A deductible in insurance is the specific amount you pay out of pocket before your insurer starts covering your claim. It serves as a cost-sharing mechanism and is most commonly found in indemnity-based policies, such as health insurance and motor insurance. A deductible is designed to lower premiums in exchange for taking on more immediate risk.

For example, a 30-year-old in Delhi with a ₹15 lakh HDFC ERGO Optima Secure+ plan pays ₹14,248 per year with a zero deductible. Opting for a ₹50,000 aggregate deductible brings that down to ₹8,549, but this means paying the first ₹50,000 of any hospital bill out of pocket before the insurer steps in.

This guide explains how deductibles work before you choose or renew a health insurance plan.

You just got a hospital bill for ₹1 lakh, but since you have a health insurance plan, you think there is nothing to worry about. But the insurer only pays ₹75,000, and the rest comes out of your pocket. Why? Because your plan had a ₹25,000 deductible.

That is the part most people miss when buying health insurance. The premium grabs your attention. But the deductible does not. And that is exactly where confusion shows up at claim time.

In this guide, you will learn what is deductible in health insurance, the types available, how they change your premium, and whether you should opt for one.

According to the Insurance Regulatory and Development Authority of India (IRDAI), a deductible is a specified amount stated in the policy, up to which an insurer will not pay any claim, and it will be deducted from the total claim amount (if the claim amount exceeds the specified amount).

Put simply: you pay a specific initial amount first, and the insurer pays the remaining amount later.

One important thing to note is that a deductible does not reduce your sum insured. Your ₹15 lakh cover stays the same regardless of the deductible.

Did You Know?

Life insurance does not have deductibles because they operate on a different principle from health insurance. Health insurance is indemnity-based, meaning your insurer pays you back for the actual cost of treatment. Whereas life insurance is benefit-based, meaning your insurer pays a fixed lump sum to your nominee when a specific event occurs, like death. There is no bill to split, so there is no reason for a deductible.

Types of Deductibles in Health Insurance

Type of Deductible

Application

Examples

Compulsory Deductible

A fixed deductible is built into your health policy by the insurer and cannot be modified or removed. It applies automatically every time a claim is made. Commonly seen in top-ups and super top-ups.

HDFC ERGO Medisure Super top-up has a compulsory deductible of ₹4 lakh and a compulsory sum insured (SI) of ₹ 5 lakh, with SI ranging from ₹5 lakh to ₹20 lakh.

Voluntary Deductible

A deductible that you opt to reduce your health premium. The higher the voluntary deductible you select, the lower your premium becomes.

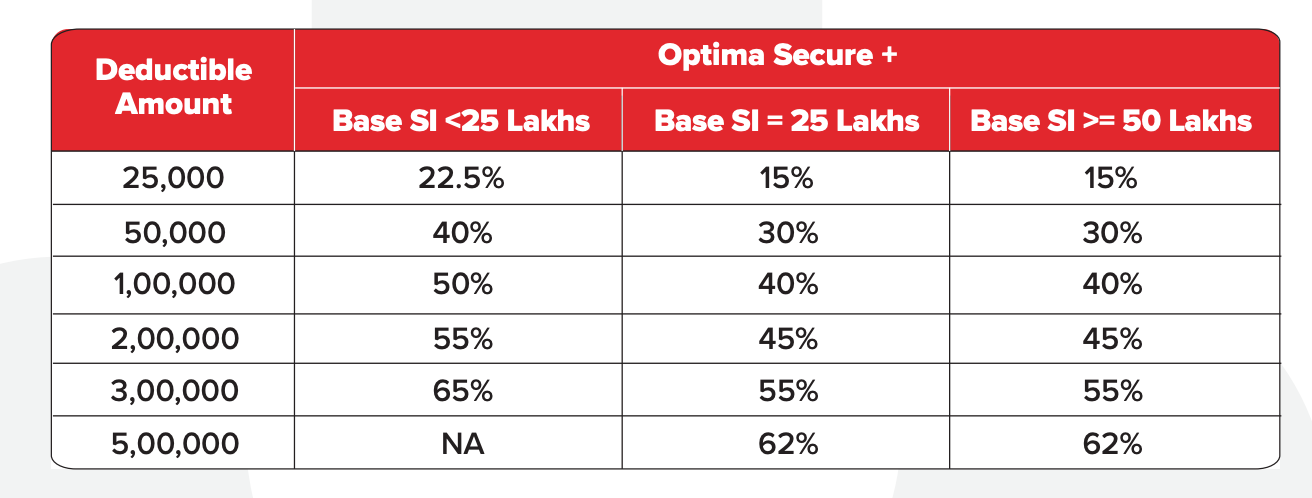

HDFC ERGO’s Optima Secure+ plan offers the option to add a voluntary deductible ranging from ₹25,000 to ₹5 lakh (in exchange for discounts ranging from 15% to 65%).

Aggregate Deductible

Applies to the total medical expenses you incur over the entire policy year. All your medical bills for the year are added together, and if the combined total exceeds the deductible, the insurer pays the remaining amount.

Applies separately to every hospitalization expense. If the per-claim deductible is ₹10,000, you must pay ₹10,000 each time you file a claim, regardless of the number of times you get hospitalized.

The relationship between deductibles and premiums is straightforward: a higher deductible means a lower premium. And a lower deductible means a higher premium. When you agree to take on more risk (by paying a larger chunk of each claim), the insurer takes on less risk. They reward this by charging you less upfront.

Here’s a snippet of the voluntary aggregate deductible offered by HDFC Optima Secure+, where you get up to 65% discount on your premium:

Let’s see how having a deductible affects your claim in different scenarios:

Cashless Claims: In a cashless claim, the insurer authorizes the admissible claim amount in accordance with the policy terms. You still need to pay the deductible, copay, non-payable items, and any amount outside policy limits to the hospital. For example, on a ₹15 lakh bill with a ₹5 lakh deductible, you pay ₹5 lakh, and the insurer settles the remaining ₹10 lakh on a cashless basis.

Reimbursement Claims: You pay the full bill initially. The insurer reimburses only the portion above the deductible. This applies to all deductible types, whether compulsory, voluntary, per-claim, or aggregate.

With Corporate Health Insurance: If you have employer health insurance along with a super top-up, the employer or base policy pays first. That claim amount helps meet the deductible, after which the super top-up covers the remaining expenses, if policy terms and policy years align.

CTA

Annual Premiums with Deductible

Deductible

Annual Premium

Insight

₹0

₹14,248

Full coverage from the first rupee. No out-of-pocket cost at claim time

₹25,000

₹11,042

Saves ₹3,206 per year. But one hospitalization costs you ₹25,000 upfront. You need almost 8 claim-free years just to break even on a single claim

₹50,000

₹8,549

Saves ₹5,699 per year. Sounds good until you claim once and pay ₹50,000. That wipes out nearly 9 years of premium savings in one visit

₹1 lakh

₹7,124

Saves ₹7,124 per year. But one claim costs ₹1 lakh out of pocket. You'd need 14 consecutive claim-free years to make this worthwhile

₹2 lakh

₹6,411

Saves ₹7,837 per year vs no deductible. One claim hits you with ₹2 lakh instantly. That is 25+ years of savings gone in a single hospitalization

Note: The premiums above are calculated for a ₹15 lakh sum insured for a healthy 30-year-old residing in Delhi (pincode: 110010) under the HDFC ERGO Optima Secure+ plan. Numbers are indicative and may vary based on age, location, medical history, and selected add-ons.

The deductible is not a savings tool. It only works in your favor if you never claim, or claim very rarely over a long period. For anyone with a family history of illness, a chronic condition, or parents on the policy, the math turns against you quickly.

Should You Choose a Deductible in Your Health Insurance Plan?

A Voluntary Deductible Makes Sense if You:

Are young, healthy, and rarely visit a hospital

Have enough savings to cover the deductible in an emergency for years to come

Have an existing policy / corporate health coverage to meet the threshold

Want to reduce your annual premium without sacrificing your core coverage

Skip the Voluntary Deductible if You:

Have a pre-existing condition or visit doctors frequently

Are covering senior parents who are more likely to claim

Do not have the deductible amount readily available in case of hospitalization

Are buying a base health plan as your primary cover

Bottom Line: Do not choose a deductible amount you cannot afford to pay in an emergency. The premium savings mean nothing if a sudden hospitalization leaves you scrambling for cash.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

A deductible in insurance is the amount you pay out of pocket before your insurer covers the remaining claim. In India, deductibles fall into two main types: compulsory (set by the insurer, non-negotiable) and voluntary (your choice, with premium savings). Higher deductibles reduce your premium but increase your out-of-pocket costs at the time of claim.

Bottom Line: At Ditto, we usually avoid recommending deductible-based plans. For most people, choosing a deductible on a basic health plan makes sense only if there is a strong fallback coverage (such as employer insurance) to absorb initial costs. They also help if you have a solid emergency fund to handle out-of-pocket expenses, and you’re confident that hospitalizations will not be frequent.

If you are looking for health plans from insurers with established track records, we recommend the best health insurance plans in India that align with your long-term goals.

Frequently Asked Questions

What is a deductible in insurance?

A deductible in insurance is the fixed amount you pay out of pocket before your insurer starts covering your claim. According to IRDAI, it is a specified amount stated in the policy up to which the insurer will not pay any claim. Think of it this way: if you have a ₹50,000 deductible and file a ₹1 lakh claim, you pay ₹50,000 first, and the insurer covers the remaining ₹50,000. It applies most commonly in health and motor insurance, not in term or life insurance.

Does a deductible reduce my sum insured in health insurance?

No, a deductible does not reduce your sum insured. Your full coverage amount stays intact regardless of the deductible you choose. If you have a ₹15 lakh health plan with a ₹50,000 deductible, your sum insured remains ₹15 lakh. The deductible only determines how much risk you are willing to take with the insurer. You pay the deductible amount upfront at the time of a claim, and the insurer covers everything above it, up to your sum insured limit.

What is the difference between compulsory and voluntary deductibles in health insurance?

A compulsory deductible is built into the policy and applies as per the policy wording, either per claim, per policy year, or both. For example, super top-ups have a mandatory aggregate deductible to be paid before the first claim of the year. A voluntary deductible, on the other hand, is something you opt for to reduce your annual premium. The higher the voluntary deductible you choose, the lower your premium. For example, HDFC Optima Secure+ offers voluntary aggregate deductibles ranging from ₹25,000 to ₹5 lakh, with premium discounts of up to 65%.

What is an aggregate deductible in health insurance?

An aggregate deductible applies to your total medical expenses across the entire policy year, not to each individual hospitalization. All your medical bills are added together, and the insurer steps in only after your cumulative expenses cross the deductible threshold. This type of deductible is most commonly seen in super top-up health insurance plans. It is generally more favorable than a per-claim deductible if you have multiple hospitalizations in a single year because you only need to meet the deductible once.

Is choosing a higher voluntary deductible always worth the premium savings?

Not necessarily, and at Ditto, we recommend being careful about this trade-off. Premium savings scale slowly, but your out-of-pocket risk jumps significantly. For a 30-year-old, going from no deductible to a ₹2 lakh deductible on a ₹15 lakh plan saves you just ₹7,837 per year. But one hospitalization wipes out over 25 years of those savings in a single visit. A high deductible only makes financial sense if you rarely claim, are young and healthy, and have enough savings to cover the deductible in an emergency.

Is it better to opt for a deductible or just buy a higher sum insured?

Most people treat a deductible purely as a way to cut their premiums. For a 30-year-old in Delhi, a ₹1 lakh deductible saves roughly ₹7,000 per year compared to a zero-deductible plan. In many cases, that same ₹7,000 can get you meaningfully closer to upgrading from a ₹15 lakh plan to a higher coverage plan. A higher sum insured provides better protection in the event of a serious claim. A deductible just shifts risk back to you. At Ditto, we recommend buying more coverage rather than cutting your premium with a higher deductible.

What happens if my hospital bill is less than my deductible?

If your hospital bill is lower than your deductible amount, your insurer pays nothing, and you bear the entire cost yourself. For example, if you have a ₹50,000 deductible and your bill comes to ₹35,000, the insurer contributes nothing. This is one of the most overlooked downsides of choosing a high voluntary deductible. At Ditto, we always remind people that smaller, more frequent hospitalizations can go completely uncovered when a large deductible is in place, making the premium savings feel far less worthwhile.

What is the difference between a deductible and a copayment in health insurance?

A deductible is a fixed rupee amount you pay before your insurer covers anything. A copayment is a percentage of every claim you share with the insurer each time you claim. A 20% copay on a ₹1 lakh bill means you pay ₹20,000 every single time you are hospitalized. A deductible applies once per claim or once per year. If your plan gives you a choice between the two, we recommend choosing the deductible at Ditto. A fixed amount is something you can plan for. A percentage-based liability grows with every bill and is much harder to predict.

Do deductibles reset every year in health insurance?

Yes, deductibles in health insurance typically reset at the start of every new policy year. This means that even if you met your aggregate deductible in the previous policy year, you start from zero again when your policy renews. For per-claim deductibles, the reset happens with every new hospitalization, regardless of the policy year. This annual reset is an important factor to consider when evaluating whether a high deductible makes financial sense for you, especially if you anticipate multiple hospitalizations across different policy years.

What is a deductible waiver in health insurance?

A deductible waiver lets you remove or reduce your voluntary deductible after meeting certain conditions, giving you full coverage going forward. HDFC ERGO Optima Secure+ offers this, but with specific rules. You must be under 50 years old when you first buy the plan with the aggregate deductible. After 5 continuous policy years, and provided the eldest insured person is under 61 at that point, you can apply to reduce or fully waive the deductible at renewal. This option is available only once in the lifetime of the policy, applies to all insured members together, and your premium gets revised accordingly.

Last updated on:

Need a human touch?

Our advisors are here to help you pick the right plan.

Our advisors are here to help you pick the right plan.