakhs for 30 years under the HDFC Life Sampoorn Nivesh Plus plan.

The math here matters. If you buy term insurance and separately invest the premium difference in mutual funds, you end up with far greater insurance coverage, far greater investment wealth, and better liquidity.

Ditto’s Expert Insights on Term Insurance vs Life Insurance in India

Shrehith, our co-founder, says that term insurance is more important than other types of life insurance. According to him, the idea is simple:

“Insurance should primarily be about protection, not investment. That’s the problem with many other life insurance products. They mix insurance with savings or investments, but often don’t offer enough returns or enough protection.

This is where term insurance has a clear advantage. It keeps things clean: you pay a low premium and get a high life cover, ensuring your family has strong financial protection if something happens to you.”

How to Choose the Right Cover Amount in Life and Term Insurance?

There’s no fixed term cover that works for everyone. The right term insurance cover depends on your income, expenses, goals, and liabilities.

At Ditto, we use the expense and liabilities replacement method to estimate the term cover you require. To get a better understanding, use our term insurance calculator to find the ideal amount for you.

Here’s how the calculator works:

- Input Essentials: Enter your age, income, existing liabilities, number of dependents, and ongoing necessary expenses (exclude luxuries).

- Adjust for Inflation: The calculator factors in rising costs over time, ensuring your coverage keeps pace with future needs.

- Consider Life Changes: Update the calculator for major events such as marriage, children, or new loans, which may increase the required sum assured.

Note: If you opt for higher coverage, insurers conduct stricter financial and medical underwriting. At Ditto, we recommend not skipping any test. Even if your policy application is declined, early clarity helps you plan and avoid future complications.

If you already have an existing life insurance cover, you may deduct that amount from the recommended coverage. This helps ensure you’re adequately insured without over-insuring or paying unnecessary excess premiums.

Refer to our guide on life insurance coverage in India for more details.

How to Choose Between Term and Life Insurance?

There is no universal answer, but there is a framework that works for most people.

Choose Term Insurance If

- You have dependents who rely on your income: a spouse, children, or aging parents.

- You have outstanding liabilities, such as a home loan.

- You want the maximum possible cover at the lowest possible premium.

- You are under 45, healthy, and buying early to lock in low rates.

- You are disciplined enough to invest the premium difference separately.

Consider Traditional Life Insurance Only If

- You are extremely risk-averse and will not invest the premium difference yourself.

- You are in a high net worth bracket and need a whole life plan specifically for estate planning or liquidity for heirs.

- You want a small forced savings mechanism alongside a term plan, not instead of one.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Ditto's Verdict on Term Insurance vs Life Insurance

At Ditto, we recommend pure term insurance as the most efficient choice in the term insurance vs life insurance debate. It offers a large cover at a low premium because it does not mix protection with investment. You can also refer to our guide on the best term insurance plans in India to find the right pick for you.

Traditional plans like endowment, money-back, or ULIPs usually offer lower cover, higher costs, modest returns, and long lock-ins. For most people, it’s smarter to keep both goals separate: use term insurance for protection and options such as mutual funds, the Public Provident Fund (PPF), or Fixed Deposits (FDs) for wealth creation.

Full Disclosure

Frequently Asked Questions

Customer Reviews

Last updated on: