Quick Overview

According to IRDAI annual reports, the life insurance industry paid 97.82% of total individual death claims, amounting to ₹33,697 Crore, in FY 24-25. Despite this high payout rate, many policyholders still worry about claim rejection and whether their family will actually receive the benefits. In this guide, we break down everything you need to know, including term insurance claim rejection reasons, regulatory safeguards, and how to avoid them.

What is Term Insurance Claim Rejection?

A term insurance claim rejection occurs when an insurer refuses to pay out the policy benefits to the nominee or policyholder. This can happen for specific policy or legal reasons.

Term insurance claim issues generally fall into three categories:

- Query/Delay: The insurer asks for additional documents or clarification.

- Rejection: The insurer formally denies the claim due to policy/legal grounds. However, insurers cannot reject claims arbitrarily. They must provide valid reasons, back them with evidence, and follow legal guidelines.

- Dispute: The nominee challenges the rejection.

Many claims initially fall into the query stage rather than the rejection stage. Understanding this difference helps avoid unnecessary panic.

Rejection vs Repudiation

A life insurance claim rejection is usually due to minor or technical issues, such as missing documents or processing errors. These problems can often be fixed, and the claim can be submitted again. On the other hand, repudiation is a serious and final denial. It happens after a detailed investigation, usually due to fraud, the concealment of important information, or the claim not being covered by the policy. For more details, you can also check out our detailed guide on rejection vs repudiation.

IRDAI Guidelines for Claim Rejections in Term Insurance

IRDAI has clear regulations in place to protect policyholders.

- Section 45 of the Insurance Act

According to Section 45, after 3 years from the later of policy issuance, commencement of risk, revival, or rider, the policy cannot be called into question. However, claims can still be rejected in cases of proven fraud. - Claim Settlement Timelines

Insurers must settle claims within 15 days when no investigation is needed, and they get an additional 45 days if an investigation is required. - Penalty for Delays

If insurers delay settlement beyond the timelines, they must pay interest (at the bank rate plus 2%) to the nominee.

Top Reasons for Term Insurance Claim Rejection

Material Non-Disclosure or Misstatement

Policy Lapse Due to Non-Payment of Premium

Policy Exclusions

Fraudulent Information or Documents

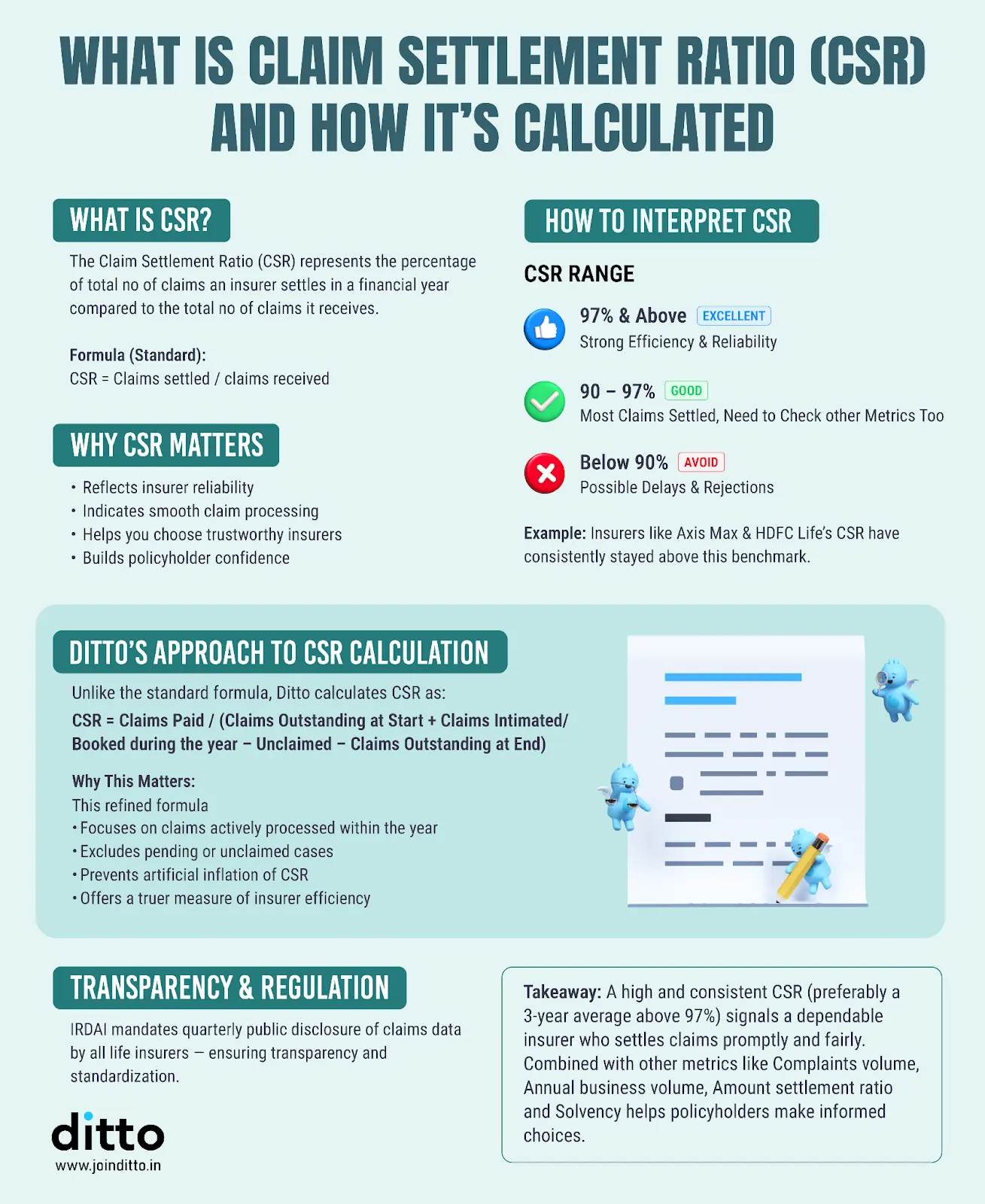

Claim Settlement Ratios of Term Insurance Companies

The Claim Settlement Ratio (CSR) is a key metric that reflects an insurer’s reliability. You can refer to the attached infographic to understand what it is, how it is calculated, and how to interpret it.

With this understanding, let’s take a look at some of the top term insurance CSRs for FY 2022-2025.

Note: These CSR figures are for the insurer's entire life insurance segment, including ULIPs, savings plans, endowment plans, and term plans. Although a high CSR is important, it alone doesn’t guarantee your individual claim will be paid. For more details, you can check out our comprehensive guide on why CSR alone misleads buyers.

How to Avoid Term Insurance Claim Rejection

Be Honest in the Proposal Form

Always provide complete and honest information in the proposal form. Disclose your medical history, lifestyle habits, occupation, and income accurately. Instead of relying on pre-filled forms, try to fill and verify the proposal form yourself.

Pay Premiums on Time

Make sure you pay premiums on time and keep the policy active. Even a good policy becomes useless if it lapses due to missed payments, so setting reminders or using auto-debit can help.

Understand Policy Exclusions

Read and understand policy exclusions carefully during the free-look period. Knowing what is not covered, such as specific conditions or the suicide clause, prevents unpleasant surprises for your family.

Keep Your Nominee Informed

Inform your nominee about the policy details, including insurer name, policy number, and claim process. Many claims get delayed or complicated simply because nominees are unaware of the policy.

Maintain Proper Documentation

Keep all your documents up to date and easily accessible, and avoid hiding any existing insurance policies. Transparency and proper documentation go a long way toward ensuring a smooth, hassle-free claim settlement process.

Choose a Reliable Insurer

When buying term insurance, ensure that the insurer performs well across key operational metrics, such as CSR, Amount Settlement Ratio (ASR), and complaint volumes. Compare policy features and premium details as well.

What to Do if a Term Insurance Claim is Rejected?

1) Review Rejection Letter

The insurer is legally required to clearly mention the reasons and supporting grounds for denial. Understanding the reason for the claim denial will help you decide on your next steps.

2) Gather Evidence and File a Complaint with the Insurer

Submit a formal complaint to the insurer explaining your case and attaching supporting evidence. The policyholder must keep all the documents ready as proof. Insurers are expected to review and respond to complaints within 14 days.

3) Contact Grievance Redressal Officer (GRO)

If the initial complaint does not resolve the issue, escalate it to the insurer’s Grievance Redressal Officer (GRO). The GRO is responsible for handling unresolved complaints and ensuring they are reviewed fairly and in line with regulations.

4) Escalate to IRDAI

If you are not satisfied with the insurer’s response, you can escalate the complaint to IRDAI. You can file a complaint through their grievance platform, and they will intervene to ensure the insurer follows proper procedures.

5) Approach the Insurance Ombudsman

As a final step, you can approach the Insurance Ombudsman. The Ombudsman handles disputes related to claim rejections (for claims under ₹50 Lakh) and can issue binding decisions on insurers. Typically, complaints must be filed within one year of the insurer’s final decision. For claims above ₹50 Lakh, you can reach out to consumer courts.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Conclusion

Although claim rejections are rare, understanding term plan claim rejection reasons can help you avoid mistakes that may delay or derail a payout. With proper disclosure, timely premium payments, and awareness of policy terms, you can ensure your claim proceeds smoothly when it matters most.

In fact, insurers are strongly inclined to settle genuine death claims because such cases are rare. Moreover, regulations laid down by IRDAI, particularly under Section 45, provide strict safeguards that prevent random rejection of policies. Additionally, maintaining a high CSR is crucial for insurers, as it serves as an important trust and marketing metric when attracting new customers.

Full Disclosure: At Ditto, you can always reach out to us for claims assistance if you bought the policy from us. The above article is for informational purposes only, and the details have been sourced from IRDAI reports, guidelines, and publicly available data.

Frequently Asked Questions

Last updated on: