Life insurance is like marriage. It is a long-term commitment. And once you purchase it, it is recommended that you stick to the same plan. In fact, according to research from our experts, it is estimated that over 70% of people who purchase a life insurance plan stick with it and do not cancel it within the first year. However, your financial situation might change sooner than you expect. Maybe you bought a policy under pressure and now realize it doesn’t align with your needs. Or perhaps you’ve found a better plan elsewhere or no longer see value in holding the policy. Whatever your reason, one question usually comes up: Can you cancel your life insurance policy and get your money back?

Well, the answer depends on what type of policy you’ve purchased and when you choose to cancel it. Let’s walk through the different scenarios so you know exactly what to expect, whether it’s a pure term insurance plan or a savings-based policy like an endowment or ULIP.

Heads Up: It takes an average person up to 5 hours to read & analyze a policy, and 10 hours or more to compare different plans and make a decision.

This is why we propose a better alternative - taking a FREE consultation with Ditto’s certified advisors. We have a spam-free guarantee, and we’ll never push you to buy a plan. Don’t delay this - we have limited slots every day, so book a quick call here before they run out.

Can you get a full refund of your premiums for your life insurance plan?

The short answer: Yes. Every life insurance policy comes with a free-look period, usually 30 days from the date you receive the policy document. During this window, you’re allowed to cancel the plan for any reason at all, maybe you didn’t understand the terms, or you simply changed your mind.

If you cancel during this period, you’re entitled to a full refund of your premium, although the insurer may deduct a few nominal charges. These can include medical examination costs (if any), stamp duty, and proportionate risk premium for the days the policy was active.

This rule applies across both term insurance policies and other life insurance policies, such as ULIPs or endowments. However, once the free-look period lapses, things become more complicated, and in most cases, you won’t be eligible for a full refund anymore.

Cancel within the free-look period, and you’ll get most of your premium back, minus minor deductions.

Cancelling a Life Insurance Policy After Free-Look Period

Once the free-look period is over, term insurance policies, especially those that offer pure protection without any return, do not provide any monetary payout upon cancellation.

You can stop paying premiums anytime, and the policy will simply lapse. But since there’s no savings or investment component involved, you won’t get any of your money back. This is true regardless of how long you've held the policy or how much you’ve paid in premiums.

It’s similar to letting your car insurance expire; you lose coverage, and the premiums you’ve already paid don’t return to you. So if you’re thinking of cancelling because you’ve found a better term plan, consider applying for the new one before you stop the current policy to avoid a coverage gap.

However, there are exceptions. If you've opted for a Return of Premium (ROP) plan, a limited pay option, or a zero-cost term plan, there may be a surrender value built into the contract. That means you could get some or all of your money back if you cancel under the right conditions. These cases work differently, and we’ve broken them down in this article to help you understand exactly how much you can recover and when.

Cancel a term policy after the free-look period, and you won’t get a refund, but you will lose your coverage.

Cancelling Traditional Life Insurance or ULIPs

If you’ve bought a traditional life insurance plan like an endowment or money-back policy, or a ULIP (Unit Linked Insurance Plan), the story changes a bit. These policies accumulate a surrender value over time. But that doesn’t mean you can walk away with your full premium anytime you want.

Here’s how it usually works:

- If you try to surrender the policy within the first three years, you typically get nothing back (or a very small amount). These plans may have a lock-in period during which no surrender value is payable.

- If you surrender after three to five years, your insurer may return a portion of the premiums, but this is usually much lower than what you’ve paid. Various charges, such as policy administration, premium allocation, and surrender charges, are deducted.

- For ULIPs, the value you receive depends on the Net Asset Value (NAV) of the fund and how long you’ve stayed invested. ULIPs come with a mandatory five-year lock-in, and if you cancel before this, your money is moved to a discontinued fund (earning minimum returns), and you’ll only receive it after five years.

Cancelling a ULIP or traditional policy can lead to financial loss, especially if done within the lock-in period.

What is Surrender Value in Life Insurance, and When Do You Get It?

The surrender value is what you receive if you exit your life insurance policy before maturity. It's most relevant for endowment plans, money-back policies, and ULIPs.

There are typically three kinds of surrender values:

- Guaranteed Surrender Value: A fixed percentage of total premiums paid, applicable after a minimum number of years.

- Special Surrender Value: Calculated based on factors like bonuses, number of premiums paid, and policy term, usually higher than the guaranteed value.

- Cash Surrender Value: The actual payout you get, which may include bonuses or market-linked gains in the case of ULIPs.

The longer you keep paying premiums and stay invested, the higher your surrender value becomes. But even at its peak, it’s rarely equal to the total premiums you’ve paid, especially after accounting for policy charges.

Surrender value builds over time, but you’re unlikely to recover your full investment unless you stay till maturity.

Impact of Cancelling Your Life Insurance Plan

Cancelling your life insurance can leave you without protection. If the cancelled policy was your family’s financial safety net, you could expose them to serious risk unless you replace it with an alternative.

Moreover, cancelling savings-linked plans often means locking in a financial loss. You may have paid premiums for years, only to get a fraction of that back.

Before pulling the plug, ask yourself:

- Are you switching to a better, more affordable plan, such as term insurance?

- Have your financial responsibilities reduced significantly?

- Will the loss in surrender value be offset by gains elsewhere?

If you’re just reacting to premium fatigue or short-term financial pressure, consider whether temporary solutions, like pausing your premiums, can help.

A cancellation decision should align with your financial goals and leave no gap in protection.

Alternatives to Cancelling Your Life Insurance Policy in 2025

Before you cancel your life insurance, it’s worth exploring a few middle-ground options that can limit your losses and maintain some benefits.

1) If you have a ULIP or Endowment plan, switch to a term plan:

If your current policy is a ULIP or endowment and you no longer need the savings feature, consider replacing it with a low-cost term plan. However, ensure the new plan is active before canceling the old one.

2) Convert to a Paid-Up or Reduced Paid-Up Policy

For investment-linked plans (like endowment or ULIPs), cancelling the policy outright may cause you to lose a substantial portion of your invested money. Instead, you can convert the plan into a paid-up or reduced paid-up policy. This means you stop paying future premiums, but the plan continues with a proportionately reduced benefit. So if you’ve already paid, say, 50% of your total premiums, the final maturity or death benefit will also reduce to around 50% of the original amount. Still, at least you don’t walk away with nothing.

3) Continuation Benefit

Most of the term insurance plans we recommend at Ditto have a continuation benefit, which allows you to skip paying premiums for a year without affecting the policy's active status. So, if you temporarily can’t pay the premiums, you can always use this feature. And pay the premiums the following year (for both years).

4) If your policy is lapsed:

Some insurers allow you to revive a lapsed policy within a limited period of 5 years. Revival will entail paying back the backlog of premiums, penalties, and fresh underwriting.

You may not need to cancel; you can pause paying the premiums and pay them during the next renewal, or switch to a term policy, which can preserve value and protection.

How to Cancel Your Life Insurance Policy

If you’ve decided to go ahead with cancellation, the process is usually straightforward:

- Visit your insurer’s branch or log in to your online account.

- Submit a written cancellation request with your policy number and personal details.

- Complete KYC requirements and fill out refund or surrender forms, if applicable.

- Receive an acknowledgment from the insurer.

- Wait for confirmation and refund, which typically takes 7–10 working days if you’re eligible.

Keep a copy of the request and acknowledgment for your records. If your policy has any cash value, make sure you clarify the final payout amount before proceeding.

Cancelling is easy, but always check eligibility for refunds and keep records of the entire process.

Tax Implications of Cancelling Life Insurance in 2025

Taxes are often overlooked when cancelling a policy, but they can make a noticeable dent in your returns or savings:

- If you’ve claimed Section 80C deductions under the old tax regime on premiums in earlier years and then canceled the policy within 2 years, those tax benefits can be reversed.

- In the case of ULIPs, surrendering before 5 years can make the entire withdrawal taxable as income in your hands under section 10(10D) of the Income Tax Act.

- Even if you cancel within the free-look period, any refund received could be subject to tax if the policy was employer-funded or structured through a salary package.

Cancelling your policy early can lead to tax setbacks, especially under Section 80C and 10(10D).

Note: Please double-check with your Chartered Accountant or your financial adviser for any aspect related to taxes.

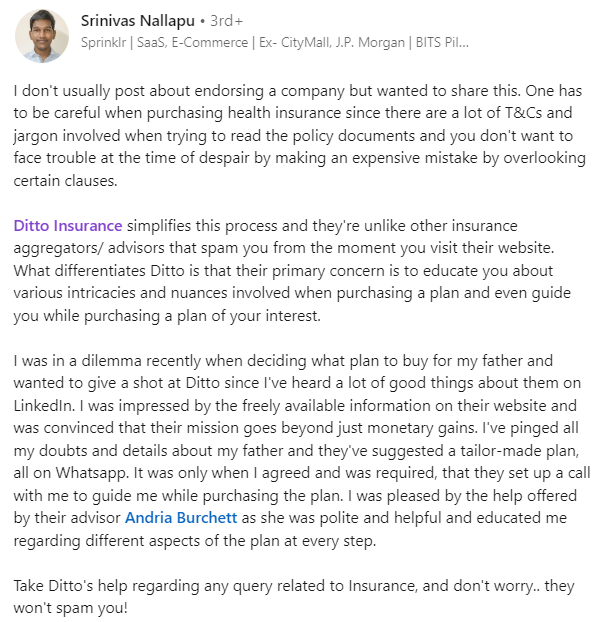

Why Talk to Ditto for Your Health Insurance?

At Ditto, we’ve assisted over 3,00,000 customers with choosing the right insurance policy. Why customers like Srinivas below love us:

✅No-Spam & No Salesmen

✅Rated 4.9/5 on Google Reviews by 5,000+ happy customers

✅Backed by Zerodha

✅100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now!

Conclusion: Should You Cancel Your Life Insurance Policy?

Cancelling a life insurance policy isn’t as simple as walking away, especially if you’ve held it for a while or built up value. The financial and protection consequences can be long-lasting, so it’s important to take a step back and evaluate the whole picture.

Here’s a quick guide to help you decide:

- Term Insurance: If you have a standard term policy, cancelling it after the free-look period won’t fetch you a refund unless it's a zero-cost or return of premium (ROP) plan. If you’re considering ending it due to affordability, explore options like continuation benefits or switching to a lower-coverage plan.

- Savings-Based Plans (ULIPs/Endowments): Don’t rush to cancel. Always check the surrender value first and consider converting the plan to reduced paid-up to avoid losing everything you've invested. Remember, early exits can lead to significant losses and tax implications.

- Still Unsure? Talk to an Expert: Cancellation should never be a knee-jerk reaction to short-term discomfort. If your needs have changed or you're confused about your options, a short call with a certified advisor can save you time, money, and regret.

At the end of the day, cancelling life insurance should never be a knee-jerk decision. Always evaluate the financial and protection impact, and when in doubt, speak to a certified advisor to explore better-suited alternatives.

Last updated on: