When purchasing a health insurance policy, you must check numerous factors such as waiting periods, exclusions, daycare treatments, etc. However, two of them probably convey the essence of the policy — Inpatient Care (IPD) and Outpatient Care (OPD). After all, health insurance was historically designed to cover only hospitalisations.

Whether you’re undergoing surgery or visiting a specialist for a consultation, knowing the specifics of IPD and OPD can help you when making a claim with your health insurance policy.

Difference between Inpatient (IPD) & Outpatient Care (OPD) in Health Insurance

Before we get into the specifics of inpatient and outpatient care, here is a summary of what they entail.

| Basis | Inpatient Hospitalisation (IPD) | Outpatient Hospitalisation (OPD) |

|---|---|---|

| Meaning | When you require an overnight or more extended period of hospitalisation | When you require medical treatment involving short-term hospitalisation (not overnight) or doctor consultations. |

| Cost | Considering the complexity of treatments and procedures you may require, expensive charges are involved. | Nominal charges are incurred since no long-term treatments/hospitalisation is involved. |

| Availability | Included in all health insurance policies, whether private or government. | It is included only in some health insurance plans as an in-built feature or as an add-on. |

Heads Up: It takes an average person up to 5 hours to read & analyse a policy and 10 hours or more to compare different plans and make a decision.

This is why we propose a better alternative - taking a 30-minute FREE consultation with Ditto’s certified advisors. We have a spam-free guarantee, and we’ll never push you to buy a plan. Don’t delay this - we have limited slots every day, so book a quick call here before they run out.

What is Inpatient Hospitalisation (IPD) in Health Insurance?

Any medical treatment or procedure that requires you to stay in the hospital for at least 24 hours is called inpatient hospitalisation. This is usually more intensive than regular doctor consultations or hospital visits and may involve complex treatments or surgeries.

Health insurance policies usually cover a wide range of expenses for inpatient hospitalisation, including room rent, nursing fees, doctor’s fees, surgery costs, and post-operative care. However, coverage for inpatient hospitalisation can also vary based on the type of hospitalisation. Let’s take a look at this in detail.

What are the Types & Coverage for Inpatient Hospitalisation?

There are two main types of inpatient hospitalisations, based on which coverage differs –

- Emergency Hospitalisation: This occurs when a patient requires immediate medical attention due to a sudden illness or injury. In case of emergency hospitalisation, you must inform the insurer within 24 hours of getting admitted. Once you do this, the insurer will either approve a limit up to which you can claim in a cashless manner or let you know that you need to pay the entire amount first and then file for a reimbursement claim.

- Planned Hospitalisation: This involves medical procedures or surgeries that were scheduled beforehand, such as joint replacements or planned deliveries. This is also called an Elective Procedure Hospitalisation. In case of a planned hospitalisation, you need to inform the insurer at least 48 hours in advance. The insurer then pre-approves an amount for cashless claims or lets you know that the procedure or the facility is unavailable for cashless treatments.

Let’s understand this with the help of an example.

Riya purchased an excellent health insurance plan a few years ago. Suddenly, one night, she experiences severe abdominal pain and rushes to the hospital. Unfortunately, she is diagnosed with appendicitis.

Since this was an emergency hospitalisation, Riya's family informed the insurance provider within a few minutes of her admission. The insurer approved a limit for her cashless treatment, covering the surgery and hospital expenses up to a certain amount. Due to this, Riya didn’t have to worry about hospitalisation expenses and focussed entirely on her recovery.

Now, let's say that she also needs knee replacement surgery a few years later. This will fall under planned hospitalisation. So, Riya should inform her insurer 48 hours before the scheduled surgery, and the insurer pre-approves a cashless claim amount for the hospital where the surgery is set to take place. However, if the hospital isn’t part of the insurer’s network, Riya must pay upfront and file for reimbursement later.

Now that we have understood what in-patient hospitalisation is, let’s take a look at out-patient hospitalisation.

What is Outpatient Hospitalisation (OPD) in Health Insurance?

Outpatient hospitalisation, also known as OPD (Outpatient Department) services, is the medical treatments or consultations that do not require an overnight stay in the hospital. Patients visit the hospital or clinic, receive treatment within a few minutes or hours, and leave on the same day.

What is the Coverage for Outpatient Hospitalisation?

While all health insurance policies cover in-patient hospitalisation, only a few provide out-patient coverage. OPD coverage usually includes consultations with specialists, diagnostic tests or scans, and other minor procedures.

It is also important to remember that insurers often have restrictions on this, too. To make the claim, you can only go to specified doctors at specified clinics, hospitals, and diagnostic centres. Apart from this, there may be a per-visit limit on the amount the insurers pay out—for instance, let’s say your consultation costed ₹ 900. If the insurer has a limit of, say, Rs 500, they will pay only up to this amount.

What are the Essential Features of Inpatient Hospitalisation in Health Insurance?

While each policy has its own benefits and drawbacks, It’s important to consider these factors while purchasing a good health insurance plan:

- No Room Rent Limits: Ensure your policy does not restrict the type of room you can choose during hospitalisation, as room rent limits can lead to higher out-of-pocket expenses. You can take a look at this article for more information.

- No Disease-wise Sub-limits: Check that your policy does not impose sub-limits on specific diseases or treatments, ensuring comprehensive coverage for all medical needs.

- No Copayment: Opt for a policy without copayment requirements, so you do not have to bear a percentage of the hospitalisation costs out of pocket.

Why Talk to Ditto for Your Health Insurance?

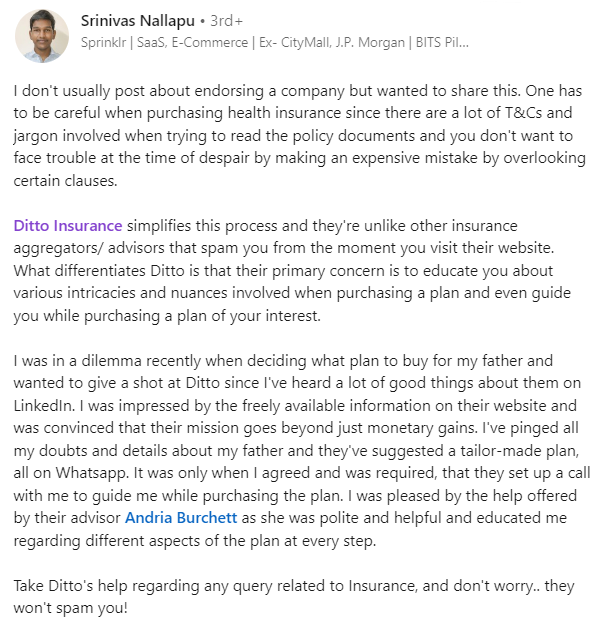

At Ditto, we’ve assisted over 3,00,000 customers with choosing the right insurance policy. Why customers like Srinivas below love us:

✅No-Spam & No Salesmen

✅Rated 4.9/5 on Google Reviews by 5,000+ happy customers

✅Backed by Zerodha

✅100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now!

Conclusion

Inpatient and outpatient services have two distinct roles in healthcare. Together, they ensure comprehensive health insurance coverage for you and your family.

When choosing any health insurance policy, it's also important to evaluate your specific healthcare needs and financial situation. For personalised, spam-free insurance advice, consider booking a call with Ditto Insurance’s IRDAI-certified experts to find the best plan for your requirements.

Last updated on