Term insurance is a pure protection plan. It pays your family a lump sum or structured payout if you pass away during the policy term. There is no maturity benefit if you survive, except for return-of-premium variants, which are often not recommended due to their poor cost-to-benefit structure.

Thinking about term insurance but unsure where to start? With dozens of plans, confusing features, and rising premiums with age, choosing the right cover can feel overwhelming.

At Ditto, we’ve guided thousands of people daily to make smarter insurance choices, so we truly understand what matters most when selecting a term plan. This guide breaks down term insurance simply, compares the best plans of 2026, and helps you buy the correct term plan without overpaying.

We’ll be honest: Our job gets harder when premiums are revised. We want you to get the most cover for the least amount of money, and that window is shrinking. Leading insurers are updating their pricing models. So secure your family’s safety net at the current rates while they still exist. Book a 30-minute consultation call or chat on WhatsApp with our experts.

Top Term Life Insurance Plans (2026)

Before we discuss the list, we assess the plans through Ditto’s Cut to ensure strong coverage, clear features, and long-term value.

01

Axis Max Life Smart Term Plan Plus

The Axis Max Life Smart Term Plan Plus is a flexible term insurance plan offering six variants. For most buyers, the Regular (Level Cover) and Smart Cover options stand out, making it a well-rounded and customizable choice for varied protection needs.

Axis Max Life

Smart Term Plan Plus

4.65

Overall Rating

Premium Rating

5.0/5

Insurer Rating

4.9/5

Feature Rating

4.1/5

Customer Service Rating

5.0/5

Features:

Accidental Death Benefit and Critical Illness Cover (up to 64 illnesses)

Regular or Smart Cover (1.5X coverage for first 15 years)

Waiver of Premium on Disability or Critical Illness

Terminal Illness Benefit (up to ₹1 crore)

Additional features like Zero-Cost Exit Option and Women's Perks (Lifeline Plus & Discounts)

An accelerated benefit of 2 Lakhs out of the base sum assured within 1 working day upon intimation of death( after waiting period of 1 policy year)

Annual Premiums Across Ages

Age/Sum Assured

₹1 Crore

₹2 Crore

25

₹10,459

₹18,400

30

₹13,185

₹22,556

35

₹17,223

₹28,506

40

₹22,920

₹38,760

45

₹30,112

₹55,620

Note: The listed premiums are for a non-smoker male (Coverage till age 70, without first year discounts)

02

HDFC Life Click 2 Protect Supreme Plus

HDFC Life Click 2 Protect Supreme Plus is a comprehensive term plan that offers a flexible Smart Exit benefit and cover increase options. It also gives all customers access to comprehensive health management services through the Life Rewards app.

HDFC Life

Click 2 Protect Supreme Plus

4.35

Overall Rating

Premium Rating

5.0/5

Insurer Rating

4.55/5

Feature Rating

4.46/5

Customer Service Rating

5.0/5

Features:

Terminal Illness Benefit (up to ₹ 2 crores) and optional Accidental Death Cover

Disability & Critical Illness Premium Waiver

Income benefit on Accidental Disability

Insta Payment on claim intimation

Critical Illness Cover (60 illnesses)

Life Stage Cover Increase

Annual Premiums Across Ages

Age/Sum Assured

₹1 Crore

₹2 Crore

25

₹12,148

₹23,075

30

₹15,033

₹29,514

35

₹21,140

₹39,916

40

₹26,865

₹51,484

45

₹35,298

₹67,235

Note: The listed premiums are for a non-smoker male (Coverage till age 70, without first year discounts)

03

ICICI Prudential iProtect Smart Plus

ICICI iProtect Smart Plus is a comprehensive term plan offering features like a Premium Break that lets you defer premiums for a year, Insta Payment with a ₹3 lakh advance payout on claim intimation, and the flexibility to switch from regular to limited pay after three years.

ICICI Prudential

iProtect Smart Plus

4.30

Overall Rating

Premium Rating

5.0/5

Insurer Rating

4.4/5

Feature Rating

3.8/5

Customer Service Rating

5.0/5

Features:

Accidental Death Benefit and Zero Cost Option

Life Stage Benefit (increased coverage after milestones like marriage/childbirth/home loan)

Terminal Illness Payout (Entire base cover)

Critical Illness Cover (60 illnesses)

Annual Premiums Across Ages

Age/Sum Assured

₹1 Crore

₹2 Crore

25

₹10,480

₹17,014

30

₹12,968

₹21,237

35

₹17,650

₹28,238

40

₹23,866

₹39,594

45

₹31,008

₹56,057

Note: The listed premiums are for a non-smoker male (Coverage till age 70, without first year discounts)

04

Bajaj Life eTouch II

Bajaj Life eTouch II is a strong term plan with useful riders, including a comprehensive 60-illness critical illness cover. It also stands out for affordable premiums, a good claim settlement record, and discounts for salaried and first-time buyers.

Bajaj Life

eTouch II

4.20

Overall Rating

Premium Rating

5.0/5

Insurer Rating

4.4/5

Feature Rating

3.4/5

Customer Service Rating

5.0/5

Features:

Accidental Death Benefit

Life Stage Benefit (increased coverage after marriage/childbirth)

Early Exit Option

Waiver of Premium on Accidental Total & Permanent Disability

Terminal Illness cover (up to ₹2cr)

An accelerated benefit of ₹2 Lakhs out of the base sum assured within 3 working days of claim registration( after waiting period of 1 policy year)

Annual Premiums Across Ages

Age/Sum Assured

₹1 Crore

₹2 Crore

25

₹10,020

₹16,105

30

₹12,630

₹20,717

35

₹16,070

₹26,953

40

₹21,907

₹36,951

45

₹32,386

₹54,384

Note: The listed premiums are for a non-smoker male (Coverage till age 70, without first year discounts)

05

Aditya Birla Sun Life Super Term Plan

Aditya Birla Super Term Plan offers multiple cover options, income-based payout choices, and optional riders. While premiums can be slightly higher for younger buyers, they are justified by the plan’s strong built-in features and long-term flexibility.

Aditya Birla Sun Life

Super Term Plan

4.0

Overall Rating

Premium Rating

5.0/5

Insurer Rating

3.7/5

Feature Rating

4.3/5

Customer Service Rating

5.0/5

Features:

Accelerated Critical Illness Benefit

Waiver of premium on Accidental Total & Permanent Disability

Life Stage Flexibility and Terminal Illness payout

Cover Continuance (premium deferment up to 12 months)

Early Exit Value (specific age/tenure bands)

Annual Premiums Across Ages

Age/Sum Assured

₹1 Crore

₹2 Crore

25

₹11,700

₹20,538

30

₹13,900

₹24,440

35

₹18,000

₹31,597

40

₹23,800

₹41,779

45

₹31,100

₹54,593

Note: The listed premiums are for a non-smoker male (Coverage till age 70, without first year discounts)

Learn more about these term plans and how we rate them.

What Are the Different Types of Term Insurance Riders?

Critical Illness Rider: In case you opt for this rider, you receive a lump sum payout upon diagnosis of a critical illness listed in the policy, which helps cover loss of income and medical expenses and preserves your savings.

Accidental Death Benefit Rider: With this rider, your family receivesan additional sum if you pass away due to an accident, over and above the base policy payout.

Waiver of Premium: Premium payments are waived in case of a covered risk, ensuring the policy remains active even if you're unable to pay.

Terminal Illness Cover: This benefit is often inbuilt. If you’re diagnosed with a terminal illness, a part of the cover is paid in advance. This helps you access funds early and plan expenses and family needs in time.

Total Permanent Disability Rider: If an accident leads to permanent disability, this rider gives a lump-sum payout. It helps manage income loss. It is helpful for individuals with high-risk jobs or those requiring additional protection.

Why Should You Buy Term Insurance?

Lower Premiums

Term life insurance offers more affordable premiums than other types of life insurance.

Higher Coverage

Term life insurance offers high coverage at a comparatively low premium.

Premium Stability and Flexibility

Premiums remain fixed throughout the term plan, and your premium payments are flexible. You get monthly, quarterly, half-yearly, or yearly premium payment options.

Tax Benefits

When a policyholder purchases a term policy, they receive a tax deduction on the premiums paid under section 80C and section 80D of the old regime, and payouts to beneficiaries are also tax-free.

Talk to an expert today and find the right insurance for you.

Who Should Buy Term Insurance?

Salaried Individuals: Ideal for protecting dependents against loss of regular income and covering liabilities like home loans.

Self-Employed Professionals: Helps secure family finances despite irregular income and business risks.

Married Individuals and Parents: Ensures your spouse, children, and dependents can manage living costs and future goals.

Young Earners and First-Time Buyers: Lock in low premiums early and build long-term financial protection at minimal cost.

Put simply: Individuals with dependents, loans, or financial responsibilities (current or potential future ones) should buy a term plan.

When Is the Right Time to Buy Term Insurance?

The ideal time to buy a term plan is when you start earning, preferably when you are in your 20s and early 30s. This is because the premium for a term plan is more affordable when you are younger, healthier, and relatively disease-free.

Delaying the decision to purchase a term plan can be costly. Premiums rise sharply with age, and health issues after 40 can further increase premium rates.

How Much Term Insurance Cover Should You Buy?

There’s no fixed-term cover that works for everyone. The right term insurance cover depends on your income, expenses, goals, and liabilities. A high cover (10-25x yearly income) should work if you are young.

For example, if your income is ₹10L/year, your ideal cover could range from ₹1 Cr to ₹2.5 Cr, depending on your family's needs, lifestyle, and liabilities.

At Ditto, we use the expense and liabilities replacement method to estimate the term cover you require. To get a better understanding, use thisonline calculator to find the ideal cover for you.

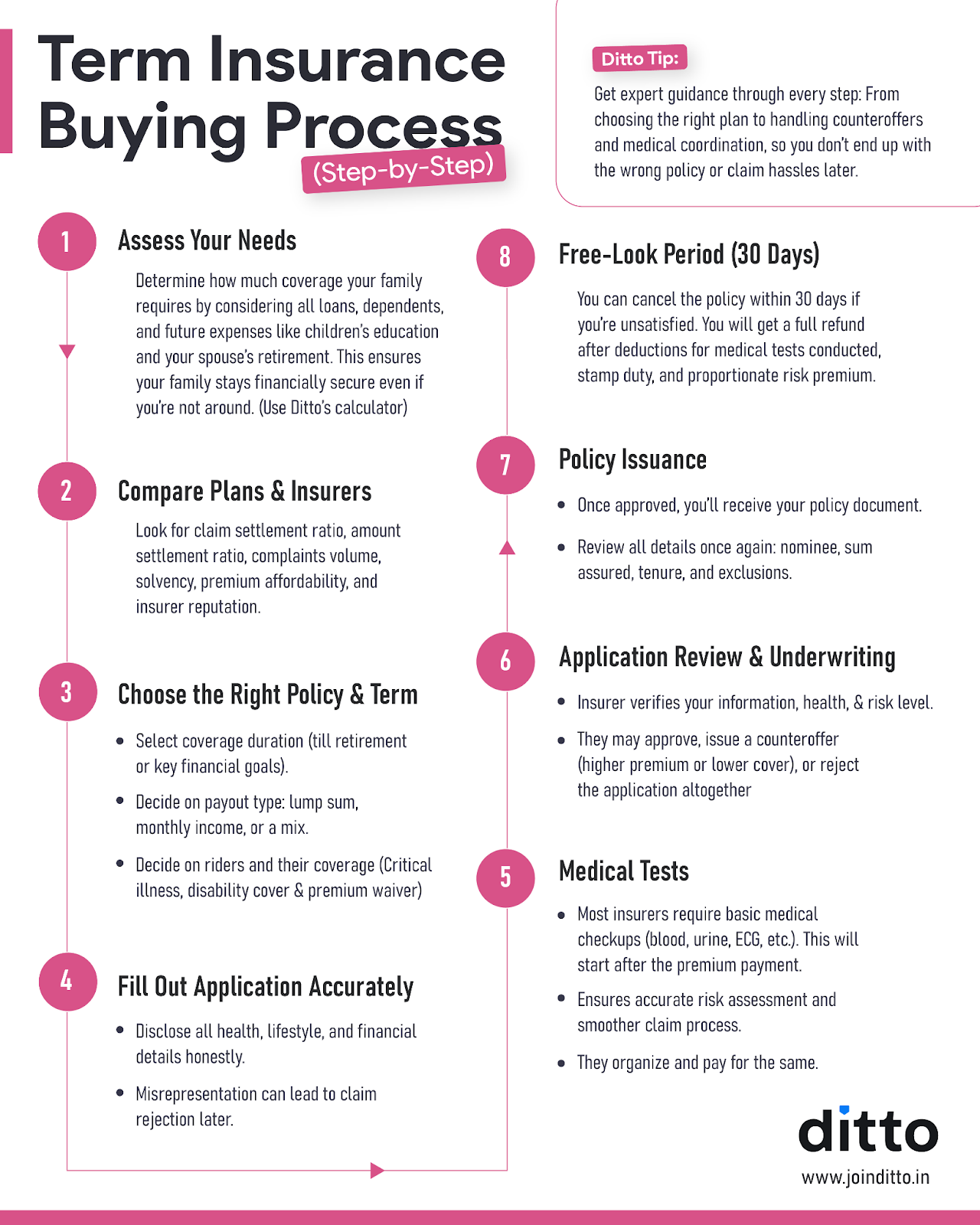

How to Buy Term Insurance Online?

Common Mistakes to Avoid While Buying Term Insurance

When buying term insurance, don’t focus only on keeping premiums low by picking a small cover.

Avoid delaying the purchase and skipping medical disclosures.

Do not get distracted by flashy add-ons like return of premium.

The cover should realistically match your income, loans, and your family’s future needs. Learn more about the common mistakes people usually make while purchasing a term plan.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why do customers like Vijay below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

Backed by Zerodha

Dedicated Claim Support Team

100% Free Consultation

Price Revision Alert: Leading insurers are revising term insurance premiums soon. Secure your family's financial safety net at today’s rates. Slots are filling up fast - Book a FREE consultation call or chat on WhatsApp with our experts.

Ditto’s Take on Term Insurance

Buying term insurance isn’t about finding a perfect plan. It’s about finding the right fit for your life. Income, health, liabilities, and family responsibilities vary for everyone, and these factors can change which plan works best.

Use this guide as a starting point, and if needed, a quick expert conversation can help tailor the choice to your budget and long-term goals.

At Ditto, we recommend term insurance as the most efficient way to protect your family. It gives you a large cover at a very low premium because it does not mix insurance with investment.

Frequently Asked Questions

How much does term insurance cost in India?

Term insurance is quite affordable. A healthy 25–30-year-old non-smoker can get a ₹1 crore cover starting around ₹800–1,000 per month. Premiums rise with age and health risks.

Can I buy term insurance without medical tests?

Yes, some insurers offer no-medical term plans, usually for lower sums assured. However, for higher cover amounts, medical tests are mandatory and help avoid claim issues later. We encourage people to get them done if the insurer asks.

Can I have multiple term insurance policies?

Yes. You can hold multiple term plans from the same or different insurers, as long as the total cover is justified by your income and disclosed honestly during purchase.

What are the basic income requirements for term insurance?

Insurers usually want a minimum income of ₹3-5 lakh for applicants. Self-employed individuals must show at least two years of ITRs to prove a stable income.

Can I buy a term plan if I currently don’t have any source of income?

No, you cannot buy a term insurance plan without an active source of income. Term insurance is designed to replace the policyholder’s income, so insurers require proof of earnings.

Customer Reviews

4.9

20915 reviews

Ditto is doing really great. Absolutely spam free- that's the best part. They don't talk to you like they are forced to sell the product. It's more like, helping us buy better. Advisor Nuha was very patient and answered all my questions with clarity. Thanks for the service

I

INDHUMATHI M

Loved the service! Maheta Nidhi Hitesh was incredibly helpful and knowledgeable. She guided me through the whole process and made everything super easy to understand. I really appreciated how patient she was with all my questions—there was no pressure at all, just clear and honest advice. Honestly, I'm very happy with my experience at Ditto so far. Highly recommend!

RK

Ragul Kumar

I had a great experience with Ditto while exploring health insurance options. The process was smooth and everything was explained clearly.

A special thanks to Swaroop SK for patiently answering all my questions and guiding me through the policy details without any pressure. The transparency and support made it much easier to understand and choose the right plan.

Really appreciate the assistance!

PS

Pulkit Singh

Had a great experience with Ditto Insurance. Ishita Sudrania was extremely helpful in guiding me through choosing the right term plan. There was no spamming or sales pressure, and all my questions were patiently answered. She also assisted me thoroughly with the entire application process. Highly recommend!

SS

Samil Shah

I had a great experience with Ditto while filing my health insurance claim. Their team guided me clearly through the entire process, helped with the required documents, and promptly answered all my queries. Their support made the claim process much smoother and less stressful. Highly appreciate their assistance.