Quick Overview

When you buy a life or term insurance policy, one of the most important questions is whether the insurer will pay the claim when your family needs it. That's where the claim settlement ratio (CSR) becomes a key indicator.

One insurer that consistently stands out on this metric is Tata AIA Life Insurance. It is a joint venture between Tata Sons and AIA Group, one of the largest life insurance organizations in the Asia-Pacific region. Founded in 2001, Tata AIA has grown into one of India's leading private life insurers. It is known for its wide range of term and life insurance products, strong digital infrastructure, and customer-first claims process.

In this article, we break down the Tata AIA claim settlement ratio, review its performance over the past years, and assess how reliably it settles claims for policyholders.

How to Calculate the Tata AIA Claim Settlement Ratio?

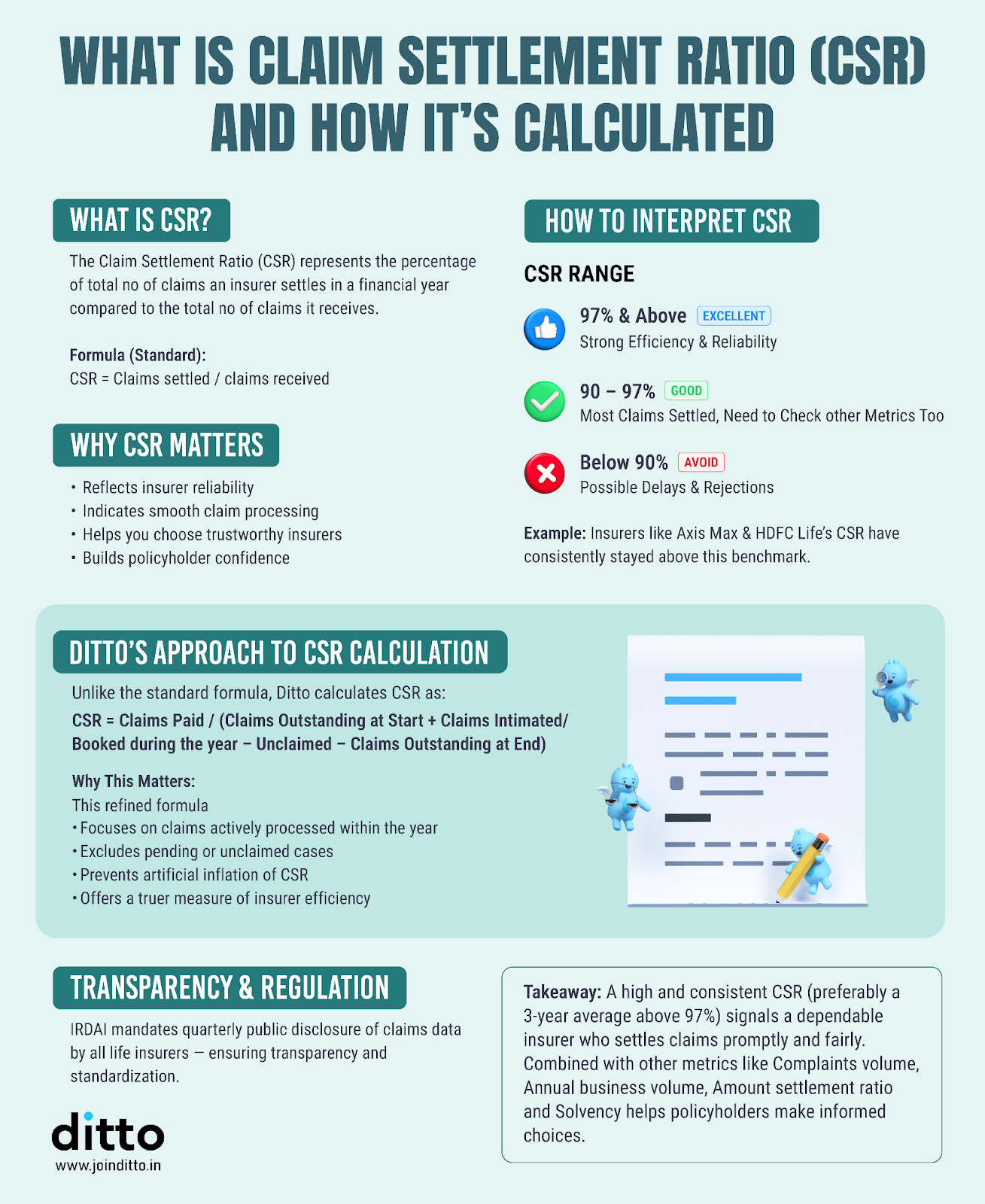

The infographic below describes what the claim settlement ratio is and how it is calculated. If you want to calculate the claim settlement ratio of Tata AIA Life Insurance on your own, you can follow this simple guide.

CSR = (Number of Claims Settled / Total Number of Claims) × 100

It's important to note that insurers may report CSR figures that differ from ours. At Ditto, we apply a uniform methodology across all insurers to ensure a fair comparison. This approach excludes claims closed without payment, including those rejected due to non-admissibility or lack of response from the policyholder after document requests, to ensure the results are not distorted. We also average data over three years to provide a more accurate, outcome-focused view of how reliably an insurer settles valid claims.

Tata AIA Claim Settlement Ratio Last 5 Years

Note: The Tata AIA claim settlement ratio reported by IRDAI includes their entire life insurance portfolio. This includes term insurance, ULIPs, whole life policies, endowment plans, and other life insurance products.

What Does Tata AIA's CSR Mean For You?

Tata AIA has been one of the most consistent performers when it comes to claim settlement. Its claim settlement ratio has crossed the 99% mark for three straight years. That kind of upward trend is rare in the industry and signals a mature, well-run claims process.

That said, the claim settlement ratio of Tata AIA alone isn't enough to make a decision. You should also look at the amount settlement ratio (ASR), complaint volume, business volume, and solvency ratio before choosing a life insurance plan. A high CSR indicates that the insurer pays, but the other metrics reveal how much they pay, how stable they are, and how smoothly the process runs.

Other Key Performance Metrics of Tata AIA Life Insurance

Here are other key metrics of Tata AIA Life Insurance that prove its claims efficiency, financial strength, and reliability.

Top 10 Life Insurance Companies by Claim Settlement Ratio

As you can see, Tata AIA Life Insurance claim settlement ratio ranks 7th among the top 10 life insurance companies in India. The competition among top life insurers has become fierce, with most consistently crossing the 99% mark.

Where Can I Find the Tata AIA Claim Settlement Ratio?

You can check the official Tata AIA Life Insurance claim settlement ratio from the following sources:

- IRDAI's annual reports

- Tata AIA's official website in its public disclosures

- Trusted platforms like ours, which regularly update the data from IRDAI

Why Choose Ditto for Your Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or WhatsApp us now!

Conclusion

Tata AIA claim settlement ratio is undeniably high, and it offers solid reassurance. Looking at the other performance metrics, Tata AIA Life Insurance demonstrates consistent reliability, financial strength, and efficient claim handling, making it a dependable choice for life insurance.

To conclude, Tata AIA is a great pick, especially if you value consistency, low complaint rates, and a trusted brand. However, if you're seeking the absolute best in terms of claim performance across all metrics, it's worth comparing it against the best term insurance companies in India before making your final decision.

Disclaimer

Frequently Asked Questions

Last updated on: