Quick Overview

Most of us don’t pay much attention to health insurance until something goes wrong. But when it’s time to use it, a lack of clarity can quickly turn into frustration and unexpected costs. From choosing the right insurer to understanding claims, renewals, and exclusions, knowing how does a health insurance work helps you make informed decisions and avoid surprises during medical emergencies.

In this guide, we break down how does health insurance work and explain key concepts in simple terms so that you’re prepared long before you need to make a claim.

How Does Health Insurance Work: Key Steps

Step 1: Choose a Reliable Insurer

When choosing a health insurer, look beyond just the premium. A Claim Settlement Ratio (CSR) above 90% indicates that most submitted claims are approved, while an Incurred Claim Ratio (ICR) between 55%–80% reflects balanced pricing and financial stability.

Pay attention to complaint volume as well, fewer complaints per 10,000 claims usually mean smoother claim processing and better customer experience. It’s equally important to check the insurer’s hospital network, especially hospitals near your home or places you frequently travel to, to ensure easy access to cashless treatment.

Finally, read customer reviews, decode policy terms, note how quickly the insurer responds to queries, and assess how transparent they are about terms. Insurers with a track record of fair, fast claims and reliable support tend to make your health insurance journey far less stressful.

Step 2: Choose an Affordable Comprehensive Health Plan

The right comprehensive health insurance policy matches your health needs, family situation, budget, and future risks.

Must-Have Features:

- Zero co-payment

- No room rent restrictions

- No disease-wise sub-limits

- Restoration of sum insured (at least once per year)

- Pre- and post-hospitalization coverage

- Daycare treatment

Good-to-Have Features

- Unlimited restorations in a policy year (for same and different illness)

- Domiciliary hospitalization coverage

- No-claim bonus that increases sum insured

- AYUSH coverage

- Modern treatments

- Simple proposal process and responsive customer support

When reviewing policies, go through the policy brochure and wording carefully to understand exactly what’s covered and what isn’t.

Here’s a simple guide on how to choose the right health insurance policy.

Step 3: Premium Determination

Premiums are central to how does health insurance work, but choosing a plan purely based on low premiums is risky. Insurers calculate premiums based on:

- Your age and medical history

- Number of people covered

- Location (healthcare costs differ by city)

- Occupation and lifestyle risks

- Chosen sum insured

Health insurance works on a pooling system, where many people pay small premiums into a shared fund. While most stay healthy in a given year, a few may face costly medical emergencies. The insurer uses this shared pool to pay those large hospital bills.

Even if you don’t make a claim, your premium helps sustain this pool. In return, when you need treatment, it protects you from paying hefty medical costs yourself. This is the core of how health insurance works.

How Health Insurance Works: Important Policy Concepts

Beyond buying a policy, understanding a few core policy concepts helps you avoid claim rejections and unexpected expenses.

- Inclusions and Exclusions: Inclusions explain what your policy covers, while permanent exclusions list treatments or situations that are never covered. Knowing this upfront helps you set clear expectations and plan expenses better. Always read your policy wording for complete terms and conditions.

- Waiting Periods: Certain treatments are covered only after a defined waiting period from the policy start date such as an initial waiting period, pre-existing disease waiting period, or specific illness waiting period. Understanding these timelines ensures you don’t expect coverage before it becomes active.

- Portability and Migration: Portability lets you switch your health insurance policy to another insurer without losing benefits like completed waiting periods, moratorium benefits, or accumulated bonuses. Migration allows you to move to a different plan within the same insurer. Both help you upgrade coverage without starting over.

How Does Health Insurance Renewal Work?

Renewal is a continuation of how does health insurance work over time. When you renew your policy timely, you retain benefits like completed waiting periods and no-claim bonuses.

We recommend renewing your health insurance policy before its due date to avoid any disruption in coverage. If you miss the deadline, insurers offer a grace period during which you can still make the renewal payment and continue enjoying your policy benefits.

As per IRDAI guidelines, the grace period is 15 days for monthly premium payments and 30 days for quarterly, half-yearly, and annual payment modes. If you fail to renew within this period, your policy may lapse, leading to cancellation and loss of accumulated benefits like waiting period credits and no-claim bonuses.

How Does Health Insurance Claim Work?

A health insurance claim is how you ask your insurer to pay for your medical treatment. When you’re hospitalized, the insurer checks whether your expenses are covered under your policy, fall within your sum insured, and comply with inclusions and exclusions.

There are two ways health insurance claims are settled: through cashless treatment or reimbursement. In a cashless claim, the hospital coordinates directly with the insurer, and the approved amount is paid straight to the hospital. In a reimbursement claim, you pay the bills upfront and submit the documents required for review to the insurer. In both cases, timely intimation, accurate paperwork, and policy clarity play a key role in smooth claim approval.

Many claim issues are preventable. This guide on why health insurance claims get rejected explains what usually goes wrong and how to stay protected.

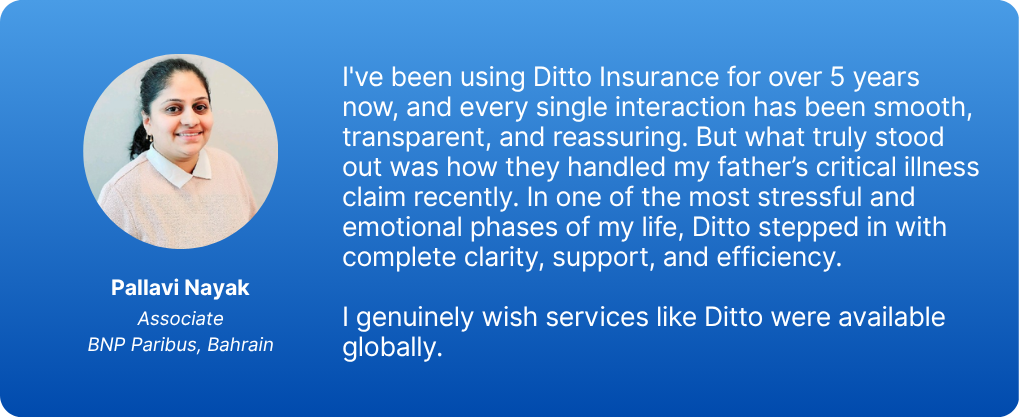

Why Approach Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call now or WhatsApp us.

Conclusion

Once you understand how does health insurance work in India, it becomes less about paperwork and more about protection. A good health insurance policy shields you from rising medical costs, gives you access to timely treatment, and offers financial stability during uncertain times. By choosing the right insurer, understanding your policy features, renewing on time, and knowing how claims work, you ensure that your health insurance supports you when it matters most.

Frequently Asked Questions

Last updated on: