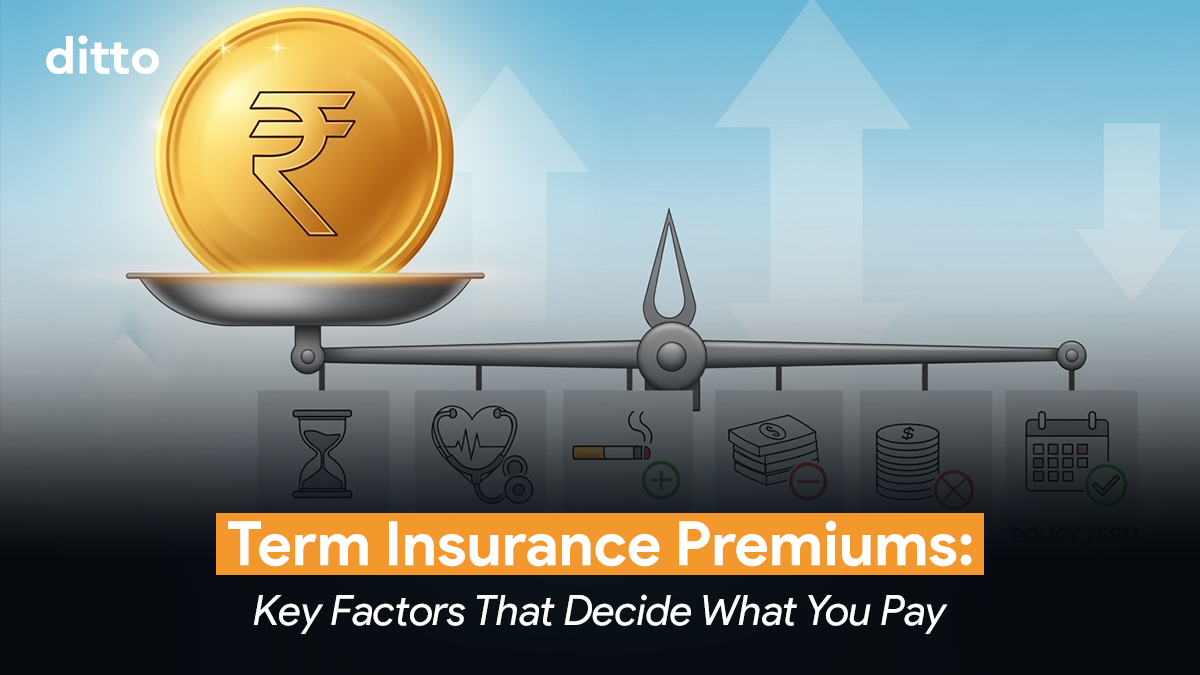

Two 30-year-olds can buy the same ₹1 Cr term plan, but one may pay ₹1,070/month while the other pays ₹1,281. Why?

Term insurance premiums may seem random at first glance, but they’re anything but. Insurers rely on medical, lifestyle, and financial data to price your policy, and even a minor detail can raise or lower your premium significantly.

At Ditto, we’ve advised over 3,00,000 people on their term insurance journey, and we’ve seen premiums vary widely based on seemingly small inputs. To write this piece, we analyzed proposal forms, underwriting guidelines from five leading insurers, and real quotes issued to Ditto users between April and July 2025.

By the end, you’ll know which factors genuinely impact your premium and which ones aren’t worth stressing over.

1. Age

Age is the most influential variable. The younger you are, the lower the premium. This is because at 25, you're statistically far less likely to develop life-threatening conditions or die unexpectedly than at 45. So the insurer takes on less risk and rewards you with a lower premium.

Here’s how your age affects premiums for a real term plan: ICICI Prudential iProtect Smart Plus. The table below shows premiums for a ₹1 Cr cover (non-smoker male, healthy, coverage till age 60 & without any discounts) at different entry ages.

| Entry Age | ₹1 Crore Term Premiums |

|---|---|

| 20 years old | ₹9,648 |

| 25 years old | ₹10,853 |

| 30 years old | ₹12,683 |

| 35 years old | ₹16,382 |

| 40 years old | ₹22,290 |

| 45 years old | ₹28,821 |

2. Medical conditions

Term insurance is priced around one question: how likely are you to die during the policy term?

If your medical reports show signs of existing conditions, even if controlled, insurers see you as a higher-risk applicant. And to balance that risk, they increase your premium.

Also, remember: the quote you see online is just a starting point. Before finalising your policy, insurers run a full set of medical tests. If anything looks off, they may “load” your premium, i.e., bump it up based on their risk assessment. Here's how it usually plays out:

- Lipid profile abnormalities (high cholesterol/triglycerides)

Can lead to a 25–100% increase in premium or restrictions on coverage/term. - Type 2 Diabetes

Even if well-managed, it often results in a 50–100% loading charge or restrictions on coverage/term and riders offered. - Other pre-existing conditions (e.g., asthma, thyroid disease, hypertension, etc.)

Loadings vary. Some cases see a small hike, others face exclusions, and sometimes, outright rejection. - Family Medical History: A history of hereditary illnesses, particularly those with early onset (e.g., familial cancer, early heart attacks), may impact underwriting decisions and premium costs, even if the applicant is currently healthy.

We’ve seen normal-looking reports still result in loadings. A mild ECG variation during a treadmill test, for instance, might not bother your doctor, but insurers may treat it as elevated cardiac risk and bump up your premium.

At Ditto, we have seen cases where the insurer decides to impose loading charges on Critical illness benefit and waiver of premium rider premiums depending on the parents' history of heart ailments, cancers.

| Did you know Can your premiums increase by more than 100% due to medical history? Generally, no. When the risk is too high, insurers don’t load your premium endlessly; they typically postpone or reject the application altogether. |

3. Occupation and lifestyle

Insurers don’t just assess your health. They also look at how risky your day-to-day life is. This includes both your profession and your hobbies.

- High-risk jobs (like pilots, marine engineers, oil rig workers, armed forces, etc.) often face significant loadings.At Ditto, we’ve seen pilots and marine engineers receive counteroffers with 100% loadings, doubling their quoted premium.

- Adventure sports, such as skydiving, scuba diving, mountaineering, or even regular high-altitude trekking, can also trigger loadings or exclusions, especially if disclosed as part of your lifestyle.

In both cases, insurers apply internal risk filters, and the resulting load can vary from 25% to 100%, depending on how frequent or hazardous the activity is.

Summary: If your work or hobbies involve physical risk, your premium won’t stay standard, and insurers will charge for the added exposure.

4. Smoking and substance use

If you smoke or use tobacco, your term insurance premium will automatically increase by 60%-100%, even if you’re otherwise fit and healthy.

Insurers don’t just rely on your declaration either. Most run medical tests, such as urine cotinine and serum cotinine, to detect nicotine traces. Even occasional or social smoking can get you tagged as a smoker if you’ve used tobacco in the last 12–36 months.

- Once tagged, you're treated as a smoker, and your premium reflects that risk.

- Marijuana or narcotics use? There’s no loading. Instead, your application is outright rejected.

Apart from smoking, another factor that increases your insurance premium is alcohol consumption.

While moderate social drinking may not significantly affect premiums, heavy or habitual alcohol use is a red flag during underwriting. Excessive alcohol intake is associated with higher mortality risks due to liver disease, cardiovascular issues, and accident-related fatalities. And applicants may be asked to disclose the frequency and quantity of alcohol consumption, and in some cases, liver function tests may be used to assess the long-term impact.

We’ve seen cases where applicants didn’t disclose occasional smoking, tested positive on cotinine, and the application was rejected for non-disclosure.

Summary: Smoking always leads to a higher premium. And in the case of drug use, there’s no negotiation; insurers reject the application altogether.

5. The cover amount you choose

The higher the sum assured you pick, the more your premium goes up. But here’s the catch: it doesn’t rise in exact proportion.

So if you go from ₹1 Cr to ₹2 Cr cover, your premium won’t necessarily double. It might go up by 70–90%, because the insurer saves on admin costs and gives you a bit of a volume discount.

Here’s a table illustrating premiums on HDFC Life Click 2 Protect Supreme for a 32-year-old healthy non-smoker (38-year term) without discounts.

| Cover Amount | Annual Premium (₹) | What Changes |

|---|---|---|

| ₹50 lakh | ₹13,595 | Base rate |

| ₹1 crore | ₹20,950 | ×2 cover ≠ ×2 premium |

| ₹2 crore | ₹36,359 | ×4 cover ≠ ×4 premium |

| ₹3 crore | ₹51,482 | X6 cover ≠ x6 premium |

Summary: More cover = more premium. But thanks to volume discounts (economies of scale), doubling your cover doesn’t double your premium. You get better value per rupee of cover when you opt for higher sums assured.

6. Policy tenure:

The longer you're covered, the more your term policy will cost, especially in your older years

When you buy a term plan, you’re asking the insurer to take on the risk of your death during a certain period. And the older your exit age is, the higher that risk.

So while covering yourself till age 60 means the insurer is only taking on the risk during your working years, extending it to age 70 or 80 means they’re covering you when the probability of death climbs steeply.

Apart from this, if you extend your cover beyond the average life expectancy in your country, there will be a steep jump in your premiums.

That’s why premiums jump, not just linearly, but disproportionately with longer tenures.

Annual Premiums, Axis Max Life Smart Term Plan Plus, ₹1 Crore cover

For a 30-year-old, healthy, non-smoking male, without discounts-

| Policy End Age | Policy Term | Annual Premium (₹) | % Increase over Age 60 |

|---|---|---|---|

| 60 | 30 years | ₹12,161 | - |

| 65 | 35 years | ₹14,086 | 15.80% |

| 70 | 40 years | ₹15,558 | 27.90% |

| 75 | 45 years | ₹17,549 | 44.30% |

| 80 | 50 years | ₹19,677 | 61.80% |

| 85 | 55 years | ₹21,502 | 76.80% |

Summary: Extending your policy beyond age 60 means you’re buying protection into high-risk decades, and your premium will reflect that. Anything above 70 years means you are paying really steep premiums.

| Point of Interest If you add riders or add-ons like critical illness benefit, waiver of premiums, accidental death/disability benefit, etc, your premiums will be higher on account of these extra benefits. And some may even have duration restrictions, meaning the coverage from riders may finish much earlier than your base term plan. |

7. Gender:

Women typically pay 10–15% lower premiums than men. And this difference is rooted in actuarial science.

Women, on average, have longer life expectancies than men. That means insurers statistically expect women to outlive men, making them a slightly lower risk to insure over the same term. Over the span of a 30- or 40-year policy, that difference can add up to significant savings.

8. Premium Payment Term (PPT)

The Premium Payment Term (PPT) is the duration over which you pay premiums. In most cases, it is the same as your policy duration. This is called regular pay. However, it can be shorter than your policy term, too.

For instance, you can pay for the first 10 or 15 years of your policy term and still be covered for your entire term duration. This is called limited pay, and it comes with one major advantage.

The total premiums you pay over the lifetime of the policy will be lower than a regular payment option. You will have to pay a slightly higher premium per annum, but the overall premium you pay will still be lower (ignoring inflation & time value of money).

Conclusion

Your term insurance premium is calculated after taking into account the risk you present, not just your age. Your health, habits, lifestyle, and the amount of coverage you request also play a role. Some factors, like your age or smoking status, have an outsized impact. Others, such as riders or policy terms, offer flexibility but at a cost.

If you want to optimise your premium without compromising on protection, start early, be transparent during medicals, and pick only what you truly need.

Still unsure what combination works best for you? Chat with a Ditto advisor. We’ll help you find the right cover at the right price.

Last updated on: