Quick Overview

ULIPs like SBI Life Smart Fortune Builder promise long-term wealth creation along with life cover. But many buyers struggle to answer a simple question: Is this policy actually worth it, or are you better off separating insurance and investment? In this guide, we look at the plan’s features, charges, drawbacks, and how it compares with term insurance.

SBI Life: Performance Metrics

Key Insights:

- SBI Life maintains a strong CSR, but it is still slightly lower than the industry average.

- The insurer’s ASR indicates that it treats both high and low-value claims fairly.

- SBI Life’s complaint volume is significantly lower than the industry median, reflecting better service quality.

- The solvency ratio meets the IRDAI (Insurance Regulatory and Development Authority of India) requirements of 1.5x, indicating financial stability.

- It is the second-largest insurer in India by business volume, after LIC (Life Corporation of India).

Note: SBI Life Insurance performs well across key operational metrics and ranks among the top term insurance companies in India. However, these metrics reflect the insurer’s overall life insurance business and do not necessarily indicate that the Smart Fortune Builder is a strong offering.

Key Features of SBI Life Smart Fortune Builder

Life Cover Benefit

In case of the death of the policyholder during the policy term, the nominee receives the highest of the following:

- Fund value

- Sum assured (after adjusting the partial withdrawals)

- 105% of the total premiums paid

Maturity Benefit

If the policyholder survives the policy term, they receive the fund value as a lump sum, based on the performance of the chosen funds.

Fund Options

SBI Life Smart Fortune Builder offers 12 investment funds, including equity, debt, and balanced options. The plan also allows fund switching (2 free switches per year and then ₹100 per switch), helping policyholders rebalance investments as market conditions change

Charges in Smart Fortune Builder SBI Life

- Premium Allocation Charge: Applies in early years (9% in year 1, 6.5% in year 2 and 3, and so on) but is waived from the 11th year (for regular pay).

- Policy Administration Charge: Waived for the first 5 years (for regular/limited pay), then 0.2% of annualized premium per month, capped at ₹500 per month.

- Fund Management Charge: Varies by fund from 0.25% to 1.35%.

- Mortality Charges: Based on age and sum assured.

- Discontinuance Charges: Applicable if exited early.

For more details, you can refer to the policy brochure of SBI Life Smart Fortune Builder or check out our comprehensive guide on SBI ULIP.

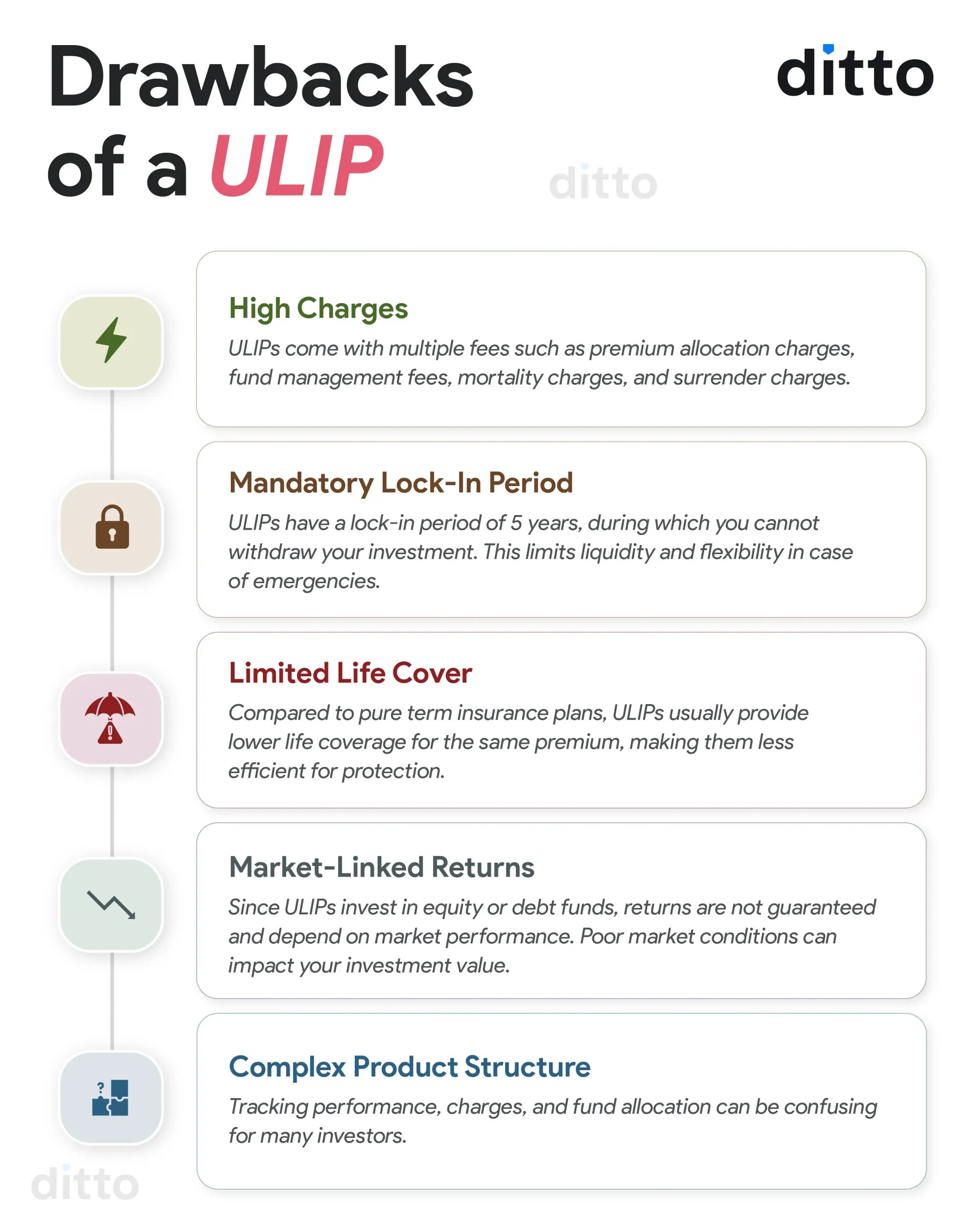

Drawbacks of SBI Life Smart Fortune Builder

Apart from the usual drawbacks of a traditional ULIP, as shown above, SBI Life’s Smart Fortune Builder has a few additional limitations.

- There’s no monthly premium option, and you can redirect premiums only from the second policy year.

- Partial withdrawals are quite restricted, as you can start only from the sixth year, or when the insured turns 18 (whichever is later).

- You get one free withdrawal a year, after which each extra one costs ₹100. Even then, you can make only up to two withdrawals a year and 10 in total over the policy term.

ULIP vs Term Insurance: Which is Better?

Premium Illustration of SBI Life Smart Fortune Builder

We’ve taken the above example of a 35-year-old, covered till 30 years (regular pay), with money invested in the Bluechip Fund, as per the official policy brochure of Smart Fortune Builder.

According to IRDAI, insurers must provide illustrations showing returns of 4-8%.

- In reality, the net return is actually far lower than the 8% you see because ULIPs typically deduct charges, especially in the early years. This means a significant portion of your premium doesn’t get invested.

- Since less money is invested upfront, compounding works on a smaller base, which has a long-term impact on wealth creation.

- Fund management charges and other costs continue throughout the policy term, further reducing returns.

As a result, even if the underlying fund delivers around 8% returns, the net return to the investor often falls closer to 6-7%, particularly over the first 10-15 years.

Term Insurance Premium Comparison

For this example, we’re considering healthy, non-smoking salaried profiles living in a tier-1 city like Delhi (pincode: 110010), covered until age 65 with a sum assured of ₹1 crore.

Takeaway: Term insurance plans provide higher and more comprehensive coverage for a fraction of the cost of Smart Fortune Builder. For more information, you can also check out our detailed guide on ULIPs vs term insurance.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Ditto’s Take on SBI Life Smart Fortune Builder

One aspect often overlooked in a typical SBI Life Smart Fortune Builder review is the complexity of the decisions involved. With multiple fund choices, switching options, and policy structure, the plan requires ongoing involvement and market understanding.

It works best only for highly disciplined investors who are comfortable with long holding periods. For others, it’s better to buy term insurance for coverage and keep investments separate through instruments such as mutual funds, the Public Provident Fund (PPF), or Fixed Deposits (FDs).

Frequently Asked Questions

Last updated on: