What are the time limits of health insurance claims in India?

Filing a health insurance claim in India? Timing plays a crucial role. Knowing the exact time limits for cashless and reimbursement claims can help avoid unnecessary delays or rejections. Regardless of whether it's an emergency admission or a planned procedure, IRDAI has set clear timelines for insurers to follow.

In this guide, we'll walk you through these deadlines, required documents, and penalties insurers face for delays so you can get your health claim without any hassle.

Did You Know?

What is the time limit for cashless claims?

Cashless claims allow you to get treated at a network hospital without paying out of pocket; the insurer settles the bill directly. However, to use this facility smoothly, it’s essential to inform the insurance company within specific timelines.

- For emergency hospitalization, you must notify the insurer within 24 to 48 hours of admission, or before discharge, whichever comes first.

- The insurer should be informed at least 48 to 72 hours before admission for planned hospitalization (non-emergency), such as pre-planned surgery .

Point to be noted

How long does it take to process reimbursement claims?

Reimbursement claims mean you pay up front, then ask your insurer to repay you. The time frames in India typically work like this:

- For hospitalization, day‑care, or pre‑hospitalization costs, submit the claim within a week of discharge, though most policies allow up to 30 days from discharge.

- For post‑hospitalization expenses (tests, medicines, etc., after leaving the hospital), submit the health claims within 15-30 days after the post-hospitalization coverage period is completed.

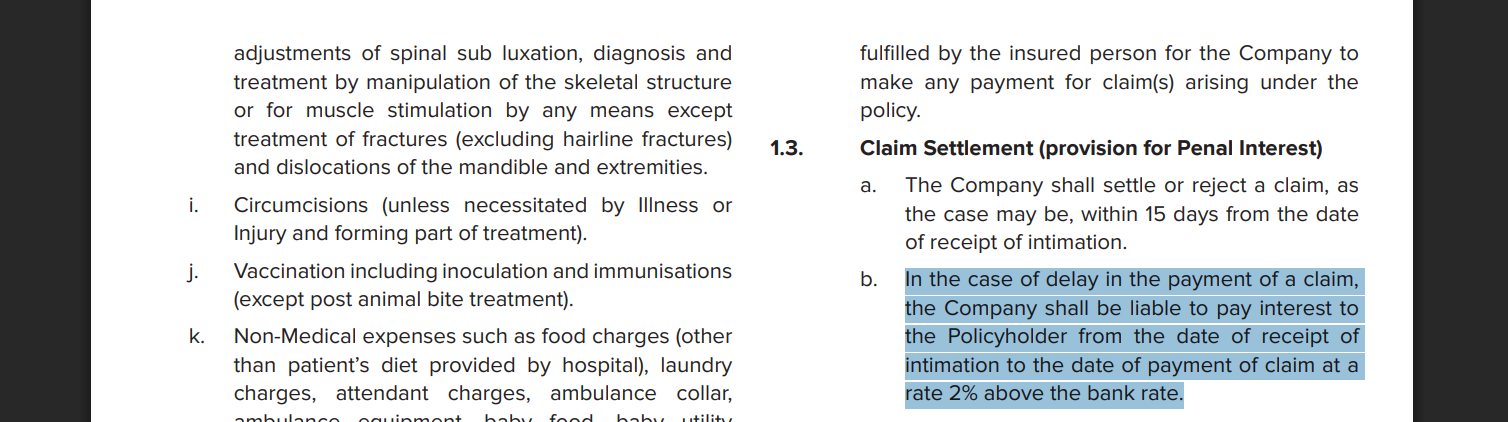

Once you submit all required documents, the insurer has time to process the claim. As discussed above, claims should be settled or rejected within 30 days of receiving all required documents. If an insurer needs to investigate further, the deadline extends to 45 days, after which they must pay interest.

Usually, the insurers can uphold the TurnAround Times (TATs) since they can request a document before the 30-day window and prevent any potential TAT breach.

Friendly Reminder

What are the factors influencing Claim Processing Time?

Several factors affect how long it takes from filing the claim to getting paid back. Here are the key ones:

Completeness of documents:

If your medical bills, discharge summary, test reports, doctor's prescriptions, identity proofs, etc., are all correct, clear, and complete, processing goes faster. Missing or wrong documents are a common cause of delay.

Be Careful

Type of claim:

Emergency and planned treatments, hospitalization, OPD, post-hospital care, and day-care procedures have different document requirements and approval steps. Emergency cases or complicated treatments usually need more paperwork and a detailed review, which can take extra time.

Timely intimation:

Especially for cashless claims, notifying the insurer quickly (within the required time) helps avoid delays. Late notifications often lead insurers to scrutinise cases more closely.

Policy terms & insurers' rules:

Different insurers may have different internal turnaround times. Some policies have stricter or tighter deadlines. Also, if policy wording requires additional approvals or medical checks, this will add time.

Hospital / TPA coordination:

Hospitals must send correct bills, treatment notes, and invoices; TPAs or insurer medical teams must verify. The claim is held up if a hospital or TPA delays submitting or verifying paperwork.

Point to be noted

Investigations or audits:

Sometimes, insurers order medical audits, verify with treating doctors, check if treatment is standard/preventive/excluded, etc. If any discrepancy or suspicion arises, this adds extra days.

Volume of claims/peak load:

When many claims are filed (e.g., during outbreaks, or when hospitals are busy), or when insurers' offices are overloaded, processing slows.

Did You Know?

Ditto’s take on the time limits of health insurance claims

A little preparation goes a long way to ensure your cashless claim goes through without delays. Follow these quick tips to stay ahead and avoid last-minute surprises:

- Save your insurer’s or TPA’s helpline number on your phone for quick access.

- Notify the insurer immediately after hospitalization, even a quick SMS or email works.

- Keep scanned copies of your bills, reports, and discharge summaries ready.

- Submit reimbursement claims early; don’t wait till the last day of the deadline.

- Always read your policy terms, as claim intimation timelines vary by insurer.

To check out how our experts at Ditto help our customers with claim assistance, click here.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Abhinav below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now!

Key Takeaways

Understanding the timelines and processes of cashless health insurance claims can save you from unnecessary delays and financial stress. Here are the most essential points to remember:

- Timely Notification is Crucial: Always inform your insurer within the required window, 24 to 48 hours for emergencies and 48 to 72 hours before planned hospitalizations to avoid approval issues.

- Insurer Response Time is Regulated: Insurers must respond to cashless requests within 1 hour and approve discharge within 3 hours. Delays beyond 45 days for any claim invite a 2% penalty above the bank rate.

- Document Accuracy Speeds Up Claims: Complete and accurate documentation, medical bills, reports, prescriptions, and IDs, is key to claim approval faster. Missing or unclear papers cause the most delays.

- Claim Type and Complexity Matters: Emergency and complex treatments often take longer due to additional reviews, while planned or OPD claims are usually processed faster if documents are in order.

Always remember, simple claims (e.g. - cataract, appendectomy) at network hospitals with clear documentation are usually approved within hours and settled before discharge. However, if the case involves undisclosed pre-existing conditions or unclear medical history, in that case, insurers may launch an investigation, delaying the claim by up to 45 days as they verify policy terms and rule out non-disclosure or fraud.

Still unsure how to file your health claims within time? Book a free call with us and let our experts help you file your claim on time.

Frequently Asked Questions

Last updated on: