Quick Overview

Aviva Life Insurance Company India Limited is a private life insurer established in 2002 as a joint venture between Aviva plc and the Dabur Group. Headquartered in Gurugram, the company offers term insurance, ULIPs, savings plans, retirement solutions, and child plans. Aviva Life operates through a mix of direct sales, bancassurance partnerships, and an advisor-led distribution network across India.

Its ULIP portfolio is designed for customers looking to combine long-term wealth creation with life insurance, offering multiple fund options and flexibility in premium payments and policy terms.

This guide explains how Aviva Life Insurance ULIP plans work and the insurer’s key performance metrics.

Aviva Life Insurance: Performance Metrics

Note: These metrics are for the entire life insurance portfolio of Aviva Life Insurance, and not just for their ULIPs.

Insights:

- CSR is marginally above the industry average, indicating a strong and consistent claim approval track record.

- ASR is significantly higher than the industry average, suggesting Aviva Life is more likely to pay the full claim amount irrespective of claim size.

- Average complaints are substantially higher than the industry median, which may point to a higher incidence of customer grievances during the claims process.

- Annual business volumes are considerably lower than the industry median, reflecting a relatively smaller market share and scale.

- Solvency ratio is below the industry median, though still above the regulatory requirement, indicating adequate, but comparatively lower, capital buffers to meet future obligations.

Popular ULIP Plans Offered by Aviva Life Insurance

Premiums for Aviva Life Insurance ULIP Plans

Note: Projected values are illustrative for a 40-year-old. Actual returns are not guaranteed and will depend on market performance. The figures are extracted from the Aviva Life Signature Investment ULIP brochure, where you will find more Aviva Life Insurance policy details.

Drawbacks of Buying an Aviva Life Insurance ULIP Plan

Multiple Charges Reduce Effective Returns

Aviva ULIPs include charges like policy administration, mortality, and fund management fees. Even if some plans offer partial charge refunds, these costs are deducted during the policy term and can impact long-term compounding.

Life Cover is Often Insufficient

ULIPs typically offer life cover of around 10 times the annual premium, which is usually not enough to financially protect dependents.

Five-year Lock-in Limits Liquidity

All ULIPs have a mandatory 5-year lock-in period, during which withdrawals are restricted. This reduces flexibility if you need access to funds early.

Market Risk with Limited Investment Flexibility

Returns are market-linked and not guaranteed. While fund switching is allowed, investment choices are limited to the insurer’s available funds.

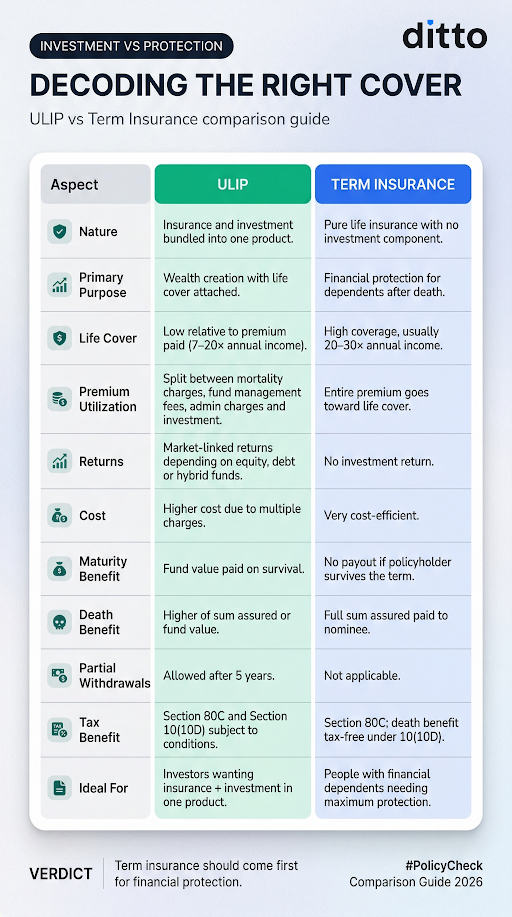

ULIP vs Term Insurance: Which is Better?

If you’re trying to decide between ULIPs and term insurance, it helps to first understand how they differ in purpose, cost, and outcomes. We’ve broken this down in detail here:

In short, the choice comes down to whether you prefer a bundled product or want to optimize protection and returns by keeping insurance and investments separate. For a detailed breakdown, check out our guide on ULIPs vs term insurance.

Numerical Illustration Based on Aviva ULIP Plans

Let’s take an example. Consider a 40-year-old individual investing ₹20,000 per month (₹2,40,000 annually) for 20 years to build a retirement corpus while also ensuring financial protection.

Option A: Aviva ULIP (Signature Investment Plan)

Note: In this article, P.A. refers to per annum.

Option B: Term Insurance + Direct Mutual Fund Systematic Investment Plan (SIP)

Corpus range reflects beginning-of-year vs. end-of-year SIP timing. Even at the conservative end, it significantly outpaces the ULIP.

The Difference

Check out the infographic below to understand the difference between a term insurance policy and ULIP.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Vijay below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat on WhatsApp now!

Conclusion

Aviva Life ULIPs offer a structured way to combine investing and insurance, with features like fund flexibility and cost efficiencies in select plans. However, these come with trade-offs, lower life cover, and multiple charges that can impact long-term returns.

At Ditto, we don’t recommend ULIPs since bundling insurance and investment often leads to compromises on both fronts. A term plan + SIP typically offers better protection and more efficient returns.

While Aviva has been around since 2002, it operates at a relatively smaller scale with lower market presence, offering fewer clear advantages versus larger insurers, especially given the inherent limitations of ULIPs.

Frequently Asked Questions

Last updated on: