Cataracts are one of the most common eye conditions affecting people as they age, leading to blurry vision and, if left untreated, potential blindness. While life expectancy is rising, people also have an increased exposure to diabetes, hypertension, and other lifestyle habits, due to which cataract cases have been rising significantly in India.

While cataract surgery is a routine procedure with a high success rate, the cost of this surgery can vary widely depending on the hospital, the type of procedure, and the intraocular lens (IOL) used. As medical inflation continues to push healthcare costs higher, health insurance has become necessary for managing such cataract surgery expenses.

A good health insurance policy will cover the entire surgery surgery cost, reducing your financial burden. However, coverage varies across policies, with different waiting periods, sub-limits, and exclusions. Understanding these factors can help individuals choose the best insurance plan for cataract treatment.

Pro tip: The health insurance market can be a labyrinth. Instead of spending hours navigating through the hundreds of policies out there, why not book a 30-minute call with our expert IRDAI-certified advisors? We don’t spam or pressure you to buy. Just honest insurance advice.

Does Health Insurance Cover Cataract Surgery?

Yes, most health insurance policies in India do cover cataract surgery, but the coverage depends on several factors, such as the type of policy, the insurer’s terms, and, most importantly, sub-limits imposed on cataracts.

In most of the top health insurance plans, cataract surgery is included as part of daycare procedures without any sub-limit, meaning hospitalization beyond 24 hours is not required, and the insurer will cover the entire amount as long as it is reasonable & customary. However, the insurer will cover this only after a specific waiting period.

If your personal health insurance plan does not cover cataracts without a sub-limit, or you are still in the waiting stage, employee health insurance plans also often include coverage for cataract surgery. However, individual policies tend to offer more flexibility and higher cover amounts. The extent of coverage varies across insurers, so you should always check the policy details before relying on either insurance for the procedure.

Factors Affecting Cataract Surgery Coverage

While most health insurance policies cover cataract treatment, specific policy terms can impact the extent of coverage. Here are some factors you should consider:

1. Waiting Period

Most insurers impose a waiting period for cataract surgery that usually ranges between 12 and 24 months. This means that if you purchase a new policy, you may have to wait for a year or two before the insurer pays for cataract-related expenses This is called the specific illness waiting period.

2. Cover Amount Limitations

Many insurers place a cap on the amount you can reimburse for cataract surgery. This cap can be either:

- A fixed limit (e.g., ₹40,000 per eye), or

- A percentage of the cover amount (e.g., 10-25% of the total cover amount).

Policies without a sub-limit on cataract surgery provide better coverage, ensuring you have lower out-of-pocket expenses.

3. Pre-Existing Disease Clause

If a cataract is diagnosed before purchasing the policy, insurers may treat it as a pre-existing condition, usually leading to longer waiting periods (up to 3 years) under the pre-existing disease waiting period. Some policies may completely exclude pre-existing cataracts from coverage.

Types of Cataract Surgery Covered by Health Insurance

Cataract surgeries have evolved significantly since its inception, with advanced techniques providing better precision, faster recovery, and an improved success rate. Health insurance policies usually cover standard surgical methods but may have limitations on other types of cataract surgeries. Let’s take a look at them now.

1. Traditional Cataract Surgery (Phacoemulsification)

This is the most commonly covered procedure in health insurance plans. The surgeon removes the clouded lens and replaces it with an intraocular lens (IOL).

2. Laser-Assisted Cataract Surgery (Femtosecond Laser)

Laser cataract surgery is an advanced, bladeless procedure with higher precision. Some insurance policies cover it, while others may only reimburse the cost equivalent to traditional surgery, requiring you to pay the difference.

3. Intraocular Lens (IOL) Implantation

Standard mono-focal lenses are generally covered by health insurance. However, more expensive lenses such as multifocal, toric, or trifocal lenses may not be covered entirely, and you may have to pay the additional cost. It’s always better to check with your insurer before the surgery.

How to Claim Insurance for Cataract Surgery?

You can claim insurance for cataract surgery in two ways:

1. Cashless Treatment at Network Hospitals

- The insurer or TPA will pre-authorize the procedure upon your claim intimations 24-48 hours prior.

- The insurer directly settles the hospital bill, subject to your policy sub-limit and cover amount.

- You only pay for non-covered expenses, such as consumables or a more expensive type of lens, if the policy does not cover it.

2. Reimbursement Process for Non-Network Hospitals

- You pay for the surgery upfront and collect all medical bills, reports, and invoices.

- These documents are submitted to the insurer for reimbursement after discharge.

- The insurer evaluates the claim and transfers the approved amount to your bank account.

Best Health Insurance Plans Covering Cataract Surgery in India

Several comprehensive health insurance plans cover cataract surgery with minimal restrictions. Let’s take a look at them now:

- HDFC ERGO Optima Secure: HDFC ERGO Optima Secure is a robust health insurance plan offering coverage from ₹5 lakh to ₹2 crore. This policy has comprehensive coverage with no room rent limits, disease-wise sub-limits, or mandatory copayment. It also includes extensive pre and post-hospitalization coverage, daycare procedures, and domiciliary treatments. It provides significant financial protection with features like 100% restoration once during the policy period and a cumulative bonus of 50% per year up to 100% of the base sum insured. Unique benefits like the Secure Benefit, which doubles the base coverage from day one, and the Protect Benefit, which covers consumable expenses, make this plan attractive. Additionally, home healthcare services are covered on a cashless basis. Notable add-ons include Unlimited Restoration, OPD coverage through Optima Well-being, and a critical illness cover for 51 conditions.

- Care Supreme: Care Supreme provides extensive coverage ranging from ₹5 lakh to ₹1 crore, ensuring flexibility without disease-wise sub-limits or room rent capping. The plan includes 60 and 180 days of pre and post-hospitalisation coverage, daycare procedures, AYUSH treatments, and domiciliary care. The restoration benefit is available an unlimited number of times during the policy period, and policyholders can benefit from a cumulative bonus of 50% per year up to 100% of the base sum insured. Care Supreme offers unlimited e-consultations with general physicians and wellness discounts of up to 30% on renewal premiums based on fitness goals. Notable add-ons include Instant Cover, which reduces waiting periods for pre-existing conditions like hypertension and diabetes to just 30 days, and Claim Shield, which covers non-payable medical expenses.

- Aditya Birla Activ One Max: Aditya Birla Activ One Max provides coverage from ₹5 lakh to ₹6 crore and includes wellness benefits like HealthReturns, which offers premium discounts for maintaining good health. The plan has no restrictions on room rent and includes pre and post-hospitalisation coverage of 90 and 180 days, respectively. It also covers daycare procedures, AYUSH treatments, and domiciliary care. The Claim Protect feature ensures inbuilt coverage for consumables, while the Super Reload feature provides unlimited restoration benefits after the first claim. The Super Credit Bonus increases the sum insured by 100% annually up to 500%. Additional optional covers include Chronic Care, which provides day-one coverage for pre-existing conditions like diabetes and hypertension, a Cancer Booster for enhanced cancer-related expenses, and Durable Equipment Cover for medical devices like wheelchairs and ventilators.

- Niva Bupa Aspire Titanium+: Niva Bupa Aspire Titanium+ is a high-end plan offering a sum insured of up to ₹3 crore with unique benefits like Lock the Clock+, which ensures premium stability based on entry age, and Future Ready, which guarantees continuity for a future spouse’s coverage. The policy provides coverage for any room, 60 and 180 days of pre and post-hospitalisation, daycare treatments, AYUSH, and domiciliary care. A unique feature, Booster+, allows policyholders to carry forward unutilized coverage based on age brackets. Maternity coverage includes prenatal care, delivery (normal and cesarean), surrogacy-related expenses, and a nine-month waiting period. Policyholders can also benefit from a Live Healthy Discount of up to 30% on renewal premiums. Notable add-ons include Safeguard+ for inflation-adjusted claims and consumables, Borderless for international hospitalization coverage, and Cash-Bag, which accumulates cashback on claim-free years to be used for future premiums or medical expenses.

- ICICI Elevate: ICICI Lombard’s Elevate plan is among the most customizable health insurance options, offering coverage up to ₹3 crores and a variety of add-ons. The plan covers hospitalization in a single private room (upgradeable via add-ons) and includes 90 and 180 days of pre and post-hospitalization coverage. It provides coverage for daycare procedures, AYUSH, and domiciliary treatments. The policy stands out with wellness discounts of up to 30% for maintaining good health and Jumpstart, an add-on that reduces waiting periods for specific pre-existing conditions to just 30 days. Inflation Protector ensures that the sum insured keeps pace with rising medical costs, while the Power Booster add-on offers a 100% bonus increase per year. Other notable add-ons include Infinite Care, which provides lifetime coverage for a single hospitalization claim, maternity coverage up to ₹1 lakh with a waiting period of 1-2 years, and durable equipment coverage for medical devices.

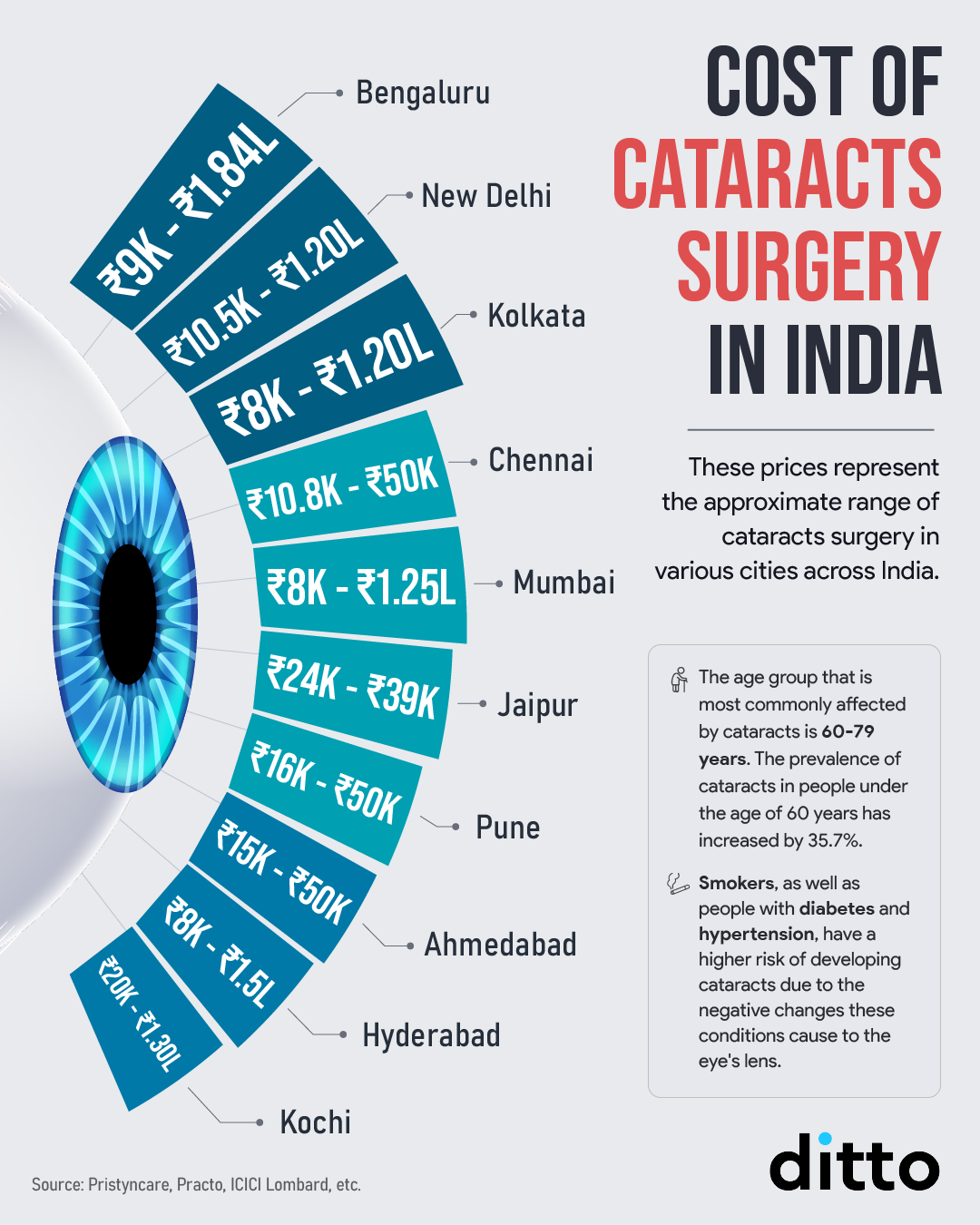

Cost of Cataract Surgery Without Insurance in India

The cost of cataract surgery in India varies widely, depending on the hospital and type of lens used.

- Government hospitals: ₹8,000 - ₹15,000

- Private hospitals (standard lens): ₹25,000 - ₹50,000 per eye

- Premium hospitals & advanced lenses: ₹80,000 - ₹1,90,000 per eye

Without insurance, these costs can add up quickly, especially if you need surgery for both eyes.

Why Talk to Ditto for Your Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Abhinav below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now!

Conclusion: Should You Get Health Insurance for Cataract Surgery?

With rising cataract cases and expensive treatments, having health insurance that covers cataract surgery is beneficial. It helps reduce out-of-pocket expenses, provides cashless treatment, and ensures you receive good quality healthcare without financial strain. Purchasing the right health insurance policy early can help secure timely treatment without worrying about expensive medical bills.

Last updated on: