Quick Overview

India is a lower-middle-income country, with a per capita income of around ₹2,73,237. As a result, people may not always prioritize health insurance due to other financial responsibilities. However, health coverage plays a key role in ensuring financial security. In this case, the best resort is to start small since some cover is exponentially better than no cover.

This is where ₹10 lakh health insurance comes in. Although this amount is considered an affordable starting point, will it protect you as medical costs rise? Let’s discuss further in this guide.

Key Features of a ₹10 Lakh Family Health Insurance Plan

A ₹10 lakh family health insurance plan covers medical expenses up to ₹10 lakh every policy year. In family floater plans, the sum insured is shared among all covered members. If one member uses a large part of the coverage for hospitalization or treatment, the remaining amount available for the others reduces. That could leave the family short of funds if multiple claims arise in the same year.

To learn more about the features of a family health insurance plan, refer to our guide on family floater health insurance.

Meanwhile, a ₹10 lakh family health insurance plan covers circumstances like:

- Pre- and post-hospitalization expenses for illnesses, accidents, or planned or emergency surgeries

- Daycare treatments like dialysis, chemotherapy, cataract surgery, or tonsillectomy

- Domiciliary hospitalization

- Ayurveda, Yoga, Unani, Siddha, and Homeopathy (AYUSH) hospitalization coverage

Best ₹10 Lakh Health Insurance Plans

Here, CSR stands for claim settlement ratio, ICR denotes incurred claims ratio, SI refers to sum insured, and PA implies per annum.

For more details, refer to our guide on the best health insurance plans in India 2026.

Let’s compare sample premiums of ₹10 lakh health insurance and higher sum insured options for a tier 1 city (New Delhi: 110001). The comparisons are for HDFC Ergo Optima Secure.

What is the Average ₹10 Lakh Health Insurance Premium?

Here, ‘A’ refers to an adult, and ‘C’ denotes a child.

Please note that the unlimited restoration add-on and online discount are included in the pricing. The premiums are indicative, and the final amount may vary based on your medical profile, age, or location.

Key Insight: The above table also shows that the price difference between a ₹10 lakh health insurance plan and other plans with higher sum insured options is quite small. In short, the premiums for a higher sum insured don't increase linearly.

How to Choose the Best ₹10 Lakh Medical Policy?

You must consider your age, existing health conditions, and family composition, among other factors, when choosing the best ₹10 lakh health insurance policy. Refer to our guide on how to choose health insurance to learn more about key features to look out for or other considerations when choosing a plan.

Benefits and Drawbacks of ₹10 Lakh Health Insurance

Is a ₹10 Lakh Health Insurance Cover Enough for You?

Despite the minimal price difference, if you have difficulty affording the premiums for a higher sum insured, a ₹10 lakh health insurance policy isn’t a bad option. However, it may also not be reliable in the long run due to the following reasons:

- A health emergency could turn your life upside down without insurance (black swan analogy). The most common examples are high-cost medical transplants or treatments like cancer (bone marrow transplant) that impact people’s lives directly.

- The other two reasons are medical inflation and difficulty in increasing the sum insured after being diagnosed with a serious illness, which we discussed in the drawbacks section.

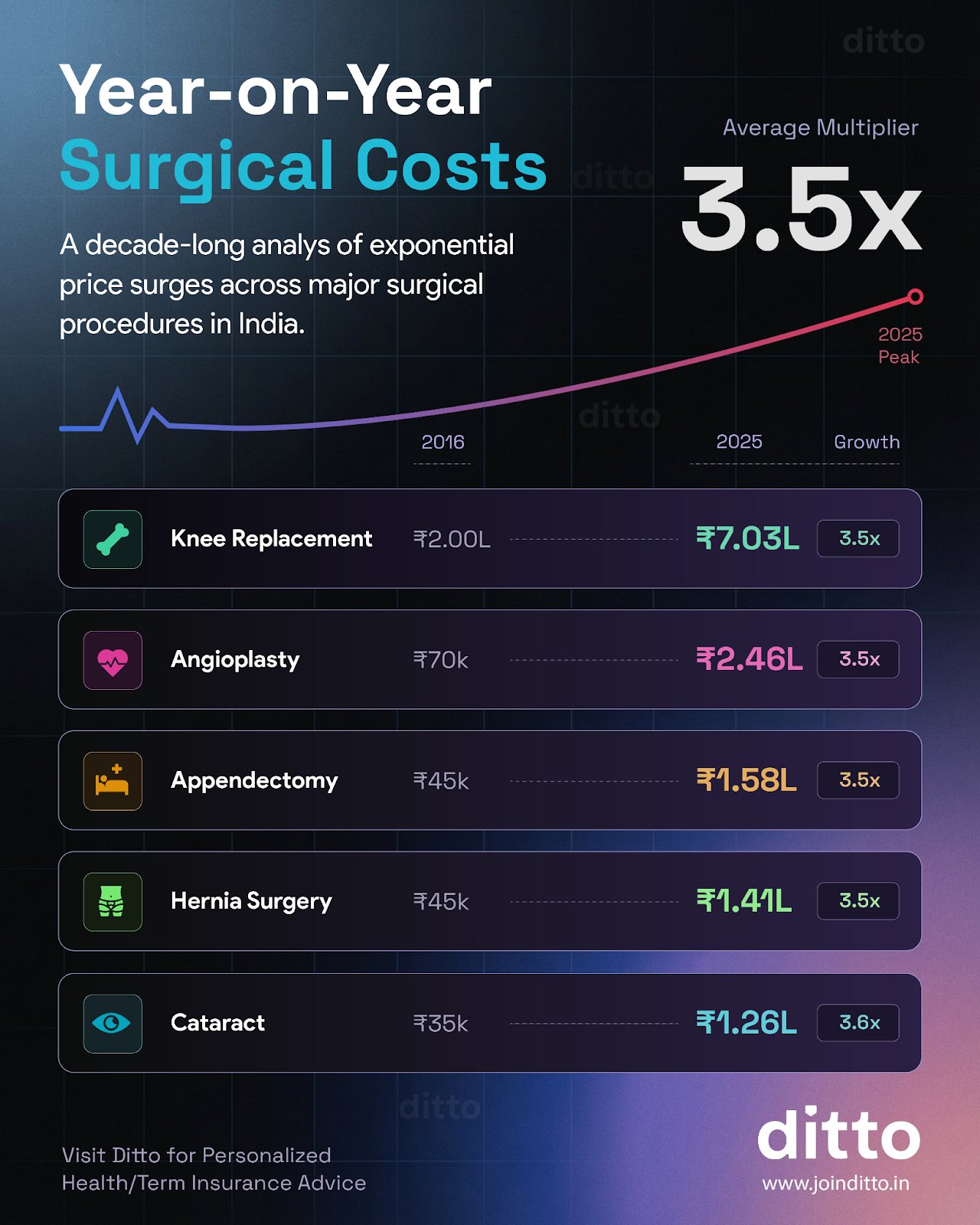

Here’s an infographic showcasing the differences between surgical costs in India between the years 2016 and 2025:

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or chat on WhatsApp with us now!

Ditto’s Take on ₹10 Lakh Health Insurance

Most insurers have a minimum sum insured requirement depending on the location of policy purchase. For Tier-1 cities like Mumbai and New Delhi, some plans may not offer the option of availing a ₹10 lakh health insurance plan. Considering the hospital bills, how much they cost today, and how difficult it is to make changes to your policy later, we recommend a health insurance cover between ₹15 lakh and ₹25 lakh instead. Additionally, a comprehensive cover with features like unlimited restoration of cover and sufficient bonuses will give you peace of mind in the long run.

Disclaimer

Frequently Asked Questions

Last updated on: