Quick Overview

Originally a joint venture between Edelweiss Group and Tokio Marine of Japan, Edelweiss Tokio Life Insurance was founded in 2011. Since then, it has operated under the Edelweiss brand and gradually expanded its footprint across India through a multi-channel distribution network, including 1,000+ branches and 80+ partnerships.

Over the years, Edelweiss Life has built a reputation for maintaining a strong Claim Settlement Ratio and a healthy Amount Settlement Ratio. However, metrics such as complaint volume and business scale reveal a more nuanced picture.

In this guide, we review Edelweiss Life Insurance’s performance across key operational metrics, its plan and rider offerings, and whether it’s the right fit for you.

Note: A simple term insurance checklist can help you compare insurers, check claim settlement ratios, and understand exclusions without feeling overwhelmed.

Edelweiss Life Insurance Performance Metrics

For the Amount Settlement Ratio (ASR), we have considered the average of FY 21-24, as the latest FY 24-25 metrics haven’t been released yet.

Key Insights:

- Edelweiss Life’s CSR (99.24%) is slightly higher than the industry mean, indicating a strong record in settling individual death claims. However, insurers like Axis Max Life perform marginally better with a CSR of 99.65% (FY 22-25).

- The ASR (95.6%) is above the industry average, suggesting that the insurer treats both low and high-value claims fairly. However, insurers like Axis Max Life perform better here with an ASR of 96.5% (FY 21-24).

- The solvency ratio, although slightly below the industry median, sits comfortably above the IRDAI’s mandated minimum of 1.5, indicating adequate capital strength. However, insurers like Bajaj Life perform exceptionally well with a solvency ratio of 4.37 (FY 22-25).

- The complaint volume of 167.33 complaints per 10,000 claims is significantly higher than the industry median. On the other hand, insurers such as HDFC Life have a minimal complaint volume of 1.33 (FY 22-25) despite operating at a larger scale.

- Edelweiss Life’s annual business volumes are quite low compared to the industry median. Despite operating since 2011, Edelweiss Life remains smaller than private insurance leaders. On the other hand, insurers like HDFC Life have recorded an annual business volume of ₹30,560 crore (FY 22-25), reflecting stronger customer trust.

Note: At Ditto, we use a 3-year average for key operational metrics to smooth out short-term volatility and avoid overreacting to one-off events, seasonality, or unusual market conditions.

The above metrics pertain to the overall life insurance segment, which includes term insurance, savings plans, ULIPs, and other products. While these metrics are not disclosed separately for term insurance, they remain indicative and relevant for assessing term insurance performance.

If you are looking for comprehensive term coverage that align your future goals, we recommend the best term insurance companies for 2026.

Top Plans Offered by Edelweiss Life Insurance

Edelweiss Life Insurance offers various types of life insurance plans:

- Guaranteed income plans such as Flexi Dream Plan, Guaranteed Savings STAR, Premier Guaranteed STAR Pro, etc.

- Group plans such as Group Employee Benefit Plus, Group Total Secure, and Group Life Protection Plan.

- Wealth creation plans such as Group Wealth Accumulation, Wealth Ultima, Wealth Premier, etc.

- Retirement plans such as Premier Guaranteed STAR Pro, Flexi Savings Plan, Guaranteed Savings STAR, etc.

- Micro plans such as Jan Suraksha and Raksha Kavach Bima Yojana.

If you’d like to learn more about these plans in detail, you can find the product listings on the official insurer website.

The insurer also offers term insurance, which we’ll look at more closely.

Term Insurance Plans by Edelweiss Life Insurance

Saral Jeevan Bima

This is a standard term insurance product mandated by IRDAI, offering simple life cover with fixed features across insurers. It has basic coverage without customisation and is ideal for first-time buyers seeking straightforward protection.

Zindagi Protect Plus

A term plan that offers coverage up to age 100. You can choose between two plan options: Life Cover or Return of Premium. It also offers optional add-on benefits such as Better Half Benefit, Child’s Future Protect Benefit, and Premium Break Benefit (available under the Life Cover option). For death benefit payout, you can select Lumpsum, Monthly Income, or Lumpsum plus Monthly Income. Premium payment options include regular pay and limited pay. Optional riders include Accidental Death Benefit, Accidental Total & Permanent Disability, Critical Illness, and Waiver of Premium.

Premium Comparison for Zindagi Protect Plus

While Edelweiss Life’s premiums are competitive for certain female profiles, Axis Max Life tends to be consistently cheaper for similar cover configurations, especially at age 30.

Note: For this example, we’ve taken profiles of healthy, non-smoking individuals living in a tier-1 city like Delhi, covered for a sum assured of ₹2 crores till the age of 70. (without first-year discounts).

The premiums are indicative in nature as they vary based on your age, health conditions, lifestyle choices, and underwriting decisions.

Riders Available in Edelweiss Life Insurance Plans

Accidental Death Benefit Rider

Accidental Total & Permanent Disability Rider

Critical Illness Rider

Waiver of Premium Rider

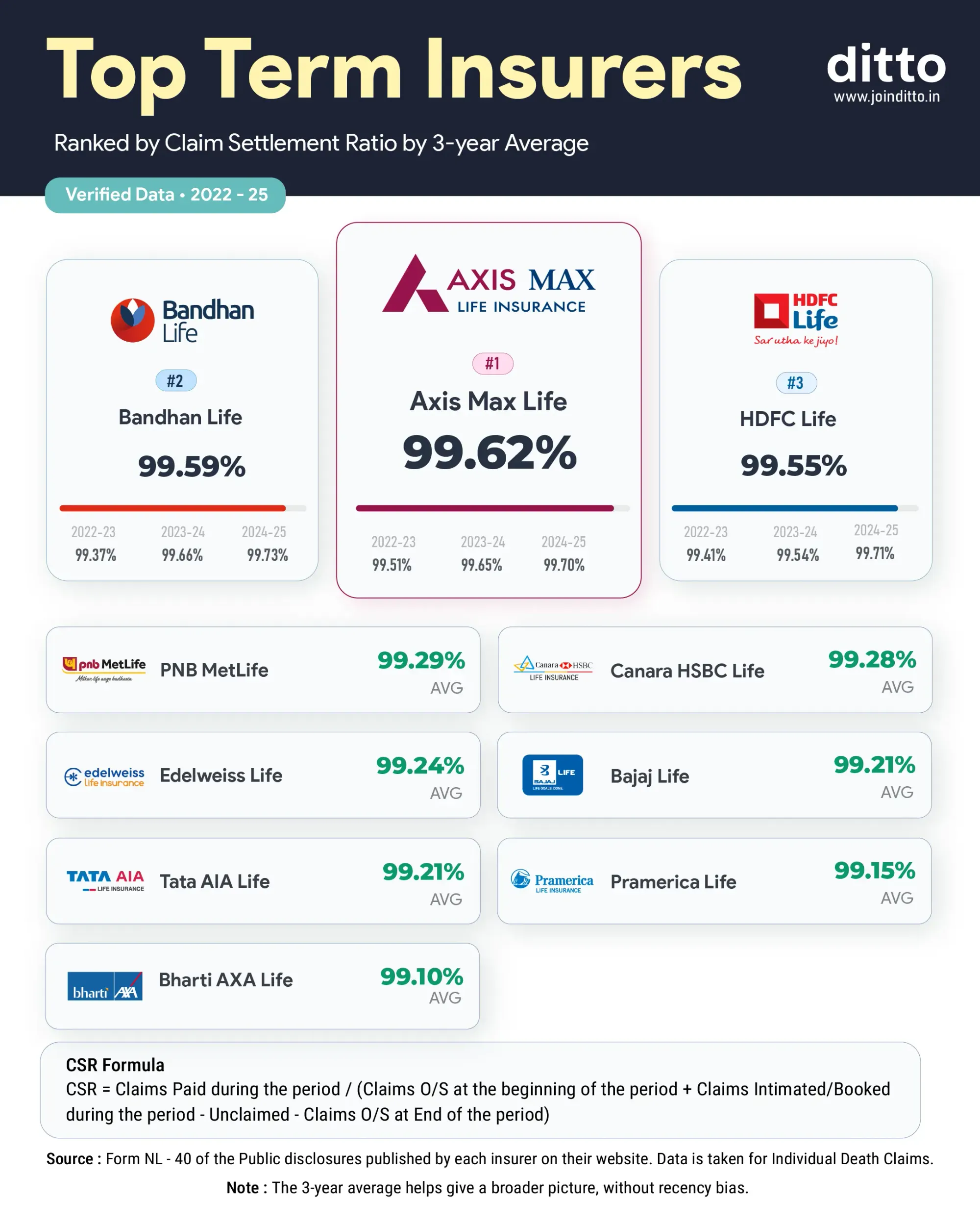

Top 10 Life Insurance Companies in India by Claim Settlement Ratio

The top 10 life insurance companies ranked by Claim Settlement Ratio are as follows:

Although Edelweiss Life Insurance makes it to the list of the top 10 term insurers ranked by CSR, it should be considered in context. Many other insurers on the list operate on a much larger scale with significantly higher policy volumes, which can make it comparatively easier for a small player like Edelweiss to maintain a high CSR.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Ditto’s Take on Edelweiss Life Insurance

Edelweiss Life Insurance performs well across claim settlement metrics, indicating good payout reliability. However, its smaller business scale and relatively higher complaint ratio suggest areas where it trails larger private insurers.

As for product offerings, Edelweiss Life Insurance’s Zindagi Protect Plus is a decent solution with useful rider options. However, flagship plan offerings from insurers such as Axis Max Life and HDFC Life may be better suited for most individuals. These insurers offer lower complaint volumes, wider servicing networks, greater financial stability, and more comprehensive coverage at competitive premiums.

Full Disclosure

Frequently Asked Questions

Last updated on: