Quick Overview

As the healthcare costs rise, a single medical emergency can wipe out years of savings overnight. At the same time, losing your income due to an untimely death can leave your loved ones struggling with daily expenses, loans, and long-term goals.

So, if you can only buy one insurance policy right now, which one should it be?

At Ditto, we went through IRDAI guidelines, insurer disclosures, and policy documents to curate this guide. In this blog, we explain what term insurance and health insurance are and what to opt for first when choosing between the two.

What is Term Insurance?

Term insurance is a pure life cover where you pay a premium every year (usually low if you buy young). If you pass away during the term, your nominee gets a lump sum payout (the sum assured).

The main purpose of term insurance is to ensure that your dependents are taken care of. It acts as an income replacement while paying off your debts, funding your children’s education, and keeping your family financially stable.

Note: No payout if you survive the policy (unless you choose a special TROP rider or plan).

What is Health Insurance?

Health insurance pays for medical expenses, such as hospital bills, surgeries, tests, treatments, and even some outpatient care, depending on the plan. You can usually choose cashless treatment at network hospitals or get reimbursed.

Key benefits of health insurance are:

- Covers hospitalization & treatment costs.

- You can add riders such as pre-existing disease waiting period reduction, consumables cover, restoration benefit, etc.

Key Differences: Term Insurance vs Health Insurance

While we understand that term life insurance vs health insurance comparisons can often get confusing, understanding the core differences can help.

Many people are also confused between term insurance vs life insurance vs health insurance.

Term insurance is a part of life insurance, which includes whole life, endowment, and even ULIPs. These policies often come with an investment component. For example, in ULIPs (Unit Linked Insurance Plans), you get the dual benefit of life coverage along with the opportunity to invest in market-linked funds, such as equity, debt, or balanced funds.

In an endowment policy, you get both life coverage and a lump sum payout after a certain number of years, which can be used as a savings or investment tool. On the other hand, in a whole life policy, the coverage continues for the entire life of the policyholder.

Term Insurance vs Health Insurance: What to Buy First?

At Ditto, we cannot emphasize enough how important it is to have both health and term insurance. However, if you can only buy one right now, here’s the practical answer:

1) Buy Health Insurance First

This is because health emergencies are far more likely than sudden death. Even young and healthy people face accidents, sudden illnesses, or hospital stays, and medical costs can easily climb into lakhs.

Moreover, many plans have long waiting periods for pre-existing conditions, so the earlier you buy, the earlier you can get complete coverage.

You can also check out our detailed guide on “How Much Health Insurance Coverage Do I Need” to get a better idea.

2) Buy Term Insurance Next

Once you have health coverage, term insurance becomes the next priority, especially if:

- You have a spouse, children, or aging parents depending on your income.

- You have loans (home loan, personal loan, education loan, etc.).

- You want peace of mind knowing your loved ones won’t struggle financially if something happens to you.

- If you’d like to find out the suitable cover amount required for your financial needs, you can check out the cover calculator tool on our website.

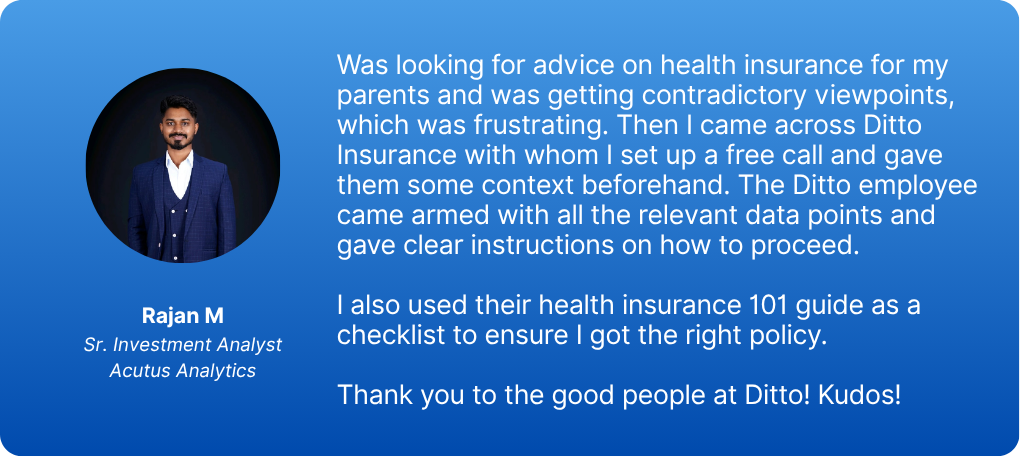

Why Choose Ditto for Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Rajan below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

Buying insurance isn’t about predicting the future, as it’s about protecting your present and future with smart financial planning. When choosing between term vs health insurance, it is important to build the foundation first. Everything else from your savings, investments, and retirement planning becomes easier and more secure.

Frequently Asked Questions

Last updated on: